THE GENDER GAP IN PENSIONS

Pensions are the main source of retirement income for the elderly, and it is well known that older women receive far less individual pension income than older men. All countries have adopted various mechanisms to take into account the wages lost by women because of their family constraints and to reduce their risk of poverty in old age.

However, before 1990, the gender pension gap was a blind spot, virtually invisible in the economic literature (Ginn, 2001), and it has only recently attracted attention (see Jefferson, 2009, for a survey; Folbre et al., 2005). There were two reasons for this invisibility. First, because pensions were based on past earnings, their less advantageous careers automatically led to smaller pensions for women, and the gender pension gap was viewed as a simple outcome of this fact. Second, it was considered that nearly all women were married, and married women shared the benefits from their husband’s entitlements, and this occurred even after his death through survivor’s pension schemes. In other words, the hypothesis of income pooling within the family was explicitly assumed for retiree couples and there was no point in studying gender inequality. Consequently, the gender aspect of pensions was covered from the perspective of the living standard of widows and spinsters, as the people most at risk of poverty. The policy issue was that of a safety net for old people and poverty (mainly women poverty) and/or the more or less generous way to transfer pension rights to the survivor (wife).The recent growing interest in the gender pension gap stems from three concurrent social evolutions. First, the end of the male breadwinner model in the 1960s has led to the current massive entry into the retirement system of generations of women with their own past work lives and their own pension entitlements. The usual analyses of the gender wage gap can then be transposed to the gender pension gap, with similar issues.

Should we expect a narrowing of the gender pension gap similar to that observed for the gender wage gap? To what extent do part-time, incomplete careers, occupational segregation, wage discrimination, and so on have adverse consequences on the level ofindividual pensions? Second, changes in family history with the decline in marriages, the rise in divorces, and the increase in cohabitation and celibacy have a direct impact on the gender pension gap. The typical figure of a single retired woman is now less likely to be a widow and more often a divorcee or spinster. This change calls into question the rationale of survivor’s pension schemes inherited from the past, when there was only one (male) breadwinner.Last but not least, population aging and the corresponding increase in the dependency ratio are exerting pressure on retirement schemes in all countries. The general trend in reforms is to reduce the level of pensions and to align pension benefits more closely with career trajectories. A pure contributory system—defined as a system where the total sum of pensions received by a pensioner is proportional to the discounted sum of contributions made during his or her working life—creates gender inequalities because of the previous gender inequalities in careers. The more the pensions system is based on contributions, the more it is disadvantageous to women. However, all countries have kept or expanded diverse mechanisms to counterbalance these (negative) gendered effects, such as noncontributory pensions, the use of unisex mortality tables to calculate contributions, and benefits or additional family rights.

In this section, we present the (few) statistics on the gender pension gap. We will see that it is even more difficult to obtain comparable international figures of this indicator than it is for the gender wage gap. Then we discuss the main mechanisms that determine the actual level of pensions and the extent to which the same rules may have a different impact on men’s and women’s pensions.

Finally, we turn to family history and its consequences on the gender pension gap. The main issue here is how to compensate for unpaid work such as caring for children or other family members and the emerging transition toward family rights and away from spouse’s rights.12.5.1 Sparse and Noncomparable Statistics

There is general agreement on the existence of a considerable gender pension gap, but there are no harmonized international statistics to compare the situation between countries. Some figures are available by country, but the way they are calculated is heavily dependent on the specificities of each national pension scheme.

One of the problems in obtaining comparable figures, which is also encountered for the gender wage gap, is the question of which population is considered. Is it limited to private pension recipients or not? Are social security pensions included or not? But there are also problems related to the variety of national pension schemes and the way data on pensions are collected. Is the gender pension gap measured at the household level, with information on the composition of earnings (direct pensions, derived pensions, savings income) or based on individual administrative data without information on the composition of the household? Finally, there is a difficulty specific to the gender issue. Unlike wages, which are defined on an individual basis and are a remuneration for hours worked, pensions may include rights derived from the spouse (pensions paid to the spouse or ex-spouse, survivors’ pensions) or from the family situation (family rights).

There are very few comparable international statistics, even fewer than for the gender wage gap. One exception is the recent document published by the European Commission (2013) presenting comparable tables based on the EU-SILC 2010 database. To the best of our knowledge, these are the only published statistics comparing countries available in 2014 and, by construction, the United States is not included in the comparison.

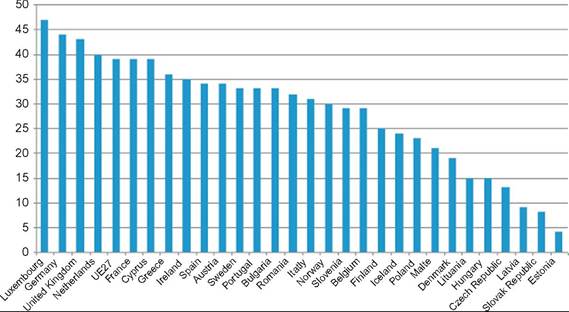

The population surveyed is defined as people over 65 years old not living in collective households[785] and receiving a pension. Because of the way the data are collected, the first “two pillars” of pensions—state pensions, based on societal solidarity and pay-as- you-go financing, and occupational pensions (OPs), based on occupational solidarity and prefunding—are not distinguished; only the third pillar (individual pension schemes) can be isolated. Another particularity of these figures is that survivor’s pensions are mixed with other pensions.According to this study, the average gender pension gap[786] in Europe was 39% in 2009, approximately twice the average gender wage gap for these countries.[787] Germany, the United Kingdom, and the Netherlands have a gender pension gap of more than 40%, whereas it is less than 25% in Nordic countries (Finland, Denmark), and Eastern European countries (Figure 12.6).

For the United States, scarce figures are given separately for the social security system (the first pillar in the United States) and for the private system. In both cases there is a gender pension gap, equal to 35% for the social security system (which includes spouse’s benefits) and stagnant over the past 50 years, despite the increase in the labor force attachment of women. This stagnation is mainly due to the US spousal benefits system: additional social security earnings have no effect on social security benefits because they replace the spousal entitlement (see below). The picture is different for private pensions: between 1978 and 2000, the ratio of women’s to men’s benefits increased from 0.23 to 0.29 (Even and Macpherson, 2004).

An additional difficulty in obtaining pertinent figures is that the population of retirees is far from homogenous in terms of work history and accumulated entitlements, so the average pension is not very informative, particularly for women: recent cohorts have had

Figure 12.6 Average gender pension gap in Europe (pensioners aged over 65 years).

Source: Bettio et al., 2013 - Based on EU-SILC UDB data 2010.a longer working life than the older cohorts, for whom the past norm was the one-earner family. This implies a narrowing of the gender pension gap, reflecting the dramatic growth in female participation in the labor market. For instance, in France in 2008, women’s own pensions were 44% of men’s for the 1924—1928 cohorts and 56% for the 1939—1943 cohorts (Andrieux and Chantel, 2011). However, the picture is not really so clear cut and depends on the viewpoint one adopts. Because the SILC statistics on pensions are not limited to personal entitlement pensions but include survivors’ pensions, the gender gap in total pensions by cohort does not indicate narrowing (Bettio et al., 2013). Comparing cohorts older than 80 years with the cohort aged 65-79, it can be seen that the younger groups face considerably wider gender pension gaps (41%vs. 33%). This surprising result is due to a combination of large proportions of widows who receive survivors’ pensions among the eldest women and selection effects (life expectancy is higher for former qualified workers, so pension benefits are relatively higher and the group is more homogeneous). Consequently, changes in women’s labor market participation result in attenuated changes in benefits for women; the benefits derived from spousal rights are replaced by benefits linked to individual careers.

12.5.2 The Gendered Effects of Pension Regulations

The individual gender pension gap mirrors work life inequality: women’s lower labor force participation, more part-time work, more career interruptions, and lower pay all have consequences on their pension entitlements and levels. Most studies (Even and Macpherson, 2004, for the United States; Bonnet and Geraci, 2009, for France) conclude that higher labor force participation and the narrowing of the gender wage gap will not suffice to produce pension equality in the future and there will be still a need to compensate for child-related career interruptions.

Differences in regulations (the extent of noncontributory schemes, the coverage of individual pension schemes, the minimum period of contributions required to establish entitlement, and the retirement age) and in the method of calculating pension benefits may amplify the gendered impact of work life differences (on international differences in pension progressivity see Aggarwal and Goodell, 2013).12.5.2.1 Coverage and Contributions: The Gendered Impact of Current Reforms Old-age pension schemes generally include a first minimum level with wide coverage, less demanding conditions, and a benefit level close to that of welfare benefits. Noncontributory schemes are a powerful way to loosen the link between career earnings (and associated contributions) and benefits (Bonnet and Geraci, 2009). They are one of the major tools to fight women’s poverty in old age. The Scandinavian countries propose the most generous scheme, with universal pensions for all residents. Most countries offer a kind of safety net but one with conditions and usually income tested; for instance, Canada’s “old age security,” the United Kingdom’s basic state pension (but with very low benefits), the ‘“minimum contributif’ in France (which is proportional to the duration of the career and is intended to compensate more for low wages than interrupted careers), or the “age pension” in Australia. Women constitute the majority of beneficiaries because of their interrupted careers and low wages.

Beyond these minimum pensions, the retirement income system is generally a mix of publicly administered social insurance (financed by employer and employee contributions) and private pension schemes supplemented by individual savings. The minimum length of employment required for entitlement to a pension may affect women more than men, given their shorter working lives. Pension reforms tend to lengthen the required period, but in some cases the higher labor participation of women has counterbalanced this negative effect, and the gender coverage gap is generally expected to narrow. For instance, the US public scheme (social security) now requires 40 quarters (15 in 1971), but the percentage of women entitled to social security benefits increased from 57% to 65% between 1980 and 1999 (Even and Macpherson, 2004). In most countries, pension reforms tend also to increase the legal age for full retirement benefits; in the United Kingdom, for instance, the state pension age, currently 60 for women and 65 for men, is being gradually equalized to reach 65 for both sexes in 2020. This can be more prejudicial to women than to men because the increase in the length of working life may not be sufficient to keep pace with the increase in the retirement age. OECD pension reforms also tend to align the legal age of retirement of men and women. In the past, the legal age of retirement for men has often been higher than that of women as a way of compensating women for unpaid care work. In 1995,15 OECD countries applied the same retirement age for men and women and 8 applied different ages; in 2013, only 2 countries (Israel and Switzerland) applied different retirement ages (64 for women, 65 for men) (OECD, 2013). The equalization of the legal age of retirement was favorable for women in higher-paid, full-time jobs, enabling them pursue their careers and to acquire more pension rights (and higher pension benefits), but it can increase income insecurity for women in precarious forms of employment (Luckhaus, 2000).

Another salient trend in pension reforms is to give a larger weight to individual private pension schemes provided through employers, that is, largely OPs, in other words, a switch from first to second pillar pensions (Behrendt, 2000). The link between contributions and the level of benefits is stronger than in public schemes (first pillar), and private pensions are viewed as the main source of the gender pension gap (Bardasi and Jenkins, 2010). This is particularly the case in the United Kingdom, where only 33% of women over 65 years old received a private pension in 1993—1994, compared with 61% of men (Ginn et al., 2001, p. 52). Because the schemes are provided voluntarily by employers, people in part-time employment, precarious jobs, and small organizations are less likely to be covered by OPs. Bardasi andJenkins (2010) estimated the effects of different variables on the probability of being covered by an OP and found significant correlations between women’s OP probabilities and labor status (part-time employment, time out of the labor market); marriage and children have only indirect effects through work history.

In the United States, the correlation between wage rates and pension coverage weakened after enactment of the Employment Retirement Income Security Act in 1974, which limits tax preferences for employer plans for which all workers, including the low paid, are eligible. However, women still tend to have lower rates of coverage because they are more likely than men to work in small firms and in low-paid or part-time jobs (Bajtelsmit, 2006). Similar regulations have been introduced in Europe: two judgments of the European Court of Justice in 1994 stipulated that the exclusion of part-time workers from OP schemes contravenes equal pay laws and may represent indirect discrimination against women.

Another possibility for rectifying gender gaps in pension coverage and entitlements is the policy of matching government contributions for low-income workers ( Jefferson, 2009). For instance, Australia has experimented with government cocontributions to personal superannuation accounts. A large proportion of women participate in this scheme, and it has been considered successful in encouraging women to build their private pension savings, although not enough to improve significantly the economic situation of old women (Olsberg, 2006). Moreover, there is doubt about whether it is possible for low-income earners in low-income households to save. It is likely that these savings came from high-income households (where women are in part-time, low-paid jobs), which can take advantage of these profitable cocontributions. In that case, first the policy target is missed, and second, it is not an individualization of private pension savings but a form of pooling savings at the household level (with predictable difficulties in case of divorce).

12.5.2.2 Benefit Calculation Methods

Benefit calculations are identical for men and women, but structural differences in working lives and life expectancies have different consequences on the level ofbenefits for men and women. Here we examine the consequences of three main characteristics in calculation methods: reference earnings years, defined benefits versus defined contributions, and the choice of annuity tables.

Women are more likely to have low earnings years in their careers, so the longer the reference periods used for benefit calculations, the more they are disadvantaged. For instance, France’s 1993 reform gradually increased the number of reference years from 10 to 25 in 2008. Using a microsimulation model, Bonnet et al. (2006) calculated that this reform would reduce the reference wage (which is used to determine the level of benefit) by over 20% for more than 30% ofwomen, compared with 12% of men. Another consequence of this reform is that it increases pension disparities between women.

The pension reforms that shift the focus from the first #961;illar to the second pillar often are combined with a change from defined benefit to defined contribution schemes (Mackenzie, 2010; Orenstein, 2013). In defined benefit schemes, the benefits are calculated using a fixed formula, and the risk of the amount to be paid is shared by employer and worker. In defined contribution schemes, the payout is dependent on both the amount contributed to an individual account and the performance of the investment vehicle.[788] The expansion of defined contribution schemes is analyzed as a transfer of risk from the employer and the worker to the beneficiary. The majority of pensions provided by private employers in the United States are now based on defined contributions (more than 85% in 2001), and they are expanding in OECD countries. In the United States, they are essentially tax-free saving accounts (i.e., a tax deferred account—retirement plans like the 401(k)), where employees choose whether to participate and how much to save for their retirement; it does not penalize quitters, unlike defined contributions.

Defined contributions offer the advantage of portability, which is appreciated by workers. This can be important for women because of their weaker attachment to the labor market. It is also likely, however, that women will not accumulate sufficient savings over their working lives—they tend to have lower amounts accumulated in their defined contribution plans (because of their lower wages) and therefore lower financial returns. In the event of a separation from their employer, they are more likely to use the lump sum to meet their urgent financial needs rather than roll it over into another tax-qualified savings plan (Bajtelsmit, 2006).

Another growing problem with this shift toward defined contributions is that participants have to be active in their employer’s pension plan. Actually, the general observation is that employees are passive and do not change the default rules proposed by employers (see Duflo and Saez, 2003). For women, the negative effect of this passive behavior may be exacerbated by their lower financial literacy compared with men (Van Rooij et al., 2011; see Fonseca et al., 2012, on financial literacy within the couple) and their higher risk aversion.

12.5.2.3 Life Expectancy, Gender, and Pensions

The gender gap in life expectancy also has an impact on individual contributions and benefits in defined contribution schemes, according to the way the benefits are designed. Calculations based on unisex mortality tables have a redistributive effect away from those with lower life expectancy (men) and toward those expected to live longer (women). If the calculations of pensions were based on sex-based actuarial factors, women’s pensions would tend to be lower than men’s or their contributions would be higher (10—15% higher) (Shilton, 2012). Whether benefits should be calculated on sex-based actuarial factors or unisex tables is an ongoing debate; insurance companies are pushing to be able to discriminate by gender (and their associated mortality tables) and apply gender-based contributions or benefits. The 1978 US Supreme Court ruled in favor of unisex tables, judging that differences in compensation based directly on sex are unlawful as a matter of statutory policy (Luckhaus, 2000) and that contributions and life annuities must be calculated from unisex mortality tables. The underlying rationale is that this ensures equity in the amount the employer pays to the employees, rather than equity in the lifetime value of that benefit to the employee (Jefferson, 2005). A similar debate was held in Europe in the 1990s, and the prohibition of sex-based mortality tables was imposed on insurance companies on the basis of antidiscrimination laws and reaffirmed in 2004 and then 2011 (Shilton, 2012).

12.5.3 Family Matters for Pensions, Too

So far we have examined the gender differences in individual pensions. The big picture is that the individual gender pension gap is due to differences in work history and that the narrowing of labor market participation and wage gaps is not sufficient to reduce gender inequality in pensions “as long as combining paid work and parenthood (or other caring responsibilities) affects women more than men” (Bajtelsmit, 2006). The role of career differences in the gender pension gap has been quantitatively estimated by Bardasi and Jenkins (2010). Using a regression-based decomposition of the average gender private pension income gap in the United Kingdom for people aged 66 and older,[789] they found that differences in returns to personal characteristics account for at least four-fifths of the private pension income gap among recipients. They conclude that this result is probably because of the nature of the jobs taken by these cohorts of workers (part time and of shorter duration). But they also suggest that women in these generations may have chosen not to contribute to private pensions in the expectation that they can rely on their husband’s entitlements.

There are strong associations between marital and fertility decisions, pensions coverage, and the level of benefits. Derived entitlements from marital status or family rights are an important component of women’s pensions and explain why the gap in living standards during retirement is relatively small compared with the individual gender pension gap. In France, for instance, the median standard of living of elderly women was 10% (single)[790] to 19% (widowed) lower than that of couples in 2009 (Bonnet and Hourriez, 2012).

97

There is a wide variety of pension entitlements derived from marital status. The US system is particularly generous from this point of view. The social security system includes a spousal retirement benefit, equal to 50% of the pension benefit of the spouse (or former spouse), subject to the condition of at least 10 years of marriage, and a survivor’s benefit equal to 100% of the husband’s actual benefit. Women’s eligibility to these benefits is based on their own earnings history; they receive whichever is higher between their own benefits and the derived pensions. One side effect of this system is that the couple’s replacement rate decreases mechanically with the labor market activity of women: one-earner couples have a maximum replacement rate (with a ceiling on monthly earnings) equal to 60% (40% for the husband plus an additional 20% for the spouse); two-earner couples, with individual benefits calculated on their own careers, have a maximum replacement rate by social security of 40% (there is no additional benefit for marital status). Actually, the replacement rate for married households is decreasing across generations from 50% (generations born in 1931—1935) to 45% (generations born in 1948—1953); this decline is being driven by the increase in the frequency of dual-earner couples with their own benefits (Wu et al., 2013). The eligibility condition of 10 years of marriage has aside effect on the duration of marriage: using American social security data, Goda et al. (2007) showed that couples tend to delay divorce decisions from year 9 to year 10.

In Germany and the United Kingdom, there is another type of spousal entitlement whereby pension rights are divided equally between spouses in the event of divorce. The mechanism is intended to remedy the low level of women’s own rights (because of unpaid work) and corresponds to a perfect pooling of the pensions rights acquired by the husband and wife during the marriage (Bonnet and Geraci, 2009). Denmark offers an interesting case study in adopting a completely opposite reform in 2006: private pension savings (which form the basis of pension incomes) were no longer regarded as community property in the event of divorce, but as private property. This reform should lead to a substantial decrease in divorced women’s pension income because men’s pension savings are 30% higher. Amilon (2012) exploited the natural experiment constituted by this change and the period of 7 months, during which couples could divorce without being affected by the reform, and she observed a significant increase in the probability of getting divorced and a rise in women’s savings within couples. As in the US case, this tends to prove the sensitivity of family status to the legal pension scheme.

Last, the survivor’s pension (defined as a percentage of the deceased spouse’s pension) is still used to guarantee the living standard of widows in most OECD countries. It is intended to compensate for the loss of the spouse’s pension and to reduce the gap in living standards between couples and widows by compensating widows for the loss of economies of scale within the couple. In a society where couples are stable, this survivor’s scheme equalizes the living standards of men and women in retirement (provided retired couples pool income).

However, there is increasing debate about the legitimacy and effectiveness of these spousal rights, especially the survivor’s pension, and a decline in these derived benefits. In Sweden, survivor’s pensions have been gradually abolished and, more recently, survivor’s benefits have been reduced in the Netherlands and Germany (OECD, 2007). Changes in marital history, with the increasing number of divorces and the decline in marriage, explain the need to reexamine the rationale of survivor’s schemes (see Bonnet and Hourriez, 2012). There are fewer widows and more spinsters and divorced women in elderly one-person households, so the effectiveness of survivor’s pensions in guaranteeing a decent living standard for older women is compromised. As a matter of fact, nowadays single mothers raising children seem to be more at risk of poverty than widows.

Because children and their consequences on mothers’ careers are at the core of the gender pension gap, family rights are gaining significance as a way to improve the situation of women in old age, in place of survivor’s schemes. Family rights have been extended in various European countries over the past 20 years (Bonnet and Geraci, 2009; D’Addio, 2013). In Italy, Germany, and the United Kingdom, family rights are limited and initially open only to parents who have not worked. France has a more generous system that combines different mechanisms: contribution credits for mothers,[791] old- age insurance for nonworking parents, and pension bonuses for parents of three or more children (this last measure is not aimed specifically at women). The tendency of a shift from marital rights to family rights reflects the decline of marriage and the shortening duration of couples but also recognizes the persistent family-related gender wage gap.

12.6.

More on the topic THE GENDER GAP IN PENSIONS:

- INTRODUCTION

- Atkinson Anthony, Bourguignon François. Handbook of Income Distribution. Volume 2A. North Holland,2014. — 2366 p., 2014

- Unemployment