Balance of Payments Accounting

Explain how

Examining the factors that affect international trade and lending first requires an the balance of

uιeuaιanceo1 understanding of the basics of balance of payments accounting.

The balance ofpaymentS iS payments accounts, which are part of the national income accounts discussed in

calculated. Chapter 2, are the record of a country's international transactions. As you read this

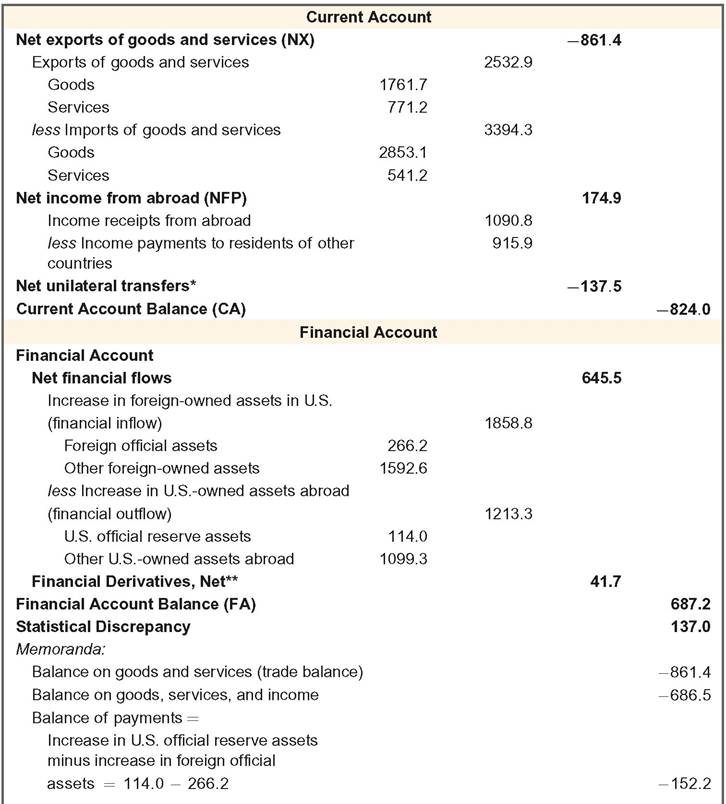

section, you should refer to Table 5.1, which presents U.S. balance of payments data for 2021.

The Current Account

The current account measures a country's trade in currently produced goods and services, along with unilateral transfers between countries. For convenience we divide the current account into three separate components: (1) net exports of goods and services, (2) net income from abroad, and (3) net unilateral transfers.

Net Exports of Goods and Services. We discussed the concept of net exports, NX, or exports minus imports, as part of the expenditure approach to measuring GDP in Chapter 2. Here we point out that net exports often are broken into two categories: goods and services.

Examples of internationally traded goods include U.S. soybeans, French perfume, Brazilian coffee, and Japanese cars. When a U.S. consumer buys a Japanese car, for example, the transaction is recorded as an import of goods for the United States and an export of goods for Japan.

Internationally traded services include tourism, insurance, education, and financial services. The Application "The Impact of Globalization on the U.S. Economy," discusses trade in business services. When a group of friends from the United States spends a week's vacation in Mexico, for example, the friends' expenditures for accommodations, food, sightseeing tours, and so on, are in the U.S. current account as an import of tourism services.

The friends' expenditures are an export of tourism services for Mexico. Similarly, when foreign students attend college in the United States, their tuition payments are exports of services for the United States and imports of services for their home countries.TABLE 5.1

Balance of Payments Accounts of the United States, 2021 (Billions of Dollars)

Note: Numbers may not add to totals shown owing to rounding.

*Net unilateral transfers includes the balance on secondary income (transfers of income) and the capital account (transfers of assets). The capital account is usually very small.

**The sign has been reversed from BEA Table 1 so that a positive number is a net increase in foreign-owned assets in U.S. (an inflow).

Source: “U.S. International Transactions: Fourth Quarter and Year 2021,” Table 1, BEA news release downloaded from www.bea.gov/sites/default/files/2022-03/intinv421.pdf, and International Transactions Accounts, Table 9.1, downloaded from https://www.bea.gov/data/intl-trade-investment/international-transactions.

Table 5.1 shows that in 2021, U.S. exports of goods were more than twice as large as exports of services. Imports of goods were over five times as large as imports of services. Note also that exports of goods were much smaller than imports of goods but the reverse is true for services—U.S. firms export more services to other countries than are imported into the United States.

Net Income from Abroad. Net income from abroad equals income receipts from abroad minus income payments to residents of other countries. It is almost equal to net factor payments from abroad, NFP, discussed in Chapter 2.1 We will ignore the difference between NFP and net income from abroad and treat the two as equivalent concepts.

The income receipts flowing into a country consist of compensation received by residents working abroad plus investment income from assets abroad.

Investment income from assets abroad includes interest payments, dividends, royalties, and other returns that residents of a country receive from assets (such as bonds, stocks, and patents) that they own in other countries. An example isIn Touch with Data and Research

The Balance of Payments Accounts in Malaysia

We continue the example of Malaysia from Chapter 2 in this case. The Malaysian balance of payments statistics are governed by the Statistics Act of 1965 (revised in 1989). Generally, all data sources are on a quarterly basis, and updates of survey coverage are performed on a quarterly basis as well. Balance of payments estimates are compiled in millions of ringgits and are, as much as possible, in accordance with the international standards recommended by the International Monetary Fund (IMF). The Department of Statistics Malaysia (DOSM) is an official compiler of balance of payments estimates for Malaysia on a quarterly basis. It releases the official estimates for the previous year in the September of the following year, while the Central Bank of Malaysia releases preliminary balance of payments (BOP) estimates for the previous year in the March of the following year. Projections for the following year are made available by the Ministry of Finance (MOF) in the October of the current year.

The DOSM obtains data from various sources including surveys, Bank Negara Malaysia (BNM), government agencies such as Royal Malaysia Customs and the Pilgrimage Fund Board, and other administrative sources.

The data are published in the DOSM's Quarterly Balance of Payments reports and BNM's Quarterly Bulletin. The DOSM also reports the data published in the Quarterly Balance of Payments to the IMF. Any errors detected are announced in the current or next publication or dissemination. Select government agencies, such as the MOF, BNM, and the Economic Planning Unit of the Prime Minister's Department, have access to the data one week before release to the public.

Statistical discrepancies and other problems are resolved at a quarterly technical meeting held with BNM. Revisions of quarterly BOP for the previous year are published together with data for the first quarter of the current year. If there are major changes regarding methodology, source data, and statistical techniques, an announcement is made by the DOSM through the department's website as well as its publication.[78] [79]interest received by a U.S. saver who owns a French government bond. Another example is the profits earned by a U.S. company from its foreign subsidiary. In both examples, the income is recorded as income receipts from abroad.

The income payments flowing out of a country consist of compensation paid to foreign residents working in the country plus payments to foreign owners of assets in the country. For example, the wages paid by a U.S. company to a Swedish engineer who is temporarily residing in the United States, or the dividends paid by a U.S. automobile company to a Mexican owner of stock in the company, are both income payments to residents of other countries.

Net Unilateral Transfers. Unilateral transfers are payments from one country to another that do not correspond to the purchase of any good, service, or asset. Examples are official foreign aid (a payment from one government to another) or a remittance of money from a resident of one country to family members living in another country. A country's net unilateral transfers equal unilateral transfers received by the country minus unilateral transfers flowing out of the country. The negative value of net unilateral transfers in Table 5.1 shows that the United States is a net donor to other countries.

Current Account Balance. Adding net exports of goods and services, net income from abroad, and net unilateral transfers yields a number called the current account balance. If the current account balance is positive, the country has a current account surplus.

If the current account balance is negative, the country has a current account deficit. As Table 5.1 shows, in 2021 the United States had a $824.0 billion current account deficit, equal to the sum of net exports of goods and services (NX = — $861.4 billion), net income from abroad (NFP = $174.9 billion), and net unilateral transfers (-$137.5 billion).The Financial Account

International transactions involving assets, either real or financial, are recorded in the financial account. When a U.S. firm or resident sells an asset to another country, for example, if a U.S. hotel is sold to Italian investors, the transaction is recorded as an increase in foreign-owned assets in the United States, which is a financial inflow, because funds flow into the United States to pay for the asset. Similarly, when the home country buys an asset from abroad—say a U.S. resident opens a Swiss bank account—the transaction involves a financial outflow from the United States and is recorded as an increase in U.S.-owned assets abroad.

The financial account balance equals the value of financial inflows minus the value of financial outflows plus the net increase in foreign-owned derivatives (which are financial assets whose value is based on, or "derived" from, the values of other assets) in the United States. When residents of a country sell more assets to foreigners than they buy from foreigners, the financial account balance is positive, creating a financial account surplus. When residents of the home country purchase more assets from foreigners than they sell, the financial account balance is negative, creating a financial account deficit. Table 5.1 shows that in 2021, U.S. residents increased their holdings of foreign assets (ignoring financial derivatives and unilaterally transferred assets) by $1213.3 billion while foreigners increased their holdings of U.S. assets by $1858.8 billion. Thus the United States had net financial flows of $645.5 billion in 2021 ($1858.8 billion minus $1213.3 billion).

Adding the net change in financial derivatives, the financial account balance in 2021 was $687.2 billion.The Balance of Payments. In Table 5.1 one set of financial flows—transactions in official reserve assets—has been broken out separately. These transactions differ from other financial account transactions in that they are conducted by central banks (such as the Federal Reserve in the United States), which are the official institutions that determine national money supplies. Held by central banks, official reserve assets are assets, other than domestic money or securities, that can be used in making international payments. Historically, gold was the primary official reserve asset, but now the official reserves of central banks also include government securities of major industrialized economies, foreign bank deposits, and special assets created by the International Monetary Fund.

Central banks can change the quantity of official reserve assets they hold by buying or selling reserve assets on open markets. For example, the Federal Reserve could increase its reserve assets by using dollars to buy gold. According to Table 5.1 (see the line "U.S. official reserve assets"), in 2021 the U.S. central bank acquired $114.0 billion of official reserve assets. In the same year foreign central banks increased their holdings of dollar-denominated reserve assets by $266.2 billion (see the line "Foreign official assets"). The balance of payments is the net increase (domestic less foreign) in a country's official reserve assets. A country that increases its net holdings of reserve assets during a year has a balance of payments surplus, and a country that reduces its net holdings of reserve assets has a balance of payments deficit. For the United States in 2021 the balance of payments was -$152.2 billion (equal to the $114.0 billion increase in U.S. reserve assets minus the $266.2 billion increase in foreign dollar-denominated reserve assets). Thus the United States had a balance of payments deficit of $152.2 billion in 2021.

For the issues we discuss in this chapter, the balances on current account and on financial account play a much larger role than the balance of payments. We explain the macroeconomic significance of the balance of payments in Chapter 13 when we discuss the determination of exchange rates.

The Relationship Between the Current Account and the Financial Account

The logic of balance of payments accounting implies a close relationship between the current account and the financial account. Except for errors arising from problems of measurement, in each period the current account balance and the financial account balance must sum to zero. That is, if

CA = current account balance and

FA = financial account balance,

then

CA + FA = 0. (5.1)

The reason that Eq. (5.1) holds is that every international transaction involves a swap of goods, services, or assets between countries. The two sides of the swap always have offsetting effects on the sum of the current account and the financial account balances, CA + FA. Thus the sum of the current account and the financial account balances must equal zero.

Table 5.2 helps clarify this point. Suppose that a U.S. consumer buys an imported British sweater, paying $75 for it. This transaction is an import of goods to the United States and thus reduces the U.S. current account balance by $75. However, the British exporter who sold the sweater now holds $75. What will he do with it? There are several possibilities, any of which will offset the effect of the purchase of the sweater on the sum of the current account and the financial account balances.

The Briton may use the $75 to buy a U.S. product—say, a computer game. This purchase is a $75 export for the United States. This U.S. export, together with the original import of the sweater into the United States, results in no net change in the U.S. current account balance CA. The U.S. financial account balance FA hasn't changed, as no assets have been traded. Thus the sum of CA and FA remains the same.

A second possibility is that the Briton will use the $75 to buy a U.S. asset—say, a bond issued by a U.S. corporation. The purchase of this bond is a financial inflow to the United States. This $75 increase in the U.S. financial account offsets the $75 reduction in the U.S. current account caused by the original import of the sweater. Again, the sum of the current account and the financial account balances, CA + FA, is unaffected by the combination of transactions.

TABLE 5.2

Why the Current Account Balance and the Financial Account Balance Sum to Zero: An Example (Balance of Payments Data Refer to the United States)

| Case I: United States Imports $75 Sweater from Britain; | |

| Britain Imports $75 Computer Game from United States | |

| Current Account | |

| Exports | $75 |

| less Imports | $75 |

| Current account balance, CA | 0 |

| Financial Account | |

| No transaction | |

| Financial account balance, FA | 0 |

| Sum of current and financial account balances, CA + FA | 0 |

| Case II: United States Imports $75 Sweater from Britain; | |

| Britain Buys $75 Bond from United States | |

| Current Account | |

| less Imports | $75 |

| Current account balance, CA | -$75 |

| Financial Account | |

| Financial inflow | $75 |

| Financial account balance, FA | $75 |

| Sum of current and financial account balances, CA + FA | 0 |

| Case III: United States Imports $75 Sweater from Britain; | |

| Federal Reserve Sells $75 of British Pounds to British Bank | |

| Current Account | |

| less Imports | $75 |

| Current account balance, CA | -$75 |

| Financial Account | |

| Financial inflow (reduction in U.S. official reserve assets) | $75 |

| Financial account balance, FA | + $75 |

| Sum of current and financial account balances, CA + FA | 0 |

Finally, the Briton may decide to go to his bank and trade his dollars for British pounds. If the bank sells these dollars to another Briton for the purpose of buying U.S. exports or assets, or if it buys U.S. assets itself, one of the previous two cases is repeated. Alternatively, the bank may sell the dollars to the Federal Reserve in exchange for pounds. But in giving up $75 worth of British pounds, the Federal Reserve reduces its holdings of official reserve assets by $75, which counts as a financial inflow. As in the previous case, the financial account balance rises by $75, offsetting the decline in the current account balance caused by the import of the sweater.[80]

This example shows why, conceptually, the current account balance and the financial account balance must always sum to zero. In practice, problems in measuring international transactions prevent this relationship from holding exactly. The amount that would have to be added to the sum of the current account and the financial account balances for this sum to reach its theoretical value of zero is called the statistical discrepancy. As Table 5.1 shows, in 2017 the statistical discrepancy was $92.5 billion.

When you examine the data on the current account across countries, you see that for most of the past decade, the advanced economies of the world together ran a large current account deficit, while emerging and developing economies around the world ran a very large current account surplus. This means the emerging and developing economies have invested some of their saving in developed countries. See the Application "Recent Trends in the U.S. Current Account Deficit," for some reasons why this may have occurred.

Net Foreign Assets and the Balance of Payments Accounts

In Chapter 2 we defined the net foreign assets of a country as the foreign assets held by the country's residents (including, for example, foreign stocks, bonds, or real estate) minus the country's foreign liabilities (domestic physical and financial assets owned by foreigners). Net foreign assets are part of a country's national wealth, along with the country's domestic physical assets, such as land and the capital stock. The total value of a country's net foreign assets can change in two ways: (1) the value of existing foreign assets and foreign liabilities can change, as when stock held by a U.S. citizen in a foreign corporation increases in value or the value of U.S. farmland owned by a foreigner declines; and (2) the country can acquire new foreign assets or incur new foreign liabilities.

What determines the quantity of new foreign assets that a country can acquire? In any period the net amount of new foreign assets that a country acquires equals its current account surplus. For example, suppose a country exports $10 billion more in goods and services than it imports and thus runs a $10 billion current account surplus (assuming that net factor payments from abroad, NFP, and net unilateral transfers both are zero). The country must then use this $10 billion to acquire foreign assets or reduce foreign liabilities. In this case we say that the country has undertaken net foreign lending of $10 billion.

Similarly, if a country has a $10 billion current account deficit, it must cover this deficit either by selling assets to foreigners or by borrowing from foreigners. Either

SUMMARY 7____________________________________________________

Equivalent Measures of a Country's International Trade and Lending

Each Item Describes the Same Situation

A current account surplus of $10 billion

A financial account deficit of $10 billion

Net acquisition of foreign assets of $10 billion

Net foreign lending of $10 billion

Net exports of $10 billion (if net factor payments, NFP, and net unilateral transfers equal zero)

action reduces the country's net foreign assets by $10 billion. We describe this situation by saying that the country has engaged in net foreign borrowing of $10 billion.

One important way in which a country borrows from foreigners occurs when a foreign business firm buys or builds capital goods; this is known as foreign direct investment. For example, when the Honda Motor Company from Japan builds a new auto production facility in Ohio, it engages in foreign direct investment. Because the facility is built in the United States but is financed by Japanese funds, foreign-owned assets in the United States increase, so the financial account balance increases. Foreign direct investment is different from portfolio investment, in which a foreigner acquires securities sold by a U.S. firm or investor. An example of portfolio investment occurs when a French investor buys shares of stock in Microsoft Corporation. This transaction also increases the financial account balance, as it represents an increase in foreign-owned assets in the United States.

Equation (5.1) emphasizes the link between the current account and the acquisition of foreign assets. Because CA + FA = 0, if a country has a current account surplus, it must have an equal financial account deficit. In turn, a financial account deficit implies that the country is increasing its net holdings of foreign assets. Similarly, a current account deficit implies a financial account surplus and a decline in the country's net holdings of foreign assets. Summary table 7 presents some equivalent ways of describing a country's current account balance and its acquisition of foreign assets.

Application

The United States as International Debtor

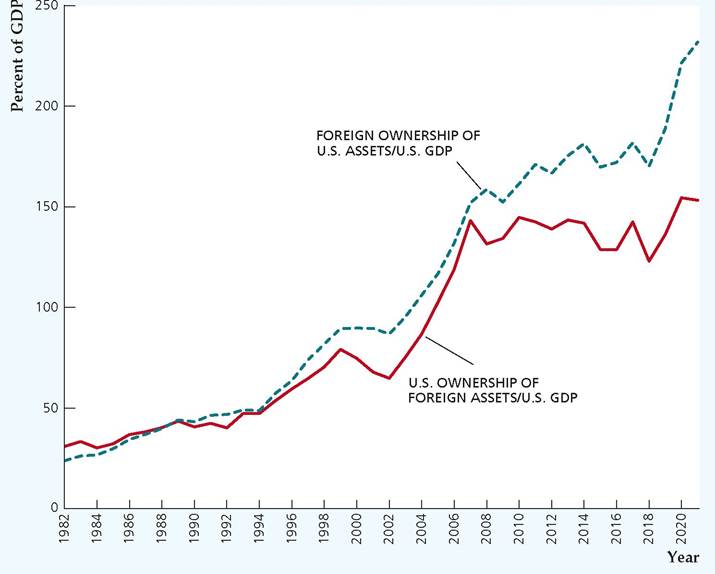

From about World War I until the 1980s, the United States was a net creditor internationally; that is, it had more foreign assets than liabilities. Since the early 1980s, however, the United States has consistently run large annual current account deficits. These current account deficits have had to be financed by net foreign borrowing (which we define broadly to include the sale of U.S.-owned assets to foreigners as well as the incurring of new foreign debts).

The accumulation of foreign debts and the sale of U.S. assets to foreigners have, over time, changed the United States from a net creditor internationally to a net debtor. Figure 5.1 shows the U.S. ownership of foreign assets and foreign ownership of U.S. assets, both measured as a percent of U.S. GDP, since 1982. As you can see, foreign ownership of U.S. assets overtook the U.S. ownership of foreign

FIGURE 5.1

International ownership of assets relative to U.S. GDP, 1982-2021

The chart shows annual values for ownership of foreign assets by U.S. residents and ownership of U.S. assets by foreigners, each as a percentage of U.S. GDP for the period 1982 to 2021.

Sources: International ownership of assets: Bureau of Economic Analysis, International Economic Accounts, International Investment Position, Table 1.1, available at ap-ps.bea.gov/iTable/ index_ita.cfm. GDP: Bureau of Economic Analysis, National Income and Product Accounts, available at fred.stlouisfed.org/ series/GDPA.

assets in the late 1980s and the gap between the two has grown substantially since then. According to estimates by the Bureau of Economic Analysis, at the end of 2021 the United States had net foreign assets of -$18.1 trillion, measured at current market prices. Equivalently, we could say that the United States had net foreign debt of $18.1 trillion.[81] This international obligation of more than $18 trillion is larger than that of any other country, making the United States the world's largest international debtor. This figure represents an increase of indebtedness of $4.1 trillion from yearend 2020. The U.S. current account deficit in 2021 was $824 billion. But the net debt of the United States increased by more because changes in the prices of stocks, bonds, and other assets caused increases in the value of foreign- owned assets in the United States relative to the value of U.S.-owned assets abroad.

Although the international debt of the United States is large, the numbers need to be put in perspective. First, the economic burden created by any debt depends not on the absolute size of the debt but on its size relative to the debtor's economic resources. Even at $18.1 trillion, the U.S. international debt is only about 79% of one year's GDP (U.S. GDP in 2021 was $20,894 billion). By contrast, some countries, especially certain developing countries, have ratios of net foreign debt to annual GDP that exceed 100%. Second, the large negative net foreign asset position of the United

States doesn't imply that it is being "bought up" or "controlled" by foreigners. If we focus on foreign direct investment, in which a resident of one country has ownership in a business in another country and has influence over the management of that business, it appears that the United States has a slightly smaller presence in other countries than they do in the United States. At the end of 2020, the market value of U.S. direct investment in foreign countries was $11,035 billion, and the market value of foreign direct investment in the United States was $14,840 billion.[82]

In evaluating the economic significance of a country's foreign debt, keep in mind that net foreign assets are only part of a country's wealth; the much greater part of wealth is a country's physical capital stock and (though it isn't included in the official national income accounts) its "human capital"—the economically valuable skills of its population. Thus, if a country borrows abroad but uses the proceeds of that borrowing to increase its physical and human capital, the foreign borrowing is of less concern than when a country borrows purely to finance current consumption spending. Unfortunately, the deterioration of the U.S. net foreign asset position doesn't appear to have been accompanied by any significant increase in the rates of physical investment or human capital formation in the United States. In that respect, the continued high rate of U.S. borrowing abroad is worrisome but unlikely to create a crisis in the near term.

5Incidentally, the largest direct investor in the United States is Japan. Japan is also the country that receives the most direct investment from the United States. For data on the distribution of U.S. direct investment abroad and foreign direct investment in the United States, see "Direct Investment by Country and Industry, 2020," Bureau of Economics Analysis website at WwwbeagpvlnewsIlOTlI direct-investment-country-and.-ind.ustry-2020, July 2021.

5.2

More on the topic Balance of Payments Accounting:

- Balance of Payments Accounting

- 23 Balance of Payments

- Detailed Contents

- Saving and Investment in Large Open Economies

- Abel A.B., Bernanke B., Croushore D.. Macroeconomics. 10th Edition, Global Edition. — Pearson,2021. — 690 pp., 2021

- The Production Function and Changes in Productivity in the European Union

- Glossary

- AYUB AND THE 1962 CONSTITUTION

- 25 Monetary Policy and Fiscal Policy

- Theory of the firm