Technological Change and the Canonical Neoclassical Model

The above analysis was for the neoclassical growth model without any technological change. As with the basic Solow model, the neoclassical growth model does not account for the long-run growth experience of the world economy without some type of exogenous technological change.

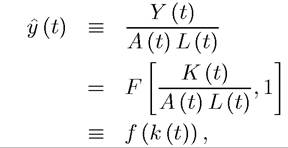

Therefore, the more interesting version of this model is the one that incorporates technological change. I now analyze the neoclassical model with exogenous technological change.The production function is extended to:

(8.43) Y (t) = F [K (t),A (t) L (t)],

where

A (t) = exp (gt) A (0).

Notice that the production function (8.43) imposes purely labor-augmenting—Harrod- neutral—technological change. This is because Theorem 2.6 in Chapter 2 still applies and implies that balanced growth is only possible with technological change that is asymptotically labor-augmenting. As in that chapter, I simplify the analysis by assuming that technological change is labor-augmenting throughout.

Assumptions 1, 2 and 3 on the production and utility functions are still in effect. Assumption 40 will be strengthened further in order to ensure finite discounted utility in the presence of sustained economic growth.

The constant returns to scale feature again enables us to work with normalized variables.

Now let us define

where

is the effective capital-labor ratio, written incorporating labor-augmenting technology in the denominator. Naturally, this is similar to the way that the effective capital-labor ratio was defined in the basic Solow growth model.

In addition to the assumptions on technology, we also need to impose a further assumption on preferences in order to ensure balanced growth.

As in the basic Solow model, balanced growth is defined as a pattern of growth consistent with the Kaldor facts of constant capitaloutput ratio and capital share in national income. These two observations together also imply that the rental rate of return on capital, R (t), has to be constant, which, from (8.10), implies that r (t) has to be constant. Let us again refer to an equilibrium path that satisfies these conditions as a balanced growth path (BGP). Balanced growth also requires that consumption and output grow at a constant rate. The Euler equation implies that

that is, if the elasticity of marginal utility of consumption is asymptotically constant. Therefore, balanced growth is only consistent with utility functions that have asymptotically constant elasticity of marginal utility of consumption. Since this result is important, I state it as a proposition:

that is, if the elasticity of marginal utility of consumption is asymptotically constant. Therefore, balanced growth is only consistent with utility functions that have asymptotically constant elasticity of marginal utility of consumption. Since this result is important, I state it as a proposition:

PROPOSITION 8.5. Balanced growth in the neoclassical model requires that asymptotically (as t → ∞) all technological change is purely labor-augmenting and the elasticity of intertemporal substitution, εu (c (t)), tends to a constant εu.

The next example shows the family of utility functions with constant intertemporal elasticity of substitution, which are also those with a constant coefficient of relative risk aversion.

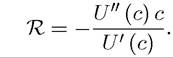

Example 8.1. (CRRA Utility) Recall that the Arrow-Pratt coefficient of relative risk aversion for a twice differentiable concave utility function U (c) is

The constant relative risk aversion (CRRA) utility function satisfies the property that R is constant. Now integrating both sides of the previous equation, setting R to a constant, implies that the family of CRRA utility functions is given by

with the coefficient of relative risk aversion is given by θ (see Exercise B.9 in Appendix Chapter B for a formal derivation).

In writing this expression, I separated the case where is undefined at θ = 1. However, it can be shown that ln c is indeed the right limit when θ → 1 (see Exercise 5.4).

is undefined at θ = 1. However, it can be shown that ln c is indeed the right limit when θ → 1 (see Exercise 5.4). With time-separable utility functions, the inverse of the elasticity of intertemporal substitution (defined in eq. (8.29)) and the coefficient of relative risk aversion are identical.

Therefore, the family of CRRA utility functions are also those with constant elasticity of intertemporal substitution.

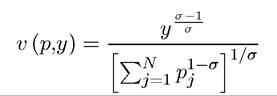

Now to link this utility function to the Gorman preferences discussed in Chapter 5, let us consider a slightly different problem in which an individual has preferences defined over the consumption of N commodities {c1,...,cn} given by

Suppose also that this individual faces a price vector p ≠(pι,...,Pn) and has income y, so that his budget constraint can be expressed as

Maximizing utility subject to this budget constraint leads to the following indirect utility

function

(see Exercise 5.6). Although this indirect utility function does not satisfy the Gorman form in Theorem 5.2, a monotonic transformation thereof does (simply raise it to the power σ/ (σ - 1)).

This establishes that CRRA utility functions are within the Gorman class, and if all individuals have CRRA utility functions, then we can aggregate their preferences and represent them as if they belonged to a single individual.

Now consider a dynamic version of these preferences (defined over infinite horizon):

The important feature of these preferences in growth theory is not that the coefficient of relative risk aversion is constant, but that the intertemporal elasticity of substitution is constant (since most of growth models do not feature uncertainty, but involve intertemporal allocation of consumption).

However, as illustrated in Exercise 5.2 in Chapter 5, with time-separable utility functions the coefficient of relative risk aversion and the inverse of the intertemporal elasticity of substitution are identical. The intertemporal elasticity of substitution is particularly important in growth models because it regulates how willing individuals are to substitute consumption over time, thus their savings and consumption behavior. In view of this, it may be more appropriate to refer to CRRA preferences as “constant intertemporal elasticity of substitution” preferences. Nevertheless, we follow the standard convention in the literature and stick to the term CRRA.Given the restriction that balanced growth is only possible with preferences featuring a constant elasticity of intertemporal substitution, let us start with the CRRA instantaneous 337

utility function

where the elasticity of marginal utility of consumption, εu, is given by the constant θ. When θ = 0, these represent linear preferences, whereas when θ = 1, they correspond to log preferences. As θ → ∞, these preferences become infinitely risk-averse, and infinitely unwilling to substitute consumption over time.

More specifically, the economy now admits a representative household with CRRA pref

erences

where c (t) ? C (t) /L (t) is per capita consumption. I refer to this model, with laboraugmenting technological change and CRRA preference as given by (8.47) as the canonical model, since it is the model used in almost all applications of the neoclassical growth model. In this model, the representative household’s problem is given by the maximization of (8.47) subject (8.8) and (8.14). Once again using the necessary conditions from Theorem 7.13, the Euler equation of the representative household is obtained as

Let us first characterize the steady-state equilibrium in this model with technological progress.

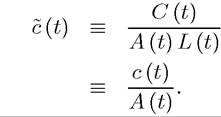

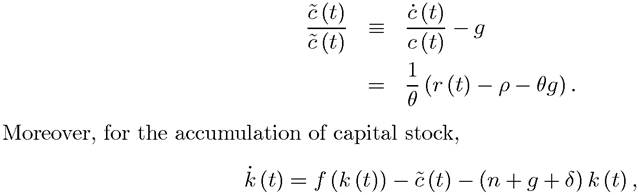

Since with technological progress there will be growth in per capita income, c (t) will grow. Instead, in analogy with k (t), let us define

This normalized consumption level will remain constant along the BGP. In particular,

where recall that k (t) ? K (t) /A (t) L (t).

The transversality condition, in turn, can be expressed as

In addition, the equilibrium interest rate, r (t), is still given by (8.26). Moreover, since in steady state (BGP) c (t) must remain constant, r (t) = ρ + θg,which implies that

(8.50)

This equation pins down the steady-state value of the normalized capital ratio k* uniquely, in a way similar to the model without technological progress. The level of normalized consumption is then given by

while per capita consumption grows at the rate g.

The only additional complication in this case is that because there is now sustained growth, the transversality condition becomes more demanding. In particular, substituting

(8.50) into (8.49),

which can only hold if the integral within the exponent goes to zero, that is, only if ρ - (1 - θ) g - n > 0. This implies that to ensure a well-defined solution to the household maximization problem and a well-defined competitive equilibrium, we need to modify Assumption 40 to:

Assumption 4. (Discounting with Technological Progress)

Note that this assumption strengthens Assumption 40 when θ < 1.

Recall that in steady state r = ρ + θg and the growth rate of output is g + n. Therefore, Assumption 4 is equivalent to requiring that r > g + n. Assumption 4 will emerge as a necessary condition for the transversality condition to be satisfied in many different models. It is also related to issues of “dynamic efficiency” discussed in the next chapter.At this point, we can also use a similar reasoning to that in Section 8.2 and establish that, given Assumption 4, the sufficiency conditions in Theorem 7.14 are satisfied, so that the solution to the household maximization problem derived above indeed corresponds to a global maximum (see Exercise 8.18). In this light, the following is an immediate generalization of Proposition 8.2:

PROPOSITION 8.6. Consider the neoclassical growth model with labor-augmenting technological progress at the rate g and preferences given by (8.f7). Suppose that Assumptions 1, 2, 3 and 4 hold. Then, there exists a unique BGP with a normalized capital to effective labor ratio of k*, given by (8.50), and output per capita and consumption per capita grow at the rate g.

The steady-state (BGP) capital-labor ratio is no longer independent of the utility function of the representative household, since now the steady-state capital-labor ratio, k* given by 339

(8.50), depends on the elasticity of marginal utility (or the inverse of the intertemporal elasticity of substitution), θ. This is because there is now positive growth in output per capita, and thus in consumption per capita. Since individuals face an upward-sloping consumption profile, their willingness to substitute consumption today for consumption tomorrow determines how much they will accumulate and thus the equilibrium effective capital-labor ratio.

Perhaps the most important implication of Proposition 8.6 is that, while the steady-state effective capital-labor ratio, k*, is determined endogenously, the steady-state growth rate of the economy is given exogenously and is equal to the rate of labor-augmenting technological progress, g. Therefore, the neoclassical growth model, like the basic Solow growth model, endogenizes the capital-labor ratio, but not the growth rate of the economy. The advantage of the neoclassical growth model is that the capital-labor ratio and the equilibrium level of (normalized) output and consumption are determined by the preferences of the individuals rather than an exogenously fixed saving rate. This also enables us to compare equilibrium and optimal growth (and in this case conclude that the competitive equilibrium is Pareto optimal and any Pareto optimum can be decentralized). But the determination of the rate of growth of the economy is still outside the scope of analysis.

A similar analysis to before also leads to a generalization of Proposition 8.4.

PROPOSITION 8.7. Consider the neoclassical growth model with labor-augmenting technological progress at the rate g and preferences given by (8.47). Suppose that Assumptions

Proof. See Exercise 8.19. ?

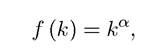

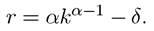

It is also useful to briefly look at an example with Cobb-Douglas technology.

Example 8.2. Consider the model with CRRA utility and labor-augmenting technological progress at the rate g. Assume that the production function is given by F (K, AL) =

and thus

and thus In this case, suppressing time dependence to simplify notation, the

In this case, suppressing time dependence to simplify notation, the

Euler equation written in terms of normalized consumption becomes

and the accumulation equation can be written as

and also

which implies that

The two differential equations (8.52) and (8.53) together with the initial condition x (0) and the transversality condition completely determine the dynamics of the system. In Exercise 8.22, you are asked to complete this example for the special case in which θ → 1 (log preferences).

8.8.

More on the topic Technological Change and the Canonical Neoclassical Model:

- Technological Change and the Canonical Neoclassical Model

- Acemoglu Daron. Introduction to Modern Economic Growth: Parts 1-4. Department of Economics, Massachusetts Institute of Technology,2008. — 604 p., 2008

- Taking Stock

- Contents

- Table of contents

- Acemoglu D.. Introduction to Modern Economic Growth. Princeton University Press,2008. — 1248 p., 2008

- Preface

- Taking Stock

- Optimal Growth in Discrete Time