Why Doesn’t Capital Flow from Rich to Poor Countries?

The model studied in the previous section provides us with a framework to answer the question posed above and in the title of this section. In the basic Solow and neoclassical growth models, a key source of cross-country income differences is capital-labor ratios.

For example, if we consider a world economy in which all countries have access to the same technology and there are no human capital differences, the only reason why one country would be richer than another is differences in capital-labor ratios. But if two countries with the same production possibilities set differ in terms of their capital-labor ratios, then the rate of return to capital will be lower in the richer economy and there will be incentives for capital to flow from rich to poor countries. We now discuss reasons why capital may not flow from societies with higher capital-labor ratios to those with greater capital scarcity.19.2.1. Capital Flows under Perfect International Capital Markets. One potential answer to the question posed above is provided by the analysis in the previous section. With perfect international capital markets, capital flows will equalize effective capital-labor ratios. But this does not imply equalization of capital-labor ratios. This result, which follows directly from the analysis in the previous section, is stated in the next proposition. Note that this result does not give a complete answer to our question, since it takes productivity 757

differences across countries as given. Nevertheless, it explains how, given these productivity differences, there is no compelling reason to expect capital to flow from rich to poor countries.

PROPOSITION 19.4. Consider a world economy with identical neoclassical preferences across countries and free flows of capital. Suppose that countries differ according to their productivities, the Aj's. Then there exists a unique steady state equilibrium in which capitallabor ratios differ across countries (in particular, effective capital-labor ratios, the kj's, are equalized), and there are no capital flows across countries.

Proof. See Exercise 19.7. ?

This proposition states that there is no reason to expect capital flows when countries differ according to their productivities. The more productive countries will have higher capitallabor ratios. To the extent that two countries j and j0 have different levels of productivity, Aj (t) and Aji (t) > Aj (t), their capital-labor ratios should not be equalized, instead, country j0 should have a higher capital-labor ratio than j. Consequently, capital need not flow from rich to poor countries, because rich countries are more “productive”. This is in fact similar to the explanation suggested in Lucas (1990), except that Lucas also linked differences in Aj's to differences in human capital and in particular to human capital externalities. Instead, Proposition 19.4 emphasizes that any sources of differences in Aj's will generate this pattern.

The reader would be right to object at this point that this is only a “proximate” answer to the question, since it provides no reason for why productivity differs across countries. This ob jection is largely correct. Nevertheless, this proposition is still useful, since it suggests a range of explanations for the lack of capital flows from rich to poor countries that do not depend on the details of the world financial system, but instead focus on productivity differences across countries. We have already made some progress in understanding the potential sources of productivity differences across countries, and as we make more progress, we will start having better answers to the question of why capital does not flow from rich to poor countries (in fact, why it might sometimes flow from poor to rich countries).

19.2.2. Capital Flows under Imperfect International Financial Markets. It is also useful to note that there are other reasons, besides Proposition 19.4, why capital may not flow from poor to rich countries. In particular, it may be the case that the rate of return to capital is higher in poor countries, but financial market frictions or issues of sovereign risk may prevent such flows.

For example, lenders might worry that a country that has a negative asset position might declare international bankruptcy and not repay its debts. Alternatively, domestic financial problems in developing countries (which will be discussed in Chapter 21) may prevent or slow down the flows of capital from rich to poor countries. For whatever reason, if the international financial markets are not perfect and capital cannot flow freely 758from rich to poor countries, we may expect large differences in the return to capital across countries.

Existing evidence on this topic is mixed. Three different types of evidence are relevant. First, a number of studies, including Trefler’s (1993) important work discussed in Chapter 3 and recent work by Caselli and Feyrer (2007), suggest that differences in the return to capital across countries are relatively limited. These estimates are directly relevant to the question of whether there are significant differences in the returns to capital across countries, but they are computed under a variety of assumptions (in Trefler’s case, they rely on data on factor contents of trade and make a variety of assumptions on the impact of trade on factor prices; Caselli and Feyrer, on the other hand, require comparable and accurate measures of quality-adjusted differences in capital stocks across countries).

Second and somewhat in contrast to the aggregate results, a number of papers exploiting microdata, for example, summarized in Banerjee and Duflo (2005), suggest that the rate of return for additional investment in some firms in less-developed countries could be as high as 100%. Nonetheless, this evidence, even if taken at face value, does not suggest that there will be strong incentives for capital to flow from rich to poor countries, since it may be generated by within-country credit market imperfections. In particular, it may be that the rate of return is very high for a range of credit-rationed firms, but various incentive problems make it impossible for domestic or foreign financial institutions to lend to these firms on profitable terms.

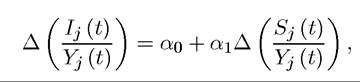

If these developing economies were to receive an infusion of additional foreign capital, the rate of return would not be given by the rate of return to credit-rationed firms, but by the rate of return to unconstrained firms, which is presumably much lower. Consequently, the incentives for capital to flow from rich to poor countries may be quite weak as suggested by Proposition 19.4.Finally, directly related to the issue of the flow of capital across countries is the evidence related to the Feldstein-Horioka puzzle. In an influential paper, Martin Feldstein and Charles Horioka (1980) pointed out a striking fact: differences in savings and investment rates across countries are highly correlated. In particular, Feldstein and Horioka used various different samples to run a regression of the form:

where. is the change in the investment to GDP ratio of country j between

is the change in the investment to GDP ratio of country j between

some prior date and date t, am is the change in the savings to GDP ratio.

is the change in the savings to GDP ratio.

Imagine that savings to GDP ratio varies across countries and over time because of “shocks” to the saving rate or other reasons. In a world with free capital flows, we would expect these changes in savings to have no effect on investment, thus we should estimate a coefficient of αι ≈ 0. In contrast, Feldstein and Horioka estimated a coefficient close to 1 (around 0.9)

for OECD economies. Similar results have been found for other samples of countries, though other studies, most notably Taylor (1994), argue that including additional controls removes the puzzle. Feldstein and Horioka and much of the literature that has followed them has interpreted the positive correlation between investment and savings as evidence against free capital flows. Naturally, in practice there are a number of econometric issues one needs to worry about before one can reach a precise conclusion. For example, Exercise 19.6 shows how correlation between investment and savings can arise without imperfections in international financial markets, when the major difference across countries is in investment opportunities. Nevertheless, the Feldstein-Horioka puzzle suggests that issues of sovereign risk might be important in practice and may create barriers to the free flow of capital across countries. Models incorporating endogenous sources of sovereign risk together with the process of economic growth could be an interesting area for future research.

19.3.

More on the topic Why Doesn’t Capital Flow from Rich to Poor Countries?:

- Why Doesn’t Capital Flow from Rich to Poor Countries?

- Contents

- Acemoglu D.. Introduction to Modern Economic Growth. Princeton University Press,2008. — 1248 p., 2008

- Table of contents