Journey of Money from Its Brief History to Internet

While it is so difficult to unite even on a general definition of money, arranging a detailed title on the history of money will drag the study into a scope beyond its purpose. Examining the studies in the literature about the history of money, it is observed that, on the one hand, generalizations involving the life and nature of human beings were put forward, and on the other hand, the positioning of money in various cultures and societies was discussed.

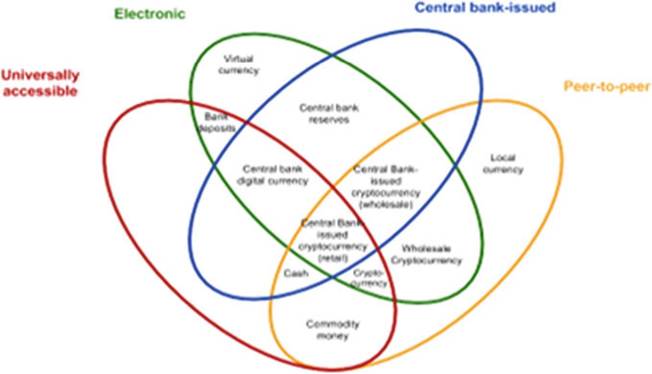

On the other hand, it was deepened by economic historians through statistics and general theories based on pure economics. Accordingly, the concept of money is not only seen as the transformation of any substance according to social acceptances throughout history, but also the ways in which this value is registered and the way in which the controlling sovereign power evolves according to its political purposes have been adopted in a broad perspective. In this respect, it will focus on certain milestones that will not harm the purpose of the study, but will facilitate the understanding of the transition to electronic-based currencies (Fig. 11.1).

Fig. 11.1 Money flower: a taxonomy of money. Source Bech and Garratt (2017)

11.3.1 The Order Before Money

The value represented by money can be described as abstract and concrete. In concrete terms, it is important which materials that the money is made of. There are many types from various mines to electronic form nowadays, with the development and spread of technology (see Bech and Garratt 2017). The enormous increase in the rate of use over time also adds new functions of money (promoting economic activities, redistribution of income, etc.). In an abstract evaluation, the principle of acceptability and trust in money are manifested itself in society (s) and, today, even in the global framework.

The fact that these and many similar variations increase by changing over time leads to the conclusion that money should not be limited to a single definition as it is always dynamic and adapt to the environment and period in which it is accepted.Ludwing von Mises’ book “The Theory of Money and Credit”, first published in 1912, explained the situations where money is not needed by the individual and/or society by stating: “Money is not a need where there is no free exchange of goods and services. At the same time, if the production and consumption of only local resources take place in the same household in a society, money becomes an unnecessary phenomenon as much as what it expresses to an individual living in isolation from society. Moreover, even in an economic order based on division of labour, money would still be unnecessary if the means of production were socialized, control of production and distribution of finished products were in the hands of a central body and individuals were not allowed to exchange their allocated consumer goods for consumer goods allocated to others. The phenomenon of money foresees an economic order in which production is based on the division of labour and private property is formed not only in first order goods (consumer goods) but also in goods of higher orders (goods of production)” (Mises 1954).

The Exchange System, which is one of the most primitive financial systems, provided the functioning of economic life before trade and the use of money. Our distant ancestors wanted to exchange the excess they had and get other things they needed. However, this system has encountered a bottleneck over time. It was not always easy to find what you want and someone who is looking for what you have, in the right amounts, in return for what you want. As a solution, some objects were considered markers that most people would be willing to trade for something else in the future. At first, salt or ox skins were examples of such a practice; over time some metals were used, because these metals were scarce, useful, durable, portable and divisible.

In general, in everyday life “Money” succeeded because it fulfilled the superior exchange function, valued not only as a commodity in itself but also as a ready-made medium of exchange (Hart 2005).Although it is not at the forefront of the financial system, exchange trade somehow continued to exist in the background. However, it would not be rational to think of this system as independent from technology today, at least in countries where technology is advancing. When we think that the states are now in collective exchange of technological progress and even ideas in some communities (Digital Nations), it is not an assumption that they adapt to the new order and survive as was the case in history. One-way interactions with the digital transformation of individuals (Peer to Peer, P2P), companies (Business to Business, B2B) and governments (Government to Government, G2G) will be the trigger for this adaptation (Table 11.1).

Table 11.1 Digital development of the government phenomenon

| Gov 1.0 | Gov 2.0 | Gov 3.0 | |

| Main goal | Better services | Openness and collaboration | Societal problem solving, citizen well being, optimization of resources |

| Main method | Connected governance | Open and collaborative governance | Smart governance |

| Usual application level | National | National and local | Local to international |

| Key tool | Portal | Social media | Ubiquitous smart services/devices/apps |

| Key obstacle/risk | Public sector mentality | Public sector mentality | Public sector mentality |

| Key ICT (information and communication technology) area | Infrastructures and organisation | People and data | Machine intelligence and IoT (Internet of Things) |

| Most needed discipline, beyond ICT | Management | Sociology | Everything |

Source Charalabidis (2015)

As a pre-money system, the Gift Economy is considered as a sub-branch of the economy.

However, this concept is put forward to refute the planned economy, which believes that human behaviour is a result of rational calculations. The gift economy refers to the providers of goods or services that do not have a clear expectation of what to return or what they expect to return. There are many sharing behaviours based on non-standard habits. At the same time, giving and receiving gifts has turned into an unspecified obligation, creating a confidential relationship between buyer and seller.11.3.2 Commodity (Good) Money and Shifting to Paper

Money

With the spread of Commodity Money and the development of trade and productivity over time, people immediately needed a tool for change that they could widely use. The exchange tool to meet these requirements should not be relatively difficult to obtain, not easy to damage and rot, easy to process and suitable for payment in a variety of sizes. After people tried various items, almost all civilizations in the world chose two metals as “money”: gold and silver. It is difficult to obtain gold and silver; they are suitable mines due to their relatively soft and easy-to-cut properties, although they are not easy to destroy.

In the economy, if the objects used as money are related to other uses as well as their properties as goods, the commodity monetary system is considered to be in place in that economy. This system developed spontaneously and there is no state intervention at any stage of development. At this point, another issue is that paper money may be mistaken for commodity money. The commodity value of a piece of paper used as money is much lower than its value as money. In other words, the value of paper money has taken on a different quality by completely separating it from its essence. In this case, the monetary value included in the commodity money definition is valid for goods with equal relative values as goods (Parasiz 2013).

The first examples of Paper Money have a history dating back to the seventh century, the Tang Dynasty in China.

That its actually active use developed in the Song Dynasty in the eleventh century is the prevalent view in the sources. It is accepted that it later spread to China and the Mongol Empire through the Yuan Dynasty. The recognition of this system by Europe dates back to the thirteenth century, when explorers like Marco Polo mentioned it in their travel notes.Although the origin of paper money is considered to be China, it was mentioned by the Lombards in the West. Lombards, of Italian origin, spread all over Europe and became bankers who kept the money of those dealing with trade. The functions these bankers have undertaken over time roughly summarize the development of paper money. These bankers, who facilitate trade significantly, have credited or debited these accounts according to the trade between merchants through the checking accounts they open for their customers.

In this process, turnover transactions emerged for the first time. Subsequently, deposit transaction, lending to custody money against interest, certificates with the statement of immediate payment in case of debt instead of coins, and finally, as some of the certificates issued and released to the market were returned, debt certificates were started to be issued on the deposits they consigned, and the foundation of modern banking was laid (Paya 2013).

The origin of banknotes in their current form is based on the certificates of gold and silver coins accumulated in gold and silversmiths (goldsmith-bankers), in the example of England, where the origin of the banknotes is not so independent from commodity currencies. London’s first bankers are these goldsmiths. Goldsmiths eagerly embraced the banking role. The first goldsmith’s certificate for precious metal deposits was issued in 1633 by the goldsmith Lawrence Hoare. However, most of the wealthy merchants kept their commodity money in the mint located in the Tower of London. When King Charles I seized £ 200,000 worth of commodity money in 1640, trust in the state was lost and wealthy merchants turned to goldsmiths.

This event is considered as a historical event in terms of acting like a bank.As a result, the position of paper money became one of the instruments of intervention in government-run markets. The amount of paper money used by individuals in the market as a medium of exchange and the amount of “cash” along with the coins has become a very small part of the total money offered over time. The amounts that are created as bank money which are only included in the bank records started to quit being the equivalent of a precious metal, which is the logic of paper money’s emergence, and created its own identity with the trust mechanism; it began to turn into bank money, first in bank books and then on computer screens.

11.3.3 Electronic-Digital-Virtual Confusion and Plastic Period

Increasing dependence on machines, especially computers, has led to significant social effects. A generation ago, computers were cumbersome but were built-in tools for data computing and word processing; that is, it was not found in every workplace or home. Today, computers can be accessed everywhere, from mainframes computers to smart phones, from desktop computers to laptops and even from visible to invisible technology, and today’s computers are intelligent machines powered by artificial intelligence. Thanks to the high-speed connection and Internet, anyone with a computer or a smart phone can access information, services and entertainment in many parts of the world. In summary, just as people changed computers, computers changed people (Lin 2013).

Expectations from the digital system come to the fore in areas such as data storage, processing speed and accessibility. There is an uninterrupted digital revolution in the global economy. According to a recent study, this amount, called the global data sphere, will increase from 16.1 trillion gigabytes in 2016 to 163 trillion gigabytes

Table 11.2 Money matrix

| Form | |||

| Physical | Digital | ||

| Legal status | Irregular | Some local currencies | Virtual currencies |

| Regular | Banknotes and coins | Digital currencies | |

| Deposit account in commercial banks | |||

Source European Central Bank (2012)

(163 Zettabytes) by 2025. This tenfold increase will encompass data held everywhere from cloud systems to handheld devices (Zhang 2018). This means that the pool, which includes from personal data to the private sector and even government data, is now transferred from the physical environment to the digital environment.

Today, payment cards are a more preferred method than cash payment system, through a bank deposit or credit account. Being individually configurable, they make it possible to pay, transfer and split into instalments the high amounts via a small plastic card. Despite the presence of sub-types that serve many purposes, debit card and especially credit card are the prominent payment cards. These plastic cards, which became more popular towards the end of the twentieth century, started with telephone lines, which were the minimum technological need in this period, and the use of the blessings of the Internet in the data sharing of mass media in the twenty- first century and its spread to wider circles expanded the usage areas of payment cards (Table 11.2).

When looking at the equivalents used in the literature regarding the concept of digital money, it is possible to see that electronic (electronic money, electronic currency, e-money) expressions are also preferred in some studies. However, in a wider perspective, as a result of a detailed research, it was observed that there were small differences between the phenomena represented by each concept. Electronic money refers to a certain amount of cash or deposits received and given from a financial institution through the fast payment service initiated by banks and third parties through the use of certain electronic channels (credit cards, etc.). It turns out that digital currencies, unlike electronic money, are not based on bank money and are created completely independently in the digital environment. The most important criterion they expressed in general terms, be it the concept of digital or electronic money, is that money has undergone a new change.

11.4

More on the topic Journey of Money from Its Brief History to Internet:

- THE TECHNOLOGY MUDSLIDE HYPOTHESIS: SUSTAINING INNOVATION VS. DISRUPTIVE INNOVATION

- THE THEORY AND PRACTICE OF EMPIRE-BUILDING

- Ever the Twain Shall Meet, 1830–1900

- La debrouille: A Dominant Approach to Coping in the Kivus

- References

- Model Test Paper (Base on the Latest Online Pattern)

- C Why PPV Is Higher with Hypothesis-Based Research

- New fiqh created

- XAT 2011

- Banerjee Abhijit V., Duflo Esther. Good Economics for Hard Times. PublicAffairs,2019. — 403 p., 2019