Maturity level of Good Corporate Governance (GCG) principles implementation - Case study from micro and small enterprises in Bandung

C. T.L. Soei, A. Setiawan, K. Fitriani & R. Satyarini

Parahyangan Catholic University, Bandung, Indonesia

ABSTRACT: This study investigates the maturity level of Good Corporate Governance implementation in micro and small enterprises in Bandung.

We first identified five major good corporate governance indicators to implementation of good corporate governance principles. We then used maturity model to measure the success rate of good corporate governance implementation in micro and small enterprises. The first result of this study is maturity level as a map to assess the good corporate governance implementation. The next result indicates that micro and small enterprises in Bandung focus on fairness. The reason micro and small enterprises in Bandung focus on fairness is the unawareness of informal business of doing business with standard. These results indicate the need to improve micro and small enterprises’ awareness of the importance of good corporate governance implementation to have sustainability of doing business.1 INTRODUCTION

Good corporate governance becomes a hot topic since the 1998 economic crisis. One of the main causes is the implementation of bad corporate governance. Corporate governance is one of the best practices that ensures the company is properly directed, managed and monitored to achieve the company’s objectives. The purpose of corporate governance is to create a balance among shareholders, directors, and management by increasing shareholder value and protecting the interest of stakeholders (Alnaser et al. 2014). For investors, one of the most important aspects when making investment decisions is the application of corporate governance principles and the company’s profit to ensure the return on investment (Todorovic 2013).

Since the Asian crisis, Asian countries have sought to introduce corporate governance guidelines to direct companies to improve their best corporate governance practices.

However, corporate governance has not been accepted by most companies in Asia. In Indonesia, during the economic crisis in 1997, the value of the currency depreciated by 80% and many companies in the banking sector went bankrupt. One of the main causes is the implementation of bad corporate governance (Susanty et al. 2013).Good governance practices in corporate listed in the Indonesia capital market is necessitated in order to increase Indonesian position in the international rating regarding governance implementation as a reference for the practice of a good governance system, which the National Committee on Governance Policy (KNKG) refers to the principles issued by the OECD. KNKP established a regulation for public companies to put the application of GCG in the annual reports. The application of GCG in public companies became a must. Corporate governance is a series of corporate control activities involving management, board members and stakeholders in order to encourage the creation of an efficient, transparent market and a high compliance with the laws and regulations (KNKG 2006).

Micro, Small and Medium Enterprises (MSMEs) have contributed more than 50% to Indonesia GDP. MSMEs are sole proprietorship business entities that strive for corporate governance in accordance with the principles of good corporate governance. At present, there have not been many studies that assess the application of good corporate governance to small and medium enterprises because since good corporate governance is commonly applied to large companies. Good corporate governance will be important to an MSME provided that the company expands into a larger scale business. The company needs good corporate governance to increase shareholder values and interests of stakeholders. (Alnaser et al. 2014). Therefore, it is important to know whether MSMEs apply the principle of GCG. The study was conducted on micro and small enterprises in Bandung. The research questions were:

RQ#1: How is the implementation of the maturity model in assessing the company’s good corporate governance?

RQ#2: How is the maturity level of the implementation of good corporate governance in small and medium enterprises?

2 LITERATURE REVIEW

2.3 Micro, small and medium enterprises

2.1 Goodcorporategovernance

Corporate governance is a process and structure as a basis for all members of the company to take action to protect the interests of stakeholders (Ehikioya 2009).

Corporate governance can be seen from two points of view, behavior and normative (Cosneanu et al. 2013). Corporate governance from behavioral perspective is related to company interactions with stakeholders, and corporate governance from normative perspectives is related to regulation regulating this relationship (Cosneanu et al. 2013). Behaviors related to corporate governance include structures and processes or mechanisms. The corporate governance structure relates to the company’s ownership structure (Ehikioya 2009), including the composition, expertise, independence and size of the board of commissioners. In addition to the board of commissioners, the corporate governance structure also includes two basic ownership structures, namely concentrated or scattered (Ehikioya 2009). In developed countries, company ownership structure is scattered. However, in developing countries, where investor protection systems are weaker, company ownership structure is usually concentrated (Ehi- kioya 2009).Corporate governance can consist of formal and informal mechanisms. Formal mechanisms are based on formally defined structures and processes, while informal mechanisms arise in relation to culture and values that are influenced by the organization’s leaders. Organizational governance systems vary depending on the size and type of organization and the environmental, economic, political, cultural and social conditions in which the organization operates (ISO/ TMB Working Group on Social Responsibility 2010).

The principles of good corporate governance in Indonesia are based on 5 principles of corporate governance, namely (1) transparency, (2) accountability, (3) responsibility, (4) independence, and (5) fairness (KNKG 2006). One of the implementations of this transparency principles is to carry out adequate company disclosures about corporate governance and other important information. The information disclosed must be in accordance with the needs of the stakeholders.

2.2 Maturity model

Maturity model is a model developed by Software Engineering Institute to assess the capability of information system applications in a company (Visconti & Cook 1998). In 2007, ISACA implemented this model maturity in COBIT 4.1 by conducting a benchmark maturity model and applied to the performance assessment and information technology processes in the company (IT Governance Institute 2007).

Micro enterprises are productive business owned by private company or business entity that has net assets of no more than IDR 50,000,000 excluding lands and business premises. Usually micro enterprises have not even carried out simple financial administration. They do not separate family finances from business finance (Bank Indonesia, 2015).

Small enterprises are productive businesses owned by companies or individual business entities that have net assets more than Rp. 50,000,000.00 excluding lands and buildings of business premises. In addition, usually small businesses have better management and organization, with a clear division of tasks, among others, finance, marketing and production (Bank Indonesia 2015).

One characteristic of micro and small enterprises is insufficient knowledge related to business management due to numbers of employees and managerial experience (Oliveira et al. 2014). Oliveira et al. (2014) concluded the application of knowledge management to small and medium enterprises is often difficult due to insufficient of documentation. It can analogously be assumed the implementation of good corporate governance is also often difficult due to documentation problems.

3 METHODOLOGY

The population of this study is Micro and Small Businesses in the Bandung. We choose 4 micro and small enterprises using a purposive sampling technique that met the criteria for micro and small businesses and the willingness to involve in this study.

The questions for each GCG principle were formulated based on previous literature with some adjustment.

Each question was answered using maturity scale to know maturity level. Semi-structured interviews were conducted with 4 owners of micro and small enterprises to determine the maturity level of each GCG principle. The data obtained from interviews and observation were processed qualitatively. After then, we did mapping using MS Excel to analyze the result.4 RESULTS AND DISCUSSION

4.1 The implementation of maturity model in assessing the company’s good corporate governance

The maturity model was implemented by mapping the five principles of good corporate governance in measurement in maturity models (non-existent, initial, repeatable but intuitive, defined, managed and measurable, and optimized). This mapping was done by making indicators for each of the principles of good corporate governance and making measurements to reflect each score in the maturity model.

Indicators for each principle were made to identify the measurement of the application of each principle of good corporate governance in the company. For small and medium enterprises, according to the objectives in this study, indicators were designed as follows:

1) Transparency (T): an assessment was made for the availability of information, including clarity, accessibility, accuracy, socialization and timeliness. However, an assessment was also carried out for the ability to maintain information confidentiality.

2) Accountability (A): an assessment was made for the company’s accountability to employees, interested parties, the surrounding environment and the country.

3) Responsibility (R): an assessment was made for the clarity of tasks and responsibilities, the availability of business ethics standards, compliance with regulations and performance appraisal.

4) Independence (I): an assessment was made for freedom from the influence of outside parties in carrying out company operations.

5) Fairness (F): an assessment was made for the implementation of fairness for company stakeholders.

Based on indicators for each good corporate governance principle, the score is assigned to the application in the company. The scoring system applied in this study were: (1) inadequate application, meaning that the application of GCG principle is poorly applied, (2) basic application, meaning that the application of GCG principle is applied at a minimum effort, (3) adequate application, meaning that the application of GCG principle is applied well, (4) effective application, meaning that the application of GCG principle is effectively applied in daily life, and (5) the application of the lead, meaning that the application of GCG principle is applied so it can help company create a proactive solution. In each score for each indicator, the status of implementing good corporate governance principle was made. After the interviews, the results of GCG indicator were interpreted into maturity level. The result of the mapping can be seen in Table 1.

4.2 The maturity level of good corporate governance implementation in small and medium enterprises

Based on the characteristics of small and medium enterprises according to (Oliveira et al. 2014), there are limitations in the application of normal

Table 1. Comparison table of good corporate governance principles application.

| Principles | MSME 1 | MSME 2 | MSME 3 | MSME 4 | Average |

| T | 3.85 | 2.71 | 2.57 | 3 | 3.03 |

| A | 3.25 | 2.25 | 2.25 | 3.25 | 2.75 |

| R | 2.5 | 2.5 | 2.25 | 3 | 2.56 |

| I | 2.5 | 3 | 2.5 | 3 | 2.75 |

| F | 4 | 3 | 2.67 | 3.67 | 3.33 |

procedures, namely documentation and socialization, so this research was conducted to assess the implementation of good corporate governance in small and medium enterprises. However, based on previous research, the existence of good corporate governance in small and medium enterprises is still rarely studied because good corporate governance is commonly applied to large companies, especially companies that go public and must account for the management of the company to the company holders.

Table 1 shows the mean score of GCG principles (TARIF). The table also reveals the score for each MSME. Based on the data, fairness is the highest score among all principles.

Data from Table 1 is mapped into radar analysis using MS Excel. The result can be seen in Figure 1. It was found the principle with the greatest value was fairness, while the one with the smallest value was accountability. This is not surprising because MSMEs are managed and supervised directly by the owners.

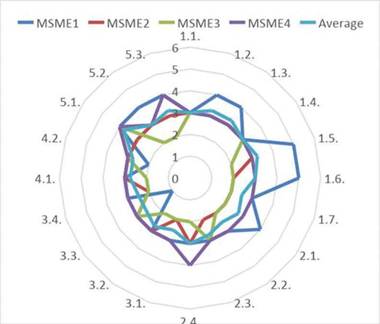

Figure 2 shows the detailed mapping for each indicator of each GCG principle. In MSME 1, transparency obtained the highest point. Fairness obtained the highest score in MSMEs 2, 3, and 4. Figure 2 also shows that there were 20 indicators consisting

Figure 1. Maturity model - good corporate governance (by principles).

Figure 2. Maturity model - good corporate governance in detail.

of 7 transparency indicators, 4 accountability indicators, 4 responsibility indicators, 2 independence indicators, and 3 fairness indicators.

5 CONCLUSION

To conclude, most micro and small enterprises have applied some of GCG principles well. The limitation of this study is that the results obtained cannot be generalized due to its case specific context. However, this is only a preliminary research. In further research, we want to expand the sample size and also want to know the factors that can affect application of GCG principles.

References

Alnaser, N., Shaban, O. S. & Al-Zubi, Z. 2014. The Effect of Effective Corporate Governance Structure in Improving Investors’ Confidence in the Public Financial Information. International Journal of Academic Research in Business and Social Sciences 4(1): 556-570.

Cosneanu, S., Russu, C., Chiritescu, V. & Badea, L. 2013. Foundations and Principles of Corporate Governance. Valahian Journal of Ecionomic Studies: 31-38.

Ehikioya, B. I. 2009. Corporate governance structure and firm performance in developing economies: evidence from Nigeria. Corporate Governance: 231-243.

ISO/TMB Working Group on Social Responsibility. 2010. ISO/FDIS 26000 - Guidance on Social Responsibility. Geneva: The International Organization for Standardization.

IT Governance Institute. 2007. COBIT 4.1. Illinois: ISACA.

Komite Nasional Kebijakan Governance (KNKG). 2006. Pedoman Umum Corporate Governance Indonesia. Jakarta: Komite Nasional Kebijakan Governance.

Oliveira, M., Pedron, C. D., Nodari, F. & Ribeiro, R. 2014. Knowledge Management in Small and Micro Enterprises: Applying a Maturity Model. Porto Alegre: Ponti- fιcia Universidade Catolica do Rio Grande do Sul.

Susanty, A., Suprayitno, G. & Jie, F. 2013. Preliminary Study The Relationship Between Organizational Culture and Implementation of Independence Principle: Indonesia Public Listed Company Case Study. International Journal of Information, Business and Management 5(1): 60-73.

Todorovic, I. 2013. Impact Of Corporate Governance On Performance Of Companies. Montenegrin Journal of Economics: 47-53.

Visconti, M. & Cook, C. R. 1998. Evolution of a maturity model - critical evaluation and lessons learned. Software Quality Journal: 223-237.

More on the topic Maturity level of Good Corporate Governance (GCG) principles implementation - Case study from micro and small enterprises in Bandung:

- Return on selling before maturity

- Abdullah A.G., Widiaty I., Abdullah G.U. (eds.). Global Competitiveness: Business Transformation in the Digital Era. Routledge,2019. — 325 p., 2019

- Table of contents

- Duration if the term to maturity is lengthened

- Article 4.1 Global corporate bond issuance at lowest level in five years

- Yield to maturity versus rate of return

- Small peoples.

- Corporate Judgment and Restraint

- Legal Provisions and their Implementation

- Religious life at the popular level