Financial development and the effect of volatility on growth

Let us augment the model of short- versus long-term investment developed in Section 1.3 of the previous chapter by introducing credit market imperfections. Thus, we assume that upon investing in short-run capital and in long-term investments, an entrepreneur born at date t can borrow only up to m times his or her initial wealth, so that he or she faces the investment constraint

where μ = 1 + m.

of credit constraints and as we might have expected, zt falls with either a reduction in μ or an increase in φ.

Using the fact that

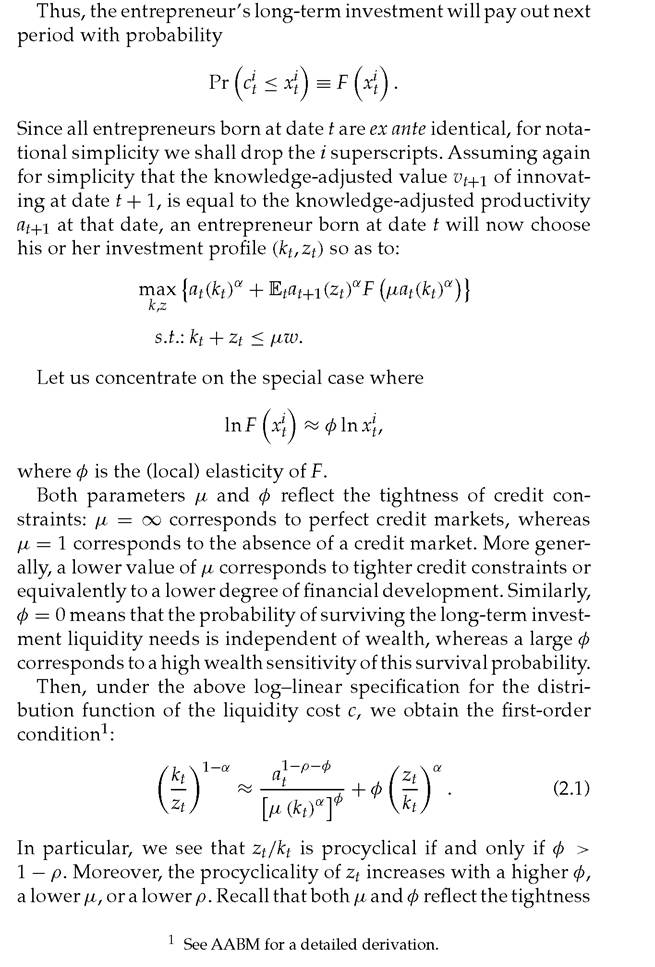

in equilibrium (in the absence of foreign lending or government bonds, and given that all entrepreneurs are ex ante identical with the same initial wealth so that there is no reason why one entrepreneur would end up lending to another entrepreneur in period t), we thus conclude that under sufficiently incomplete markets, the share ofR&D zt becomes procyclical, and the share of capital investment kt becomes countercyclical. Long-term investment zt is less procyclical the less tight the credit constraints, less persistent the shocks, or longer the horizon of long-term investment.

The intuition for why long-term investment becomes more procyclical when credit constraints are tighter, can be explained as follows: under tight credit constraints, a low realization of current productivity at means low level of profits at(kt)α at the end of the current period.

But, under tight credit constraints, this in turn implies a low borrowing capacity and therefore a low ability to respond to the liquidity shock c on the long-term investment, and therefore it makes it very unlikely that the long-term investment today at date t will pay out in the future. Anticipating this, an entrepreneur facing a low productivity shock today will shy away from long-term investment, hence the procyclicality of long-term investment under tight credit constraints.The above reasoning also implies that the tighter the credit constraint, the more risky it is to invest in long-term investments in general, therefore the lower the mean long-term investment over time, and consequently the lower the average growth rate.

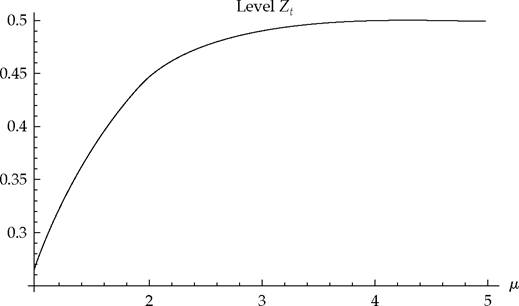

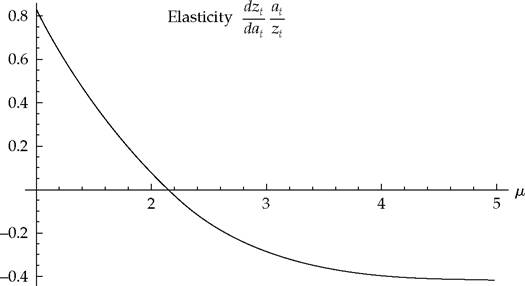

Example 1: The following two figures show how credit constraints affect the level and procyclicality of long-term investment. Here, we assume that the distribution of c is lognormal. We also assume that α = 1 /3, and we let μ vary between 1 (no credit) and 5.

Figure 2.1 depicts the equilibrium level of zt, evaluated at the mean productivity level (at = 1). Figure 2.2 depicts the equilibrium

Fig. 2.1 The effect of incomplete markets on the level of long-term investment.

Source: AABM (2004), figure 2.

Fig. 2.2 The effect of incomplete markets on the cyclical elasticity of long-term investment.

Source: AABM (2004), figure 3.

cyclical elasticity of zt (also evaluated at at = 1). In particular, we see that for μ sufficiently small, zt is increasing in at ((dzt/dat) > 0): In other words, long-term investment becomes procyclical when μ is small and becomes countercyclical for μ sufficiently large.

We now turn our attention back to the effect of increased volatility on long-run average growth, and how it is affected by credit constraints.

In the economy with credit constrained firms, by the law of large number only a fraction,

of entrepreneurs will successfully meet the liquidity needs of longterm investment.

Now if we assume that knowledge grows at a rate proportional to the number of implemented (i.e. completed) innovations, then the growth rate of technology is now given by:

where z(at) is the (incomplete-markets) equilibrium level of longterm investment. Recall that in the absence of credit constraints (see Chapter 1) we simply had

since all innovations were always completed.

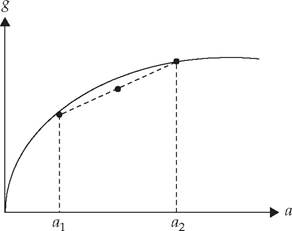

In fact, one can show that (z(at))αδ(at) is always concave in at under the Cobb-Douglas long-term investment technology considered in this chapter. Thus, the growth rate gt is a concave function of at, and therefore mean growth will now fall in response to an increase in the variance of at (see Figure 2.3). Thus, in an economy with credit-constrained firms, an increase in volatility will result in lower mean growth.

Example 2: Assume linear production and long-term investment technologies, namely:

Suppose also that the long-term growth-enhancing investment is indivisible, equal to some Zo ∈ (0, w), that the distribution for the liquidity shock”? is uniform over the interval [0,1], and that in the absence of volatility, firms could always pay? with their retained earnings from short-run production, more precisely:

where a is the average productivity shock.

Fig. 2.3 Growth rate under Cobb-Douglas long-term investment technology.

Note: If we randomize between aj and a2, the average growth rate lies strictly below the curve.

We are interested in the effect of increased macroeconomic volatility (i.e. of increased variance of a, denoted by σ) on the expected growth rate

where

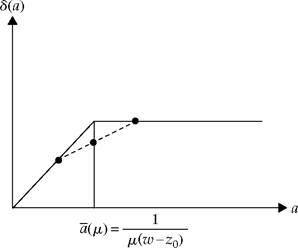

Since the liquidity shock is uniform, we have:

which is obviously concave in a. Figure 2.4 shows δ (a) as a function of a. In particular we see that randomizing between two values of a below and above the kink can only reduce the average δ so that volatility is unambiguously detrimental to average growth.

It then immediately follows that the expected growth rate g must decrease when the variance of a increases, and all the more when μ is lower. This result is quite intuitive: more volatility does not improve firms' ability to overcome the liquidity shock in a boom since firms already do it without volatility. However, it reduces the probability that they will overcome the liquidity shock in a slump, and to a larger extent when the firm faces tighter borrowing

Fig. 2.4 Volatitlity is detrimental to average growth.

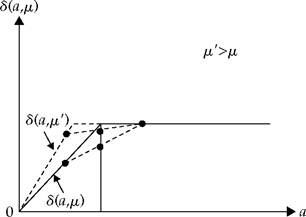

Fig. 2.5 Increased access to credit reduces the sensitivity of growth to productivity shocks.

constraints. We thus have:

Moreover, the ex post growth rate,

is increasing and concave in a, but becomes constant and equal to λzo when μ is sufficiently large.

Thus growth reacts positively to favorable productivity shocks and at the same time more volatility is detrimental to growth. Now, Figure 2.5 depicts δ(a) = δ(a,μ) for two values of μ, namely μ and μ' > μ. We see that a negative shock on a has a less detrimental effect for μ' than for μ.Thus, increased access to credit (a higher μ) reduces the sensitivity of growth to productivity shocks and also the extent to which volatility is detrimental to growth (since growth becomes less concave in a).

2.1.1 Main theoretical predictions

To complete this section we list our main predictions as they emerge from our above discussion:

1. Long-term investment tends to be countercyclical in the absence of credit constraints, but becomes increasingly procyclical as credit constraints tighten.

2. When firms face tighter credit constraints, the effect of volatility on expected average growth tends to become more negative (or less positive).

3. When firms face tighter constraints, growth becomes more sensitive to exogenous shocks.

2.2

More on the topic Financial development and the effect of volatility on growth:

- Volatility of bond returns

- Nutrition is a dynamic process to supply adequate nourishment for survival, growth and development, repair and creation of future reserves.

- We argued in Chapter 0 that credit constraints are an important part of life, especially in the developing world. In this chapter we argue, based on Aghion-Angeletos-Banerjee-Manova (AABM), that the presence of credit constraints can help us understand why volatility is so costly for growth.

- Endogenous volatility and amplified shocks

- In the previous chapters we have focused on the effects of aggregate volatility and aggregate productivity or trade shocks on long-run growth, taking volatility as being largely exogenous.

- Towardamacropolicyofgrowth

- Empiricalanalysis

- Conclusion

- Financial development and economic growth: Theory

- Contents