STATEMENT OF CASH FLOWS RATIOS

Ratios related to sources and uses of funds measure credit quality at the most elemental level—a company’s ability to generate sufficient cash to pay its bills.

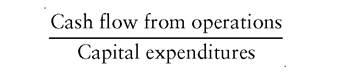

These ratios also disclose a great deal about financial flexibility; a company that does not have to rely on external financing can take greater operating risks than one that would be forced to retrench if new capital suddenly became scarce or prohibitively expensive. In addition, trends in sources-and- uses ratios can anticipate changes in balance-sheet ratios. Given corporations’ general reluctance to sell new equity, which may dilute existing shareholders’ interest, a recurrent cash shortfall is likely to be made up with debt financing, leading to a rise in the total-debt-to-total-capital ratio.For capital-intensive manufacturers and utilities, a key ratio is cash flow to capital expenditures:

The higher this ratio, the greater the financial flexibility implied. It is important, though, to examine the reasons underlying a change in the relationship between internal funds and capital outlays. It is normal for a capital-intensive industry to go through a capital-spending cycle, adding capacity by constructing large-scale plants that require several years to complete. Once the new capacity is in place, capital expenditures ease for a few years until demand growth catches up and another round of spending begins. Over the cycle, the industry’s ratio of cash falls. By definition, the downleg of this cycle does not imply long-term deterioration in credit quality.

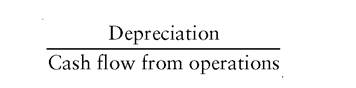

In contrast, a company that suffers a prolonged downtrend in its ratio of cash flow to capital expenditures is likely to get more deeply into debt, and therefore become financially riskier with each succeeding year. Likewise, a rising ratio may require interpretation. A company that sharply reduces its capital budget will appear to increase its financial flexibility, based on the cash-flow-to-capital-expenditures ratio. Cutting back on outlays, however, may impair the company’s long-run competitiveness by sacrificing market share or by causing the company to fall behind in technological terms.Although the most recent period’s ratio of cash flow to capital expenditures is a useful measure, the credit analyst is always more interested in the future than in the past. One good way of assessing a company’s ability to sustain its existing level of cash adequacy is to calculate depreciation as a percentage of cash flow:

Unlike earnings, depreciation is essentially a programmed item, a cash flow assured by the accounting rules. The higher the percentage of cash flow derived from depreciation, the higher is the predictability of a company’s cash flow, and the less dependent its financial flexibility on the vagaries of the marketplace.

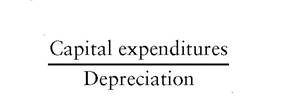

Finally, among the ratios derived from the statement of cash flows is the ratio of capital expenditures to depreciation:

A ratio of less than 1.0 over a period of several years raises a red flag, since it suggests that the company is failing to replace its plant and equipment.

Underspending on capital replacement amounts to gradual liquidation of the firm. By the same token, though, the analyst cannot necessarily assume that all is well simply because capital expenditures consistently exceed depreciation. For one thing, persistent inflation means that a nominal dollar spent on plant and equipment today will not buy as much capacity as it didwhen the depreciating asset was acquired. (Technological advances in production processes may mitigate this problem because the cost in real terms of producing one unit may have declined since the company purchased the equipment now being replaced.) A second reason to avoid complacency over a seemingly strong ratio of capital expenditures to depreciation is that the depreciation may be understated with respect either to wear and tear or to obsolescence. If so, the adequacy of capital spending will be overstated by the ratio of capital spending to depreciation. Finally, capital outlays may be too low even if they match in every sense the depreciation of existing plant and equipment. In a growth industry, a company that fails to expand its capacity at roughly the same rate as its competitors may lose essential economies of scale and fall victim to a shakeout.