Financial institutions and markets

All modern, developed economies have a sophisticated financial system which incorporates both the financial institutions and financial markets. These institutions and markets exist to mediate between those who wish to save or lend and those who wish to borrow or invest.

Mediation is necessary because lenders and borrowers have different needs in terms of maturity, liquidity and yield.Lenders can be expected to prefer to lend for a short term before the loan matures, to get their money back quickly if their own need for liquidity changes, and to receive high returns on their loans. Borrowers can be expected to prefer to borrow over the long term and to offer low returns, though sharing the same desire for liquidity.

The whole process of matching the needs of lenders and borrowers is known as ‘financial intermediation’ and the institutions which play a part in this process are known as ‘financial intermediaries’. Financial markets also play a key role in this system by allowing borrowers to issue IOUs such as bills or bonds which are acceptable to lenders and which can be traded on the secondary markets (i.e. markets dealing in securities which already exist).

The whole financial system is continually undergoing rapid development and since the 1990s financial markets have become ever more complex, offering new types of financial instruments which reduced transactions costs and were more flexible and better targeted. At the same time, the traditional roles of the financial institutions have become increasingly blurred and, as their operations evolved, they were laying the foundations for the largest financial crisis to hit the UK financial system (see also Chapter 20 and Chapter 30).

I The role of the financial system

The basic rationale of a financial system is to bring together those who have accumulated an excess of money and who wish to save with those who have a requirement to borrow in order to finance investment.

This process arguably helps to better utilize society’s scarce resources, increase productive efficiency and ultimately raise the standard of living. Santomero and Babbel (2001) have usefully summarized this role of the financial system:Without a developed financial system, institutions, firms, and households would be forced to operate as self-contained economies. As a result, they could not save without deploying their resources somewhere, and they could not invest without saving from their own current output. A financial system allows trade between individuals to accomplish both these ends. It allows savers to defer consumption and obtain a return for waiting. Likewise, it permits investors to deploy resources in excess of those that they have available from their own wealth in order to gain the productivity that such investment yields. The economy also gains from the financial system, as both households and firms advance the economy, total output, and economic growth.

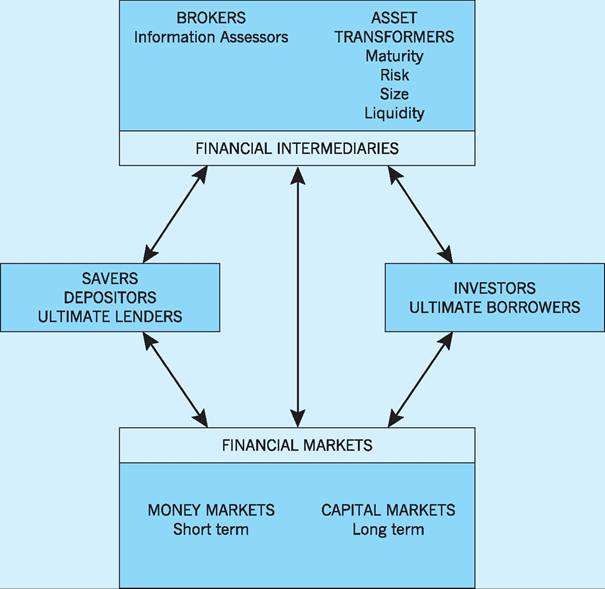

Figure 21.1 provides an overview of the structure of the financial system in the UK. Essentially there are three kinds of operator in the UK financial system.

1 Lenders and borrowers, including persons, companies and government. Lenders are also referred to as savers, depositors or ultimate lenders and borrowers as investors or ultimate borrowers.

2 Financial intermediaries, consisting of financial institutions which act as intermediaries between lenders and borrowers. Financial intermediaries take one of two general forms: brokers (bringing together lenders and borrowers by evaluating market information) and asset transformers (transforming the financial assets of lenders by varying the maturity, risk, size and liquidity of the liabilities of borrowers).

Fig. 21.1 The financial system.

3 Financial markets, where money is lent and borrowed through the sale and purchase of financial instruments.

They play an essential role in reducing the cost of placing, pricing and trading such instruments. In the UK, the financial markets can be defined as short-term money markets and longterm capital markets.The chapter will now consider in more detail the working of the financial system in the UK, beginning with the various financial instruments that are traded.

Financial claims

Operators within a financial system are essentially buying and selling paper IOUs in the form of financial claims. They are issued by those wishing to borrow and bought by those wishing to lend; lenders then hold a financial claim on the future income of the issuing company or person. Financial claims can be split into financial assets and financial liabilities. The purchaser of a claim holds it as a financial asset, whereas the issuer of the claim holds it as a financial liability.

An obvious example of a financial asset held by most people is a bank deposit account. The depositor holds a financial claim on the bank; and the bank, the borrower of the funds, holds a financial liability. Financial claims can take many forms, which are given the generic name financial instruments.

Characteristics of financial instruments

Financial instruments are classified according to various characteristics, the most important being the level of risk, liquidity and maturity. Other means of classification may also be used, for example between those instruments that can be traded by third parties (e.g. Treasury bills) and those that cannot (bank deposits), or between those issued with a fixed or variable rate of interest.

Every financial instrument also provides the purchaser with a return or yield. The yield on any financial instrument is related to its characteristics and in general will be lower if the instrument is liquid, has a short time to maturity and has a lower level of risk. Thus, yields are usually higher for long-term investments because lenders require to be compensated for giving up their money for long periods of time and because the risk of default increases with time.

If financial instruments were perfect substitutes for one another, the yields on each would be identical. Any higher yield on one type of instrument would cause lenders to adjust their portfolios in favour of that instrument. The higher demand would then raise the market price of the instrument and thereby reduce the yield. Any variation in yields therefore represents a lack of perfect substitutability between different financial instruments. The various types of financial instruments traded in the UK are discussed in more detail when reviewing the functions of financial markets.

I The role of financial intermediaries

Financial intermediaries come between these wishing to save (lend) and those wishing to invest (borrow). They provide a service that yields them a profit, via the difference which exists between the (lower) interest they pay to those who lend and the (higher) interest they receive from those who borrow. That they can earn such profits reflects the fact that they are offering a useful service to both lenders and borrowers, which can be disaggregated into at least five separate functions:

1 brokerage

2 maturity transformation

3 liquidity transformation

4 risk transformation

5 collection and parcelling - size transformation.

Brokerage

The brokerage function is rather different from the other four, which might all be regarded as including elements of ‘asset transformation’. A broker is an intermediary who brings together lenders and borrowers who have complementary needs and does this by assessing and evaluating information. The lender may have neither the time nor the ability to undertake costly search activities in order to assess whether a potential borrower is trustworthy, is likely to use the funds for a project that is credible and profitable, and is able to pay the promised interest on the due date. By depositing funds with a financial intermediary the household avoids such information gathering, monitoring and evaluation costs, which are now undertaken by the specialized financial intermediary.

The borrower needs to know that a promised loan will be received at the time and under the conditions specified in any agreement.By bringing lenders and borrowers together in these ways, the various information and transactions costs are reduced, so that this brokerage function can command a ‘fee’. The size of that fee will, of course, be greater the more difficult and expensive it is for the financial intermediary to develop procedures for evaluating and monitoring borrowers in order to minimize ‘default risks’.

The next four functions involve elements of asset transformation, in which the liabilities (deposits) are transformed by the financial intermediaries into various types of asset with differing characteristics in terms of maturity, liquidity and risk.

Maturity transformation

Here the financial intermediaries bridge the gap between the desire of lenders to be able to get their money back quickly if needed, and the desire of borrowers to borrow for a long period. In fulfilling this function, the financial intermediaries hold liabilities (e.g. deposits) that have a shorter term to maturity than their assets (e.g. loans), i.e. they borrow short and lend long. For example, a building society will typically hold around 70% of its liabilities in the form of deposits repayable ‘on demand’, i.e. which can be withdrawn at any time without penalty. In contrast, around 75% of its assets are repayable only after five years or more.

Financial intermediaries are able to perform this maturity transformation function in part because of the ‘law of large numbers’, which implies that while some depositors will be withdrawing funds others will be making new deposits. This means that, overall, withdrawals minus new deposits are likely to be small in relation to the value of total deposits (liabilities). As a result the ‘funding risk’, namely that depositors might wish to withdraw more funds than the banks have available in liquid form, is greatly reduced. This enables the financial intermediaries to hold a sizeable proportion of less liquid assets (e.g.

long-term loans) in their portfolio.Liquidity transformation

Related to the ability to transform maturity, banks also undertake liquidity transformation. Liquidity is the ability of a debt holder, e.g. the deposit holder in a bank, to redeem their deposit quickly and without cost in the event that they desire or need cash. Banks issue claims in the form of deposits which do not require their holders to give the bank any notice or pay any penalties for premature withdrawal. In contrast banks hold assets that are largely illiquid and costly to convert back into cash. This ability to hold liabilities that are liquid but assets that are illiquid is a key feature of banks and is known as liquidity transformation. Banks can achieve this for much the same reasons as for maturity transformation - as the number of customers that a bank can attract increases, the ability to measure the amount of daily liquidity required for the bank becomes more predictable, such that a bank will be able to calculate, with some certainty, the value of cash that will be needed on any one day and hold enough cash reserves to meet this demand. The rest of their assets can then be held in more illiquid, higher yielding assets. Once again this can be related to the law of large numbers outlined above.

Risk transformation

This involves the financial intermediaries in shifting the burden of risk from the lender to themselves. Their ability to do so depends largely on economies of scale in risk management. The large amounts of deposits (liabilities) the financial intermediaries collect allow them to diversify their assets across a wide variety of types and sectors. ‘Pooling’ risk and reward in this way means that no individual is exposed to a situation in which the default of one or more borrowers is likely to have a significant effect.

Collection and parcelling

Financial intermediaries also transform the nature of their assets through the collection of a large number of small amounts of funds from depositors and their parcelling into larger amounts required by borrowers. Often the financial intermediaries have relied on obtaining many small deposits from conveniently located branches of their operations. This process is known as ‘size intermediation’ and benefits borrowers because they obtain one large loan from one source, thus reducing transaction costs. Of course this loan is an asset to the financial intermediary and a liability to the borrower.

The common characteristics of all financial intermediaries are therefore as follows. First, they take money from those who seek to save, whether it be in exchange for a deposit account bearing interest or in exchange for a paper financial claim. Second, they lend the money provided by those savers to borrowers, who may issue a paper asset in return. Third, in exchange for such lending they acquire a portfolio of paper assets (claims on borrowers) which will pay an income to the intermediary, and which it may ‘manage’ by buying and selling the assets on financial markets in order to yield further profits for itself.

I UK financial intermediaries

The UK financial system incorporates different types of financial intermediary, offering lenders and borrowers a variety of instruments which have different maturities, liquidities and risk profiles. A popular method of classification is to distinguish between the bank and non-bank financial intermediaries.

■ Bank sector. All the UK financial institutions that have been issued with a banking licence, including the high street commercial banks, the corporate wholesale banks and the foreign banks, all of which are regarded as being part of the bank sector. Currently there are 346 authorized banking institutions operating in the UK, a fall of over 200 from the 1990 figure of 548.

■ Non-bank sector. The other financial intermediaries, including the building societies, insurance companies, pension funds, unit trust and investment trust companies, are classified as part of the non-bank sector. A further disaggregation of the non-bank sector brings together those institutions which are deposit-taking institutions, such as the building societies, and those which are investing institutions, namely all the non-bank sector except the building societies.

However, even this simple classification of bank and non-bank sector is becoming more difficult to sustain with the growth of competition since the 1990s between these sectors (inter-sector competition) and between the institutions within these sectors (intrasector competition), so that the distinction between banking and non-banking institutions has become increasingly blurred. Nevertheless, it may be helpful to consider the UK financial intermediaries under the following three headings: banking financial intermediaries, non-bank financial intermediaries and the Bank of England.

The UK banking financial intermediaries

The UK bank sector includes a range of financial intermediaries.

The retail banks

These include banks which either participate in the UK clearing system or have extensive branch networks. The retail banks are sometimes known as the MBBGs (Major British Banking Groups) which includes all the UK’s large retail banks. Listing these banks was once relatively simple, but a spate of mergers and acquisitions has meant changes in ownership. This has been further complicated by the 2007/08 global banking crisis which has led to further rationalization in the UK banking sector. As a result, the largest retail banking groups operating in the UK are Barclays plc; Lloyds Banking Group (which now includes Lloyds TSB and Halifax Bank of Scotland (HBOS)); Hong Kong and Shanghai Banking Corporation (HSBC) plc; The Royal Bank of Scotland (RBS) plc; the troubled mortgage bank, Northern Rock; and Santander UK which is based in Spain but now owns Abbey National, Alliance and Leicester and Bradford & Bingley’s savings business. Further complications have also resulted from the UK government having to step in to re-capitalize RBS, LloydsTSB and HBOS (who merged) and Northern Rock (see p. 455).

Traditionally, retail banks, through their extensive branch networks, have historically been primarily engaged in gathering deposits and creating loans, usually at high margins given that they could obtain deposits at low interest rates and could offer loans to individuals and firms at high interest rates. Activities in this sector were highly regulated until the early 1970s and were often described as being ‘supply led’, since most arrangements appeared to be in the interests of the providers rather than the customers.

Today, the retail banking market is increasingly competitive and banks are more responsive to the needs of their customers. The retail banks offer a wide array of services to personal customers, including savings accounts, unsecured and secured loans, mortgages, overdrafts, automated cash machines, home banking, foreign currency transactions and general financial advice. They also offer a range of services to corporate customers, including leasing and hire purchase, export and import facilities, payroll services and international financial transfers.

Total assets in the banking sector have increased substantially during the past 10 years, from around £3,145bn in 2000 to over £7,600bn by the end of 2009, despite the problems caused by the financial crisis; however, this figure is boosted by the trend of mutually owned building societies converting to banks (see below).

The wholesale banks

These include around 500 banks which typically engage only in large-scale lending and borrowing transactions, namely transactions in excess of £50,000. The wholesale banks include the following:

■ merchant banks, of which there are about 40 including the Accepting Houses;

■ other British banks, a general category covering banks with UK majority ownership;

■ overseas banks, which include American banks, Japanese banks and a variety of other overseas banks and consortium banks.

The wholesale banks actually include a large number of small providers. This, together with the fact that the majority of transactions are completed with knowledgeable corporate clients, usually results in margins being low. Nevertheless, individual transactions are ‘wholesale’, that is of a high value (greater than £50,000 but, more typically, in excess of £1m) so that sizeable absolute levels of profit can still be made. Wholesale banking takes place mainly in foreign currencies, which reflects the substantial presence of Japanese and American banks in this sector. Recent figures show that London remains the most popular financial centre with 249 foreign banks located there during 2009. However, the sector also includes the British merchant banks, whose major business includes the acceptance of bills, underwriting, consultancy, fund management and trading in the financial markets.

Historically, retail banks could be distinguished from wholesale banks by the nature of their business, in that they dealt in a high volume of small deposits, operated an extensive branch network, were actively involved in the cheque clearing system and relied heavily on the personal sector for their deposits (liabilities). However, these distinctions are becoming increasingly blurred due to the participation of all banks and other financial intermediaries in wholesale banking and to the growth of the inter-bank market.

Much of this convergence between the retail and wholesale banking sectors has been due to retail banks entering the wholesale arena, largely because of diminishing margins in the retail sector. We consider the response of the retail banks to a variety of challenges later in this chapter (p. 451). Wholesale banking, however, has remained relatively unchanged in that the vast majority of transactions remain with the corporate sector and are undertaken in foreign currencies.

UK non-bank financial intermediaries

The institutions in this sector fulfil a number of specialist functions, such as providing mortgage finance, insurance and pension cover. They typically specialize in matching the needs of borrowers for long-term finance with the needs of lenders for paper assets denominated in small units which are readily saleable. The UK non-bank financial intermediaries include the building societies, insurance companies, pension funds, unit trusts and investment trusts.

The building societies

These are mutually owned financial institutions which have traditionally offered loans in the form of mortgages to facilitate house purchase. Mutuality means that they are owned by their ‘members’, namely those who have purchased shares in the form of deposits, and those who have borrowed from them. Until the early 1980s, building societies were the only institutions offering mortgages, and competition was restricted by various agreements and regulations between the various building societies.

Competition in this sector has, however, intensified since the early 1980s when deregulation of the retail banking sector allowed banks to offer mortgage finance and thereby to threaten the position of the building societies. This led to demands for deregulation to be extended to the building society sector in order to allow the building societies to respond by competing with banks in financial and other markets, where previously they had been restricted. The Building Societies Act of 1986, the subsequent Orders in Council of 1988 and the Building Societies Act 1997 have permitted building societies to offer a whole range of new banking, investment and property- related housing services, in addition to their traditional savings and home loan business.

The Building Societies Act 1997 relaxed restrictions on unsecured lending and permitted building societies, subject to their own prudential controls, to lend out 25% of their assets on an unsecured basis. In addition, it allowed societies to have greater access to the wholesale money markets, permitting up to 50% of their funds (liabilities) to be in the form of borrowings on these markets. This meant that societies need not rely as heavily on costly retail deposits from savers to finance their lending, allowing them to compete more aggressively with the banking sector. In fact, by the end of 2007 total wholesale liabilities in the building society sector were over £66 billion.

However, the 1997 Act, while granting societies more freedom, also ensured that the building societies’ main function and basic purpose of attracting savings and making loans for house purchase remained. To this end, societies still have to raise at least 50% of their funds from individual investors (usually in the form of issuing a retail deposit) and remain restricted to having 75% of their commercial assets in the form of loans secured by a mortgage on housing.

The evidence indicates that building societies have remained true to their basic principles and remain predominantly mortgage finance providers. Table 21.1 shows that the building society sector provided over five times more mortgage lending by value in 2009 than consumer credit lending. However, the table shows that the building societies are seeing their share of the gross consumer credit market dwindle after an initial rise. The level in 2009 is only 1.9% of the total lending of consumer credit, reflecting both the effect of the financial crisis and the extent of demutualization. Rather more significantly, the share of the building societies in gross mortgage lending has declined substantially over the period to just under 13% of the market, whereas banks now dominate over 80% of the market. This reflects the trend in demutualization.

This trend is also reflected in Table 21.2 which shows that building societies are also losing their share of UK private-sector deposits. In 1985, some 45.1% of UK private-sector deposits were held in building society accounts and 49.5% in UK banks. However, by 2009 the building societies’ share had dropped to 12.1%, whilst the share of the banks had risen to over 80%. In fact such a trend had been long established; for example, the building societies witnessed a fall in their share of UK private sector deposits of over 32% between 1985 and 2000. Table 21.3 outlines the conversion of building societies into banks and their consequent changes in ownership.

Demutualization

As we have already noted, the building societies have been losing market share to the banks in the deposit, consumer credit and mortgage markets. Indeed, in 1997 the banking sector for the first time had a greater share of gross mortgage lending than the building societies, a trend which is set to continue. However, this comparison is not entirely fair, as it does not represent a like-for-like comparison over time. In fact, a major reason for these losses of market share involve the demutualization and conversion of the larger building societies into banks, which means that their business is now counted as part of the banking sector. Table 21.3 shows those building societies which have converted into banks, the date of conversion, the total assets and the market capitalization involved. A number of reasons have been suggested for this trend towards demutualization.

■ Banks are in a better position than building societies to compete in financial services and mortgage markets because they can issue shares. This will provide the funding to permit faster growth and enable speedier diversification into new areas.

Table 21.1 Bank and building society shares of gross Iendingfor mortgages and consumer credit, 2001-2009 (£m).

| 2001 | 2002 | 2003 | 2004 | 2005 | 2006 | 2007 | 2008 | 2009 | |

| Gross mortgage lending | |||||||||

| Building Societies | 26,086 | 34,862 | 46,347 | 46,563 | 43,505 | 52,391 | 51,847 | 37,760 | 18,531 |

| % of total | 16.4 | 15.9 | 16.7 | 16 | 15.1 | 15.2 | 14.3 | 14.7 | 12.9 |

| Banks | 119,031 | 161,852 | 194,853 | 201,866 | 201,765 | 234,592 | 246,925 | 193,982 | 118,533 |

| % of total | 74.6 | 73.6 | 70.3 | 69.6 | 70 | 67.9 | 68 | 75.7 | 82.5 |

| Other | 14,356 | 23,107 | 35,937 | 41,488 | 42,630 | 58,630 | 63,851 | 24,343 | 6,585 |

| % of total | 9 | 10.5 | 13 | 14.4 | 14.9 | 16.9 | 17.7 | 9.6 | 4.6 |

| Total | 159,473 | 219,821 | 277,137 | 289,917 | 287,900 | 345,613 | 362,623 | 256,085 | 143,649 |

| Gross lending of consumer credit | |||||||||

| Building Societies | 3,219 | 3,703 | 4,909 | 6,213 | 7,963 | 9,218 | 9,820 | 3,383 | 3,302 |

| % of total | 1.8 | 1.9 | 2.4 | 2.8 | 3.6 | bgcolor=white>4.44.8 | 1.8 | 1.9 | |

| Banks | 142,223 | 158,605 | 168,659 | 176,882 | 173,038 | 162,342 | 157,466 | 152,595 | 133,816 |

| % of total | 80.2 | 80.8 | 81.4 | 80.2 | 79.3 | 78.1 | 77.1 | 79.5 | 78.6 |

| Other | 31,792 | 33,868 | 33,513 | 37,491 | 37,222 | 36,433 | 36,993 | 35,973 | 33,165 |

| % of total | 18 | 17.3 | 16.2 | 17 | 17.1 | 17.5 | 18.1 | 18.7 | 19.5 |

| Total | 177,234 | 196,176 | 207,081 | 220,586 | 218,223 | 207,993 | 204,279 | 191,951 | 170,283 |

Source: Adapted from Bank of England (2010) Monetary and Financial Statistics 2010, Tables A5.3 and A5.6.

UK FINANCIAL INTERMEDIARIES 431

Table 21.2 UK private sector deposits with banks and building societies, 1985-2009 (£bn).

| 1985 | 1995 | 2000 | 2005 | 2006 | 2007 | 2008 | 2009 | |

| Total UK Banks | ||||||||

| UK private sector deposits | 114.9 | 412.6 | 696.7 | 1,047.50 | 1,193.50 | 1,333.50 | 1,522.90 | 1,675.00 |

| % of total | 49.5 | 60.6 | 79.8 | 79.9 | 80.7 | 80.8 | 80.4 | 83.0 |

| Building Societies | ||||||||

| UK private sector deposits | 104.8 | 211.3 | 112.9 | 189.8 | 206.9 | 231.6 | 275.6 | 244.3 |

| % of total | 45.1 | 31.0 | 12.9 | 14.5 | 14.0 | 14.0 | 14.5 | 12.1 |

| Other | ||||||||

| UK private sector deposits | 12.5 | 56.9 | 63.2 | 72.9 | 79.2 | 84.7 | 95.9 | 99.3 |

| % of total | 5.4 | 8.4 | 7.2 | 5.6 | 5.4 | 5.1 | 5.1 | 4.9 |

| Total | 232.20 | 680.80 | 872.80 | 1,310.20 | 1,479.60 | 1,649.80 | 1,894.40 | 2,018.60 |

Source: Adapted from British Bankers Association (2010) 27th Annual Abstract of Banking Statistics, Volume 23, Table 4.03.

Table 21.3 Building society conversions, total assets and market capitalization.

| Building society | Date of conversion | Total assets (£bn)* |

| Abbey (acquired by Santander UK) | July 1989 | 285 |

| Cheltenham & Gloucester (merged into Lloyds Banking Group) | August 1995 | 1,027 |

| National & Provincial (merged into Abbey - now Santander UK) | August 1996 | 285 |

| Alliance & Leicester (acquired by Santander UK) | April 1997 | 285 |

| Halifax (merged into Bank of Scotland to form HBOS - HBOS merged | June 1997 | 1,027 |

| into Lloyds Banking Group) | ||

| Bristol & West (merged into Bank of Ireland) | July 1997 | n/a |

| Woolwich (acquired by Barclays August 2000) | July 1997 | 1,379 |

| Northern Rock (UK government supported) | October 1997 | 87 |

| Birmingham Midshires (merged into Halifax - Halifax merged into | January 1999 | 1,027 |

| Bank of Scotland - HBOS merged into Lloyds Banking Group) | ||

| Bradford & Bingley (a portion merged into Santander UK) | December 2000 | 285 |

| *Total assets 2009 of the parent bank. | ||

| Sources: Building Society Association (2010a) BSA Annual Report, and earlier; Building Society Association (2010b) BSA | ||

| Yearbook2009/2010, and earlier. | ||

■ Building societies which convert to banks cannot be taken over for five years, giving them time to establish themselves and compete with the larger banks.

■ Building societies which convert can now compete under the same regulatory environment as banks, which means that they no longer have restrictions on access to the wholesale markets. This provides them with improved access to corporate clients and to cheaper funding, allowing them to compete more aggressively in the consumer credit market.

■ Diversification into new and risky areas of business should, it is argued, be undertaken by using newly issued capital raised by newly constituted institutions rather than by using historical capital derived from relatively safe savings and mortgage business.

Such arguments were present in the conversion documents of both the Alliance & Leicester Building Society and the Halifax Building Society. The Alliance & Leicester document (1996) stated that the society intends to expand its commercial lending activities, extend its use of wholesale money markets, and increase its provision of ‘personal financial services, such as unsecured lending, telephone banking, life assurance and unit trust products’. This will allow it to reduce its ‘dependency on the mature residential mortgage market... and to build new sources of revenue from cross-selling’.

Expansion and consolidation was also a central theme in the Halifax Building Society’s transfer documentation (1996). Their strategy statement read:

Halifax plc are seeking significant earnings growth in the areas of long term savings and protection products and personal lines insurance... Halifax must continue to focus on its key competitive advantages of providing innovative and competitive products together with a high level of customer service.

Those who doubt the benefits of conversion have, however, expressed their concern. First, the costs of paying large dividends to shareholders will increase the interest rate to borrowers and decrease the rate for deposit holders (lenders). Second, capital markets have a tendency to be short term in their evaluation of strategy and performance, which may hinder longterm growth. Third, there is little evidence that banks are more accountable to their owners than are building societies. Fourth, takeover threats by other banks may still exist. At least one building society waived its right not to be taken over after conversion and in any case the protection from takeover for five years is removed if another building society initiates the takeover, as when Birmingham Midshires was acquired by the Halifax in 1999. Fifth, there are increased costs resulting from conversion, including the cost of compliance with a new regulatory code and the cost of retraining staff.

However, the comparison of building societies with banks and the debate as to the respective advantages and disadvantages of conversion have arguably become redundant issues, having been overtaken by events. Those building societies that wish to remain specialist mortgage providers are likely to stay in the building societies sector and, by remaining as mutual institutions, may acquire a competitive edge in offering mortgages at lower interest rates. Much of the rationalization of this sector may already have occurred, there having been 481 building societies in 1970 but only 63 by the end of 2005. However, it is worth noting that these societies continue to manage over £270bn worth of assets.

On the other hand, most former building societies that have wished to expand their range of products and services, having found regulations in the sector somewhat restrictive, have already chosen to convert. Of the top 10 building societies in December 1996, only three exist today, namely Nationwide, Britannia and Yorkshire.

Insurance companies and pension funds

About half of all personal savings are channelled into these institutions via regular and single-premium life assurance and pension payments. These savings from the personal sector are used to acquire a portfolio of assets. The institutions then manage these assets with the objective that they yield a sufficient return to pay the eventual insurance and pension claims as well as providing a working rate of return for the financial institutions themselves. The insurance companies and pension funds are major investors in the financial markets and exert considerable influence in these markets. They hold large amounts of longterm debt and help absorb (‘make markets in’) large volumes and values of new issues of various equities, bills and bonds.

Although these insurance companies and pension funds compete strongly against each other in the personal savings market, their portfolio choices differ because the structures of their liabilities differ. For example, the life assurance companies hold a larger proportion of assets as fixed-interest securities, because many of their liabilities are expressed in nominal terms (e.g. money value of payments in the future on policies is known). Pension funds, however, hold a larger proportion of assets in the form of equities, which historically have yielded higher real rates of return, because many of their liabilities are expressed in real terms (e.g. pensions paid in the future are often index linked). However, both these institutions are affected by the volatility of financial markets, both domestic and worldwide. For example, at the beginning of 2000 they held quoted UK company shares to the value of £743bn, which made up 45% of their total financial assets of £1,657bn. As the UK share market dropped, the value of their investments in UK company shares halved and by the end of 2002 it was worth only £388bn. As a result, total financial assets held by insurance companies and pension funds also fell to 1998 levels of around £1,250bn. The financial crisis has meant that the value of these holdings had dropped to £353bn by 2009. Importantly, such volatility can affect both premiums and payouts in the sector.

Unit and investment trusts

Both unit and investment trusts offer lenders a chance to buy into a diversified portfolio of assets and thereby reduce risk while at the same time receiving attractive returns. These institutions can achieve this by pooling the funds received from a large number of small investors and then implementing various portfolio management techniques not available to such small investors.

There are over 1,400 unit trusts, provided by individual companies, banks and insurance companies. A lender looking to buy into a unit trust purchases the number of units they can afford at the current value and then pays a further 5% of the purchase price for the management of the fund. The price of each unit is given by the net value of the trust’s assets divided by the number of units outstanding. The size of the unit trust fund varies with the amount of units currently in issue, which allows the fund to expand and contract depending on demand, thus unit trusts are termed ‘open ended’.

There are over 300 investment trusts and they undertake a similar role, allowing individuals to benefit from a pooled investment fund. However, investment trusts are plcs and raise funds for investment by issuing equity and debt and by using retained profits. Unlike unit trusts they can also borrow money. If individuals or firms are to buy into an investment trust, they must purchase their shares, which are limited in supply, thus investment trusts are termed ‘closed ended’.

Table 21.4 shows total investments by both unit and investment trusts. Two factors are worth noting. First, unit trusts hold over ten times the value of assets held by the investment trusts. Second, both institutions invest heavily in foreign company shares, with unit trusts investing around 37% and investment trusts about 49% in this type of investment.

An important issue is the extent to which insurance, pension fund, investment and unit trust companies are involved in equity finance. These institutions are responsible for holding around 50% of UK equity, which means that share prices will be significantly affected by the portfolio preferences of these institutions. That preference will be influenced by overall

Table 21.4 Total investments of investment and unit trusts, 2008 (market value, £m).

| Unit trusts holdings | Investment trusts holdings | |

| Investment: | ||

| British Government Securities | 33,469 | 628 |

| UK listed company securities | 190,985 | 14,204 |

| Overseas company securities | 144,108 | 19,008 |

| Other | 19,637 | 5,239 |

| Total | 388,199 | 39,079 |

| Source: Adapted from ONS (2010) Financial Statistics | ||

| 2010, Tables 5.2C and 5.2D. | ||

‘environmental’ factors, such as the inflation rate, the exchange rate and the state of business expectations, as well as by the particular needs of the institutions themselves. A concern is that such institutions may tend to be affected in the same way by the same set of factors, so that share prices may be more volatile than would otherwise be the case. This could have significant repercussions on the individual companies concerned because share prices may then fluctuate in ways which do not reflect their true valuation in terms of yield. It follows from this that the ability of companies to raise funds on the Stock Exchange may be affected by the activities of these institutions, and possibly in ways unconnected to their underlying profit potential.

I The Bank of England

The Bank of England is at the head of the UK financial system, is owned by the government (having been nationalized in 1946), and has a monopoly on the note issue in England and Wales. As the central bank of the UK, the Bank is committed to maintaining a stable and efficient monetary and financial framework. In pursuing its goal, it has three core purposes (Bank of England 2000, p. 14).

1 Maintaining the integrity and value of the currency. Above all, this involves maintaining price stability (as defined by the inflation target set by the government) as a precondition for achieving the wider economic goals of sustainable growth and high employment. The Bank pursues this core purpose through its decisions on interest rates taken at the monthly meetings of the MPC, by participating in international discussions to promote the health of the world economy, by implementing monetary policy through its market operations and its dealings with the financial system, and by maintaining confidence in the note issue.

2 Maintaining the stability of the financial system, both domestic and international. The Bank seeks to achieve this through monitoring developments in the financial system both at home and abroad, including links between the individual institutions and the various financial markets; through analysing the health of the domestic and international economy; through close co-operation with the financial supervisors, both domestically and internationally; and through developing a sound financial infrastructure including efficient payment and settlement arrangements. In exceptional circumstances (in consultation with the Financial Services Authority and HM Treasury as appropriate) the Bank may also provide, or assist in arranging, lastresort financial support where this is needed to avoid systemic damage.

3 Seeking to ensure the effectiveness of the UK’s financial services. The Bank wants a financial system that offers opportunities for firms of all sizes to have access to capital on terms that give adequate protection to investors, and which enhances the international competitive position of the City of London and other UK financial centres. It aims to achieve these goals through its expertise in the marketplace, by acting as a catalyst to collective action where market forces alone are deficient, by supporting the development of a financial infrastructure that furthers these goals, by advising government, and by encouraging British interest through its contacts with financial authorities overseas.

In order for it to achieve its core purposes, the Bank is split into three main divisions, each of which has its own responsibilities to the UK financial system. These are the Monetary Analysis and Statistics division, the Financial Market Operations division and the Financial Stability division.

Monetary Analysis and Statistics division

This division is responsible for providing the Bank with economic analysis that helps the MPC (see p. 437) formulate its monetary policy to aid economic growth and control inflation. Within this division, economists at the Bank conduct research and analyse developments in international and UK economies and publish reports which are then made publicly available. These include the Bank of England Quarterly Bulletin, the Inflation Report and the monthly Monetary and Financial Statistics.

Financial Market Operations division

This division has three main areas of responsibility.

1 Operations in the financial markets. It is responsible for planning and conducting the Bank’s operations in the core financial markets, especially the sterling wholesale money markets, where it aims to establish short-term interest rates at the level required by government in order to meet its monetary policy objectives (see p. 436). This division also manages the UK’s foreign exchange and gold reserves and contributes market analysis to aid the MPC and the Financial Stability Committee in their operations.

2 Banking and market services. It undertakes the traditional role of providing banking services to the government, banks and other central banks and managing the note issue. In addition, the division also plays an important role in providing (and monitoring) a safe and efficient payment and settlement system for the UK financial markets and the wider economy.

3 Risk analysis and monitoring. It is responsible for analysing any risks that may arise from the Bank’s operations in the financial markets and for assessing the effects that these may have on the Bank and the UK economy.

Financial Stability division

The Bank of England no longer has any supervisory or regulatory powers over the UK financial system, so the Financial Stability division undertakes to maintain the stability of the financial system as a whole. Its main areas of responsibility are domestic finance, financial intermediaries, international finance, financial market infrastructure and regulatory policy. This division works closely with the Financial Stability Committee which is chaired by the Governor of the Bank of England. In general, the work of the division covers the functioning of the international financial system as well as that of the UK. To this end, it carries out research into developments in the structure of financial markets and institutions and makes proposals for changes to increase safety and effectiveness. The division is also responsible for publishing the Financial Stability Review.

In operational day-to-day terms the Bank of England has an important influence on three major markets: the sterling money market, the foreign exchange market and the gilt-edged market.

1 The Bank is a major player in the sterling money market (see p. 440), buying and selling Treasury bills on a daily basis. The object is twofold. First, the Bank buys or sells bills in order to ease cash shortages or to withdraw cash surpluses, which arise as a result of daily transactions between the government and the public. Such transactions by the Bank affect commercial bank clearing balances, alter the liquidity of these banks and hence their willingness to lend. Second, the ‘Financial Market Operations’ division of the Bank trades in bills with the government’s interest rate policy specifically in mind. The buying and selling of bills by the Bank affects yields and therefore influences interest rates throughout the market (see p. 443). The Bank, in its daily dealings, attempts to reconcile these two separate objectives.

2 The Bank has a major role in the foreign exchange market as it is responsible for carrying out government policy with regard to the exchange rate. A strong pound has been seen by successive governments as essential if inflation is to be kept low. The combination in recent years of a floating pound and a weak balance of payments on current account has made it necessary to attract short-term funds on capital account by maintaining high interest rates. The Bank also uses the Exchange Equalization Account to intervene in the foreign exchange market by buying up surplus sterling should it need to support the external value of the pound.

3 The Bank is also influential in the gilt-edged market as it administers the issue of new bonds when the government wishes to borrow money. Various methods are used, depending on market circumstances. The ‘tap’ method is where bonds (gilts) are issued gradually in order not to flood the market and depress the price; the ‘tender’ method is where institutions are invited to tender for a given issue; and the ‘auction’ method is where bonds are sold to the highest bidders among the 20 or so gilt-edged market makers (GEMMAs). The Bank also manages the redemption of existing bonds in such a way as to smooth the demands on the government’s financial resources. For instance, it buys up bonds which are nearing their redemption date, so as not to have to make large repayments over a short period of time.

The Bank faces a continual problem in that its actions in each of these markets have repercussions for the functioning of the other markets. For instance, intervention to purchase sterling in the foreign exchange market in order to support the sterling exchange rate is often ineffective because of the size of speculative outflows of short-term capital from the sterling money and gilt-edged markets. As a result, interest rates may need to be raised in order to deter these short-term capital outflows. This often proves difficult, however, because of the way in which daily transactions between the government and the public affect the balances of the clearing banks with the Bank of England. For example, if the banks are short of liquidity the Bank of England may be purchasing bills on the Open Market in order to help replenish their cash balances. However, purchasing existing bills by the Bank of England will raise their market price and lower their yield, i.e. lower interest rates. This may then conflict with the need to keep interest rates high to prevent shortterm capital outflows from depressing the sterling exchange rate.

Bank of England and the economy

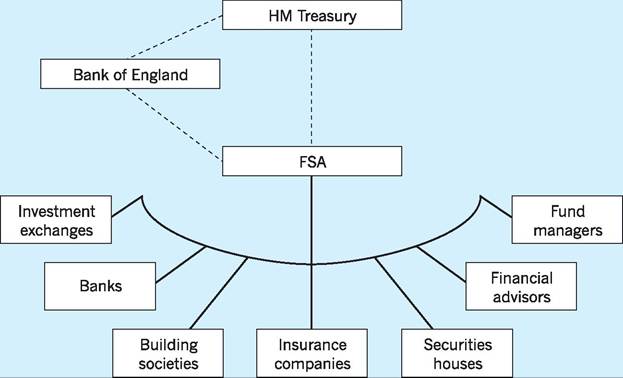

The three main purposes of the Bank of England were defined in May 1997, when the then Chancellor of the Exchequer, Gordon Brown, proposed a number of institutional and operational changes to the Bank of England. First, it was given operational independence in setting interest rates which would now be the responsibility of a newly created Monetary Policy Committee (MPC) working within the Bank. Second, the regulation of the banking sector was taken away from the Bank and given to a newly established ‘super’ regulator called the Financial Services Authority (FSA). Third, although the government retained responsibility for determining the exchange rate regime, the Bank could now intervene at its discretion in support of the objectives of the MPC. Fourth, the management of the national debt was transferred from the Bank to the Treasury. These changes were set out in The Bank of England Act which came into force on 1 June 1998. The most important of these changes involved the creation of the MPC and the FSA.

The Monetary Policy Committee (MPC)

The Bank of England Act established that the responsibility for monetary policy and therefore for setting short-term interest rates was to reside with the MPC, a committee within the Bank of England. The MPC would be free from government intervention in all but extreme economic circumstances. The aim of shortterm interest rate setting would be to restrict the growth of inflation to within a target range set by the government and announced in the annual Budget Statement. The target had been set at 2.5% for annual retail price inflation, excluding mortgage interest payments (RPIX), but was subsequently revised in 2003 to a point target of 2% for CPI inflation. Significantly, if inflation is more than 1% either side of this figure then the MPC is required to write an open letter of explanation to the Chancellor.

The MPC consists of the Governor of the Bank, two Deputy Governors, two members appointed by the Bank in consultation with the Chancellor, and four ‘experts’ appointed by the Chancellor. The MPC meets monthly, publishes its decisions within days of concluding any meeting and publishes minutes of the meeting within six weeks.

There has been much discussion as to the merits of these changes. In essence, they are an attempt by the Chancellor of the Exchequer to take the ‘politics’ out of setting interest rate policy. Hall (1997) makes the following points:

As a device for enhancing the credibility of monetary policy the current regime, if allowed to work with optimal efficiency, is vastly superior to its predecessors, which had confirmed the worst fears of outside observers by allowing the Chancellor to attempt to extract the maximum political advantage from the interest rate setting process... Moreover, if one believes in a high and positive correlation between the degree of independence enjoyed by a Central Bank and that country’s success in fighting inflation, then the recent changes can only but serve to reinforce one’s optimism about the UK’s future inflation prospects.

It has been argued that as a result of such independence, the financial markets will gain additional confidence in the UK’s ability to control future inflation. Some have pointed to the fact that long-term interest rates for UK government borrowing have reached a 30-year low since the Bank’s independence was announced, as evidence of such confidence. Nevertheless, concerns over the new policy include fears that the Bank may set interest rates which are higher than necessary to control inflation, thereby stifling investment and raising the sterling exchange rate to levels which damage trading sectors of the economy, such as manufacturing. Others have argued that the MPC should have been given a target for economic growth as well as a target for inflation, to prevent an overemphasis on deflationary policies.

The Financial Services Authority (FSA)

Overall, supervision of any banking system is essential to protect the interests of depositors, and although there was some degree of depositor protection in the 1960s it was not until the secondary banking crisis of the 1970s that formal supervisory structures were developed and embodied in the Banking Acts of 1979 and 1987.

Traditionally, the Board of Banking Supervision within the Bank concerned itself with three issues.

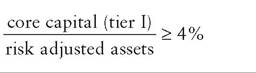

1 Capital adequacy. To what extent do banks have sufficient reserves of capital to cover the possibility of default by borrowers? This issue has become particularly important in recent years as the volume of Third World debt has grown to unmanageable proportions. The 1989 Solvency Ratio Directive established an EU-wide rule that a bank’s capital reserves must be at least 8% of its risk- adjusted assets and off-balance-sheet transactions. Off-balance-sheet transactions include such things as an advance commitment to lend (rather than an actual loan) which may or may not ultimately lead to a future balance sheet entry.

2 Liquidity. There is currently no formal requirement as to adequate liquidity holdings by banks. However, the Bank of England required all banks under the Banking Act of 1987 to keep a ratio of ‘primary liquid assets’ to some definition of deposit liabilities. Such ratios may differ as between different types of banks, and deposits will be ranked according to their maturity. The shorter is the maturity structure of deposits, the higher will be the ratio of liquid assets required.

3 Foreign currency exposure. This issue relates particularly to banks which take deposits and lend in different currencies. Supervisors are concerned that banks should balance their assets and liabilities in each currency in such a way that their ‘exposure’ (to risk of loss on the foreign exchange market) should not exceed 10% of their capital base.

However, in May 1997 the Chancellor also reformed the regulatory structure of the financial system. As already noted, regulation and supervision of the banking sector was traditionally the responsibility of the Bank of England. In contrast, the regulation and supervision of the non-bank sector has historically been the responsibility of numerous different bodies, such as the Building Societies Commission and the Securities and Investment Board which itself headed three other self-regulating bodies. The Chancellor of the Exchequer highlighted problems with the then regulatory structure in a statement on 20 May 1997:

It has long been apparent that the regulatory structure introduced by the Financial Services Act 1986 is not delivering the standard of supervision and investor protection that the industry and the public have a right to expect. The current two tier system splits responsibilities... This division is inefficient, confusing for investors and lacks accountability and a clear allocation of responsibilities. It is clear that the distinctions between different types of financial institutions - banks, securities firms and insurance companies - are becoming increasingly blurred... [therefore] there is a strong case in principle for bringing the regulation of banking, securities and insurance together under one roof.

The Bank of England Act of 1998 transferred the regulatory functions of the Bank to a new regulatory authority called the Financial Services Authority (FSA), which was now to be responsible for regulating all financial institutions, whether bank or non-bank. The Bank of England retains responsibility for monitoring the financial system, with the government establishing a structure whereby the Treasury, the Bank of England and the FSA work together to achieve stability. In a Memorandum of Understanding published in October 1997 the Chancellor set out the various roles of the Treasury, the Bank and the FSA, making it clear that these organizations should exchange information and consult regularly. A standing committee was established to provide the means for the three bodies to discuss any foreseeable problems.

The new regulatory structure was completed by the establishment of a new Financial Stability Committee whose functions were to oversee the stability of the system and detect any risk of system-wide failure. This Committee had the responsibility of liaising with the Standing Committee created by the Memorandum of Understanding. Figure 21.2 provides an overview of the new regulatory structure.

I UK financial markets

The financial markets within the UK perform a variety of functions which make them attractive to both lenders and borrowers. Such functions include providing a place to trade financial instruments and a system by which to ‘price’ such instruments. The major UK financial markets are located in London, one of the three dominant financial centres together with New York and Tokyo. One reason for London’s dominant position is the large number of overseas banks transacting in foreign currencies on the financial markets.

As with the financial intermediaries, there are a number of ways in which the financial markets might be classified. One of the most common is to separate the UK financial markets into the sterling wholesale money markets and capital markets.

Fig. 21.2 The regulatory structure in the UK.

The sterling wholesale money markets

Transactions undertaken in the UK ‘money market’ involve the borrowing and lending of short-term wholesale funds by financial institutions. ‘Short-term’ means for periods varying from one day to one year, and ‘wholesale funds’ means amounts in excess of £50,000. Money market activity in London has developed rapidly over the last 35 years, partly due to the growth of the financial sector in general, but also because of the increasing demand for sophisticated financial services by clients both in the UK and abroad.

In the UK, the money markets have been traditionally split into the primary markets, which issue new financial instruments, and the secondary (or parallel) markets, which deal in previously issued financial instruments or securities (financial instruments which can be traded by third parties are known as securities). This distinction is no longer relevant today and it is best to think of the wholesale money market as one market issuing and trading short-term financial instruments. There are various money markets operating in the UK but it is useful to begin with the discount market.

The discount market

The discount market has always played an important role within the UK financial system. In this market, short-term (commonly 91 days) financial instruments known as ‘bills’ are bought and sold ‘at a discount’ to their redemption value on maturity (i.e. bought and sold at a price below their maturity value). The discount market has no physical location and only bills of the highest quality are traded. This is ensured by bills being accepted and underwritten (guaranteed) by creditable banking institutions (counterparties), with the Bank of England dealing only with ‘eligible’ bills that have been accepted by these registered counterparties.

During the nineteenth century, the major function of the discount market was the discounting of commercial bills of exchange which financed the increasing volume of international trade. In general, the functions of the discount market today are to allow commercial banks to adjust their cash positions, to provide short-term finance to the government and corporate sector, and to underwrite and ‘make-a-market’ in the weekly trade of government Treasury bills.

Traditionally, the main players in the discount market were the discount houses that bought and sold discounted bills, thereby acting as a buffer between the Bank of England and the UK banking sector. This meant that if the banking sector needed more cash (liquidity), the Bank of England would provide this by purchasing bills from the discount houses. The discount houses would then make the cash from the sale of the bills available to the banking sector. However, over the past few years the Bank of England has started to provide direct support to the banking sector. The UK banks have also made growing use of the inter-bank market and other money markets to adjust their liquidity, which has somewhat nullified the role of the discount houses. Today, many of the former discount houses have merged with larger financial institutions, so that the Bank of England now deals only with registered counterparties, which include banks, building societies and securities firms. The Discount House Association, which was the overseer of the operations of the (now defunct) eight discount houses, has been replaced by the Finance House and Leasing Association.

The main functions of the counterparties are to:

■ underwrite the weekly tender issue of Treasury bills by bidding competitively for those bills not sold;

■ provide short-term finance for companies by discounting bills; and

■ maintain a secondary market in certificates of deposit (CDs) and other short-term financial instruments.

The characteristics of bills

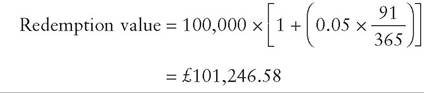

Bills are short-term financial instruments that are generally issued by large corporations (known as commercial bills) or by the Bank of England on behalf of the government (known as Treasury bills or Tbills) and traded on the discount market. The original purchaser (the lender) buys the bill at below its face or redemption value, i.e. at a discount, and earns a return by holding it until maturity. Alternatively, the original purchaser can sell the bill in the discount market before the bill matures. For example, the government might make an issue of £100,000, 91-day bills, at a discount of £2,000. This would mean that the purchaser would pay £98,000 for the bills and on maturity, in 91 days, would receive £100,000 back from the government. For the purchaser of the bill, it is important that they are aware of the annual percentage ‘yield’ or ‘return’ on the bill so that they can compare it with other financial instruments. The annualized ‘discount yield’ is calculated using the formula:

In the above example the discount is £2,000, the redemption value of the bill is £100,000 and n equals the number of days to maturity, which is 91. Therefore the annual ‘discount yield’ on the above bill is given by

The discount yield, however, is not the actual return that the investor enjoys, because in the above formula the redemption value of the bill has been used and not the purchase price of the bill. To convert the discount yield into the rate of interest enjoyed by the purchaser of the bill and one that is comparable with other financial instruments, it is necessary to change the denominator in the formula, thus:

which is slightly higher than the discount yield. Bills have a number of additional features.

■ They are issued in denominations of no less than £5,000 (but more typically £250,000).

■ They are highly liquid and low-risk securities. They gain their liquidity from being short-term and from being actively traded on the discount market. They are low-risk instruments because either they are issued by governments or, in the case of commercial bills, they have been underwritten by creditable banks - giving them eligible bill status, meaning that they are eligible for discount at the Bank of England.

■ They are fixed income securities because the purchaser of the security knows the amount they will receive from the bill at the time of purchase. However, their price fluctuates in line with any change in market or current interest rates.

The sterling inter-bank market

This market is now the largest and the most significant of the money markets. The inter-bank market allows financial institutions to borrow and lend wholesale funds amongst themselves (dealing through money brokers) for periods ranging from overnight to five years. By using such borrowings, banks have been able to make (profitable) lending decisions which are to some extent independent of the amount of personal deposits that they have been able to attract, because they could now obtain any extra funding they might acquire on the inter-bank market. The amounts involved are large, starting from £500,000, but £10-12m is not untypical. Banks today borrow to finance lending, to balance out fluctuations in their books, and to speculate on future movements in interest rates. The London Inter-Bank Offer Rate (LIBOR) therefore represents the marginal or opportunity cost of funds to the banks and is the major influence on banks’ base rates. The average size of the market in 2009 was over £237bn.

The sterling certificate of deposit market Certificates of deposit (CDs) are paper assets issued by banks, building societies and finance houses to depositors who are willing to leave their money on deposit for a specified period of time. They are issued for periods ranging from three months to five years, but tend to be shorter rather than longer term and are issued at a rate of interest which can either be fixed or floating. Unlike Tbills and commercial bills, CDs are issued ‘at par’ (that is, its issue, nominal or face value) and the interest is added on to the face value at maturity, when the deposit is repaid. So, for example, the future (or redemption) value of a 91-day £100,000 CD that pays 5% interest can be found by the formula:

The purchaser of the CD can sell it on the market at any time if they have a requirement for liquidity. This enables banks to lend for longer time periods because they can be certain of having access to liquidity. In addition, CDs are attractive to portfolio holders because the yield is competitive. By 2009, UK banks held £132bn in CDs and other shortterm paper liabilities on their balance sheet.

The sterling commercial paper market

Since May 1986, companies have been permitted to issue short-term (7-364 days) unsecured promissory notes, which can then be traded at a discount. This provides a way of raising cheap short-term funds for businesses that require finance for general business purposes. The 1989 Budget extended the right to issue this form of sterling commercial paper to governments, overseas companies and certain overseas authorities, as well as to banks, building societies and insurance companies.

Large companies, or companies with high credit ratings, can borrow funds at more competitive rates than they can obtain from the banks. The creation and growth of this market has led to disintermediation, whereby companies circumvent the various financial institutions and deal directly with the wholesale markets themselves. This could be a concern for banks in that they may be left with borrowers who are of ‘lower quality’ and therefore riskier should a larger proportion of the ‘higher quality’ companies deal directly with the wholesale markets.

Euromarkets

Eurocurrency is currency held on deposit with a bank outside the country from which that currency originates. For example, loans made in dollars by banks in the UK are known as eurodollar loans. The eurocurrency market is a wholesale market and has its origins in the growing holdings of US dollars outside the US in the 1960s. Since that time, eurocurrency markets have grown rapidly to include dealing in all the major currencies, and have become particularly important when oil price rises create huge world surpluses and deficits, resulting in large shifts in demand for and supply of the major world currencies.

The major participants are banks, who use the euromarkets for a variety of reasons: for short-term inter-bank lending and borrowing, to match the currency composition of assets and liabilities and for global liquidity transformation between branches. However, the market is also extensively used by companies, and by governmental and international organizations. Lending which is longer-term is usually done on a variable-rate basis, where the interest is calculated periodically in line with changing market rates.

There are two important factors which make eurocurrency business attractive. The first is that the market is unregulated, so that banks which are subject to reserve requirements or interest rate restrictions in the home country, for instance, can do business more freely abroad. The other factor is that the margin between lending and borrowing rates is narrower on this market than on the home market, primarily because banks can operate at lower cost when all business is wholesale and when they are not subject to reserve requirements.

UK capital markets

In contrast to the short-term transactions undertaken in the UK wholesale money markets, the capital market provides an arena in which private and public sector companies can trade medium- and long-term financial claims. These financial claims can be either equity shares, interest-bearing debt instruments (bonds) or a mixture of the two types of instrument.

Purchasers of equity have bought themselves a legal share in the ownership of the company, giving them the right to contribute in the determination of broad company strategy as well as a claim on the profits of the company. Purchasers of debt, in the form of bonds, in contrast, have purchased a longterm financial instrument which provides them with a flow of cash interest payments at specific times in the future. The purchasers of debt are classed as creditors or lenders and do not have ownership rights on the company.

The characteristics of equities

Equities (or shares) are non-redeemable financial instruments issued by companies. Any profits that are paid to shareholders are done so in the form of a dividend, which is usually paid annually. Shareholders usually have voting rights in the election of directors and have a claim on any income left over if the company is liquidated. However, the major advantage of holding this kind of instrument lies in the possibility of capital appreciation if strong profit growth is anticipated some time in the future. In the case of preference shares the company pays a fixed annual sum to the shareholder and there is also the possibility of capital appreciation when the share is sold. Ordinary shareholders bear the largest risks since if the company goes out of business, the ‘preferred’ shareholders have first claim to a share of the money raised by selling assets (although only after the Inland Revenue, Customs and Excise and secured bank borrowers are paid). However, in good times, the ordinary shareholder will earn the greatest returns as dividend payments may be much greater than the fixed return received by the preference shareholders. As always in the financial markets, those who bear most risk have higher potential for returns.

The characteristics of bonds

Bonds are interest-bearing financial instruments issued by central and local governments, companies, banks and other financial institutions. The issuer of the bond (the borrower) undertakes to redeem the bond at ‘par value’ (£100) on a certain date and to pay the bondholder an annual fixed sum (the coupon rate) in interest each year. They are usually issued to mature in between five and 25 years’ time with the year of maturity included in the bond’s title, though some government bonds are undated and will never be redeemed. Bonds are also classified by their residual maturity, meaning the amount of time left until the bill will be redeemed by the issuer. Bonds with up to five years until maturity are known as ‘shorts’, those with between five and 15 years to maturity ‘mediums’, with those with over 15 years to run being known as ‘longs’.

Bonds may be bought either as a new issue or second-hand on the secondary markets. The lender buying from the secondary market may have bought the bond at a price below par value and this makes the annual fixed interest payment more attractive, taking into account this lower price. For example, if 5% government bonds (gilts) of par value £100 are bought on the secondary market at £50, the buyer receives £5 a year from the government (that is, 5% of £100). However, the actual yield for the lender in this case is 10% (£5 from £50). In addition, the lender will gain a further £50 if they hold the bond until it matures when the government will redeem it for £100. Bonds normally bear a fixed rate of interest and this means that there will usually be an inverse relationship between the market price of an existing bond and movements in current interest rates. Therefore, in the above example, a doubling of the current interest rate from 10% to 20% would mean that the Treasury bond would halve in value (ignoring any later capital gain on maturity) to £25 because £5 return on £25 corresponds to an annual yield of 20% (£5/£25 ? 100 = 20%). This would certainly be the market price for an existing Treasury bond with no future redemption date (known as consols) and therefore no future capital gain. If the price of such bonds did not fall by £25 when interest rates doubled, then investors would simply move their funds to financial instruments with similar characteristics where they could earn a return of 20%. Higher interest rates therefore reduce the market price of existing bonds and lower interest rates increase the market price or value of existing bonds.

UK capital markets can be split into primary and secondary markets.

■ Primary capital markets. New issues of debt and equity are originally placed on the primary capital market and then traded in the secondary market which includes the London Stock Exchange (LSE). The majority of primary markets are ‘over-the- counter’ markets which are a type of market with no location, reporting system or centralized market. In these markets information is dispersed using burgeoning computer networks.

■ Secondary capital markets. These are organized markets that enable the equity and debt of issuing companies to be traded. The ability to trade debt on a secondary market is an important part of any capital market, because it allows holders of longterm financial debt to liquidate their holding for cash at any time, for a known return. This means that new issues are more likely to be purchased. Also the holders of marketable financial claims can more readily maximize their utility by rearranging their consumption and risk profiles over time.

At the heart of the capital market in the UK is the LSE. The LSE has a physical location where equity and debt instruments can be traded. However, the amount of business transacted on the floor of the LSE is minimal, with the majority of business taking place outside the physical location of the exchange using telephones and new technology. The market can be split into two: the Main Market, which is the largest and is where the majority of equity and debt prices are quoted; and the Alternative Investment Market (AIM) which opened in July 1995 to allow smaller companies access to the secondary market (see Chapter 4).

A major factor concerning capital markets today is the growing competition between financial centres, especially those within Europe. Traditionally, London has been the busiest European capital market: for example, the amount of international banking business undertaken from London at the beginning of the 1990s was three times that of the next busiest European country. Reasons advanced for this dominance have included London’s geographical position between New York and Tokyo, the large amount of foreign banks operating in London, the availability of trained staff, and London’s convenience in reaching the rest of Europe.

However, with the evolution of the Single Market, the increasing globalization of businesses and the advancement of technology, the competition from other financial centres has become intense. This has meant that European companies requiring long-term finance are increasingly looking throughout the European financial centres and not just at London.

The Bank of England and the sterling wholesale money markets

Having introduced both the Bank of England and the sterling wholesale money markets, it will be useful to consider the operations of the Bank of England in the money markets and the ways in which it seeks to influence the short-term interest rate.

We have already noted that setting interest rates is now the concern of the MPC which operates within the Bank of England. The aim of the Bank’s operations on the money markets is to guide short-term interest rates to the level set by the MPC. The Bank does this by providing liquidity or cash to the banking system at the interest rate set by the MPC and by buying government securities at prices consistent with the interest rate set by the MPC. This exerts pressure on the short-term money market rate of interest to move to the ‘official’ rate set by the MPC.

To be able to do this, the Bank of England manages its accounts in ways which will ensure that the banking system as a whole is short of liquidity. The Bank of England can ‘tighten’ bank liquidity in the following ways.

■ Through taxation. When people pay their taxes they do so from their bank accounts; the flow of these payments to the Bank of England (on behalf of the government) drains the banking sector of liquidity.

■ Through government borrowing. Selling government securities (e.g. Treasury bills) to individuals or institutions who pay for them from their bank accounts.

■ Through buying short-term claims on banks. Such ‘claims’ are via the Bank of England lending to the banks for short periods. A number of these claims mature throughout the day and must be redeemed by the banks, draining them of liquidity.

■ Through regulations. For example, regulations which require the clearing banks to maintain positive end-of-day balances with the Bank of England.

The Bank of England is aware that banks will always look to the money markets in general, and the Bank of England in particular, should they need to restore their liquidity. At this point the Bank will offer such liquidity at a ‘price’, namely one which will reinforce the interest rate level set by the MPC.

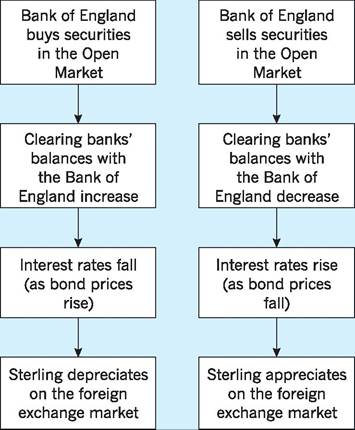

The Bank of England can, for example, raise shortterm interest rates by first starving the banking sector of liquidity and then offering to restore that liquidity at its official rate of interest. This intervention often comes in the form of Open Market Operations (OMOs) on the money market. Figure 21.3 provides a simplified overview of such OMOs. Where the

Fig. 21.3 Open Market Operations of the Bank of England.

Bank of England wants to raise interest rates it sells securities, and vice versa.