Mergers and acquisitions in the growth of the firm

A well-established maxim suggests that a company must grow if it is to survive. Mergers and acquisitions have become two of the more widely used methods of achieving growth in recent years, accounting for about 50% of the increase in assets and 60% of the increase in industrial concentration.

The years 1984-89, 1994-2000 and 2003-07 provided a sustained merger boom, in that the expenditure on mergers was extremely high compared to the number of mergers involved. This chapter examines the types of merger activity, such as horizontal, vertical, conglomerate and lateral mergers, and the motives for such activity. These include financial motives which may be related to valuations placed on a firm's assets, the desire to increase ‘market power' or to secure economies of scale and managerial motives related more to firm growth than to profitability. Trends in merger activity and legislation affecting merger activity are considered in both the UK and the EU. The UK approach to mergers is then contrasted with that of the US. The chapter concludes with a brief review of recent tendencies to de-merge.Definitions

One of the most significant changes in the UK’s industrial structure during this century has been the growth of the large-scale firm. For example, the share of the 100 largest private enterprises in manufacturing net output has risen from 22% in 1949 to a maximum of 42% in 1975, before falling back to around 34% by 2010. Most of the growth in size was achieved by acquisition or merger rather than by internal growth.

A merger takes place with the mutual agreement of the management of both companies, usually through an exchange of shares of the merging firms with shares of the new legal entity. Additional funds are not usually required for the act of merging, and the new venture often reflects the name of both the companies concerned.

A takeover (or acquisition) occurs when the management of Firm A makes a direct offer to the shareholders of Firm B and acquires a controlling interest. Usually the price offered to Firm B shareholders is substantially higher than the current share price on the stock market. In other words, a takeover involves a direct transaction between the management of the acquiring firm and the stockholders of the acquired firm. Takeovers usually require additional funds to be raised by the acquiring firm (Firm A) for the acquisition of the other firm (Firm B), and the identity of the acquired company is often subsumed within that of the purchaser.

Sometimes the distinction between merger and takeover is clear, as when an acquired company has put up a fight to prevent acquisition. However, in the majority of cases the distinction between merger and takeover is difficult to make. Occasionally the situation is complicated by the use of the words ‘takeover’ and ‘merger’. For example, in 1989 the press announced that SmithKline Beckman, the US pharmaceutical company, had ‘taken over’ the UK company Beecham for £4,509m. However, technically speaking it was a ‘merger’ because a new company SmithKline Beecham was created which acquired the shares of the two constituent companies to form a new entity.

There are two types of ‘barriers’ which can be employed by companies attempting to deter hostile takeovers:

■ ‘Poison pill’ barrier: This often involves company rules that allow the shareholders to buy new shares in their company at a large discount, should that company be threatened by a hostile takeover. The now enlarged pool of shareholders makes it more difficult and more expensive for the acquiring firm to complete the takeover. In the US, some 40% of the 5,500 companies tracked by Institutional Shareholder Service, a research organization, have been found to employ the ‘poison pill’.

■ ‘Staggered board’ barrier: These involve company rules which allow different groups of directors to be elected in different years.

This is likely to deter hostile takeovers since it may be many years before the acquiring company will be able to dominate the existing boardroom of the target company. Institutional Shareholder Service estimates that some 60% of US companies have a staggered board. Lucian Bebchuk of Harvard Business School argues that staggered boards cost shareholders around 4 - 6% of their firm’s market value by allowing entrenched managers and directors to resist takeover bids which would be attractive to the majority of shareholders (Bebchuk and Fried 2004).Types of merger

Four major forms of merger activity can be identified: horizontal integration, vertical integration, the formation of conglomerate mergers, and lateral integration.

Horizontal integration

This occurs when firms combine at the same stage of production, involving similar products or services. During the 1960s over 80% of UK mergers were of the horizontal type, and despite a subsequent fall in this percentage, some 80% of mergers in the late 1990s were still of this type. The merger of Royal Insurance and Sun Alliance to form Royal & Sun Alliance in 1996, Imperial Tobacco’s acquisition of the German tobacco firm Reemtsma Cigarettenfabriken in 2002, and the Resolution Life Group’s acquisition of the Britannic Group in 2005 were all examples of horizontal mergers. So too was the merger of Delta Airlines with Northwest Airlines in the US, which was finally consolidated in 2010, resulting in Delta Airlines becoming the world’s largest passenger carrier.

Horizontal integration may provide a number of economies at the level of both the plant (productive unit) and the firm (business unit).

Plant economies may follow from the rationalization made possible by horizontal integration. For instance, production may be concentrated at a smaller number of enlarged plants, permitting the familiar technical economies of greater specialization, the dovetailing of separate processes at higher output,1 and the application of the ‘engineers’ rule’ whereby material costs increase as the square but capacity as the cube.

All these lead to a reduction in cost per unit as the size of plant output increases. When Kraft, the US food giant, acquired Cadbury, the UK confectioner, for £11.9bn in 2010, becoming the world’s largest confectioner, cost savings of £675m per year were identified from rationalization of production and scale economies. Similarly the huge fabricated chip manufacturing plants (‘Fabs’) cost over $3bn each, roughly twice as much as previous plants, but are able to produce over three times as many silicon chips per time period, with such ‘plant economies’ reducing the unit cost per chip by over 40%.Firm economies result from the growth in size of the whole enterprise, permitting economies via bulk purchase, the spread of similar administrative costs over greater output, and the cheaper cost of finance, etc. The renamed and expanded Air France-KLM airline formed in 2004 estimated cost savings from such ‘firm economies’ of around £200m over the following five years from economies in functional areas such as sales, distribution, IT and procurement.

Vertical integration

This occurs when the firms combine at different stages of production of a common good or service. Only about 5% of UK mergers are of this type. Firms might benefit by being able to exert closer control over quality and delivery of supplies if the vertical integration is ‘backward’, i.e. towards the source of supply. Factor inputs might also be cheaper, obtained at cost instead of cost + profit. The takeover of Texas Eastern, an oil exploration company, by Enterprise Oil in 1989, serves as an example of backward vertical integration. Of course, vertical integration could be ‘forward’ - towards the retail outlet. This may give the firm merging ‘forward’ more control of wholesale or retail pricing policy, and more direct customer contact. An example of forward vertical integration towards the market was the acquisition by the UK publishing company Pearson plc of National Computer Systems (NCS) in 2000 for £1.6bn.

NCS was a US global information service company providing Internet links and curriculum and assessment testing facilities for schools. The takeover allowed Pearson to design integrated educational programmes for schools by providing students with customized learning and assessment testing facilities. It could also use the NCS network to reach both teachers and parents. In this way, Pearson was able to use its NCS subsidiary to sell its existing publishing products while also developing new on-line materials for the educational marketplace. An example of ‘backward’ vertical integration can be seen in the case of the US aircraft company Boeing, which bought out its parts suppliers Vought Aircraft in 2009 and Global Aeronautics in 2008, in order to control the supply chain for its 787 Dreamliner plane which had fallen behind in terms of its production schedule.Vertical integration can often lead to increased control of the market, infringing monopoly legislation. This is undoubtedly one reason why they are so infrequent. Another is the fact that, as Marks and Spencer have shown, it is not necessary to have a controlling interest in suppliers in order to exert effective control over them. Textile suppliers of Marks and Spencer send over 75% of their total output to Marks and Spencer. Marks and Spencer have been able to use this reliance to their own advantage. In return for placing long production runs with these suppliers, Marks and Spencer have been able to restrict supplier profit margins whilst maintaining their viability. Apart from low costs of purchase, Marks and Spencer are also able to insist on frequent batch delivery, cutting stockholding costs to a minimum.

Conglomerate merger

This refers to the adding of different products to each firm’s operations. Diversification into products and areas with which the acquiring firm was not previously directly involved accounted for only 13% of all mergers in the UK in the 1960s. However, by the late 1980s the figure had risen to 34%.

The major benefit is the spreading of risk for the firms and shareholders involved. Giant conglomerates like Unilever (with interests in food, detergents, toilet preparations, chemicals, paper, plastics, packaging, animal feeds, transport and tropical plantations - in 75 separate countries) are largely cushioned against any damaging movements which are restricted to particular product groups or particular countries. The various firm economies outlined above may also result from a conglomerate merger. The ability to buy companies relatively cheaply on the stock exchange, and to sell parts of them off at a profit later, became an important reason for conglomerate mergers in the 1980s. The takeovers by Hanson plc of the Imperial Group, Consolidated Goldfields and the Eastern Group in 1986, 1989 and 1995 respectively provide good examples of the growth of a large conglomerate organization.The classic example of a conglomerate is the Indian Tata Group which has over 90 operating companies in six business groups, namely communication and information technology, consumer products, engineering, materials, services and chemicals. It owns, for example, Tata Steel, Tata Motors and Tata Chemicals - all major players in international business. With a group revenue of $67.4bn in 2010 with 57% of its companies operating outside India, Tata is a truly global conglomerate.

Another example of conglomerate integration involves Procter & Gamble (P&G), the US multinational, which is the world’s largest consumer group conglomerate, owning brands such as Pringles crisps, Pampers nappies and Crest toothpaste. In recent years it has broadened its portfolio of products still further into haircare, acquiring Nioxin, a US scalp care company in 2009, Gillette hair care products in 2005, the German haircare company, Wella, in 2003 and Clairol in 2001. The various ‘firm (enterprise) economies’ outlined above may also result from a conglomerate merger. P&G expects to save ˆ300m annually from its purchase of Wella by economies from combining back-office activities, media buying, logistics and other purchasing activities.

ate merger. The term ‘lateral integration’ is often used when the firms which combine are involved in different products, but in products which have some element of commonality. This might be in terms of factor input, such as requiring similar labour skills, capital equipment or raw materials; or it might be in terms of product outlet. The Swiss company TetraLaval’s offer for the French company Sidel in 2001 (which was finally cleared by the EU competition authorities in 2002) provides an example of the difficulty of distinguishing the concepts of conglomerate and lateral integration. TetraLaval designs, manufactures and sells packaging for liquid food products as well as manufacturing and marketing equipment for milk and farm products. Sidel designs and sells machines used in the manufacture of plastic bottles and packaging. The European Commission regarded the merger as conglomerate in that the companies operated in different sectors of the market and were to be organized, post merger, into three distinct entities within the TetraLaval Group. However, it was still the case that the merger would resemble a case of lateral integration in that the companies had a commonality of experience in the packaging and container sector.

Economic theory and merger activity

A number of theories have been put forward to explain the underlying motives behind merger activity. However, when these various theories are tested empirically the results have often been inconsistent and contradictory. An interesting survey article on merger activity in 1989 noted that as many as fourteen separate motives were frequently cited in support of merger activity (Mueller 1989). Despite these obvious complications, it may be useful at this stage to explain some of the main factors which seem to motivate mergers, if only to understand the complexity of the process.

Lateral integration

The value discrepancy hypothesis

This is sometimes given separate treatment, though in practice it is difficult to distinguish from a conglomer- This theory is based on a belief that two of the most common characteristics of the industrial world

are imperfect information and uncertainty. Together, these help explain why different investors have different expectations of the prospects for a given firm.

The value discrepancy hypothesis suggests that one firm will bid for another only if it places a greater value on the firm than that placed on the firm by its current owners. If Firm B is valued at VA by Firm A and VB by Firm B then a takeover of Firm B will only take place if VA > VB + costs of acquisition. The difference in valuation arises through Firm A’s higher expectations of future profitability, often because A takes account of the improved efficiency with which it believes the future operations of B can be run.

It has been argued that it is in periods when technology, market conditions and share prices are changing most rapidly that past information and experience are of least assistance in estimating future earnings. As a result differences in valuation are likely to occur more often, leading to increased merger activity. The value discrepancy hypothesis would therefore predict high merger activity when technological change is most rapid, and when market and share price conditions are most volatile.

Evidence

Gort’s (1969) test of the value discrepancy hypothesis in the USA gives some support, finding a statistically significant relationship between merger rate and the parameters noted above. His hypothesis that value discrepancy drives merger activity, especially during periods of rapid shifts in market prices, seems to have some validity. Later researches by Shleifer and Vishny (2003) and Rhodes-Kroopf and Viswanathan (2004) seem to show that relatively different valuations of companies by potential acquirers and bidders often drive merger waves.

Interestingly, recent work on mergers and acquisitions has tended to concentrate on the relationship between industry-level shocks (and associated expec- tational changes) and merger activity, so reminiscent of the Gort hypothesis. For example, one such study (Andrade et al. 2001) indicates that mergers which occurred between the 1970s and the 1990s were often the result of industrial shocks triggered by technological innovations (which can create excess capacity and the need for industry rationalization), supply-side shocks (e.g. oil price changes) or industrial deregulation (greater competition). Similarly, Jovanovich and Rousseau suggest that technological shocks, to the extent that they do not affect all players in an industry equally, can lead to capital relocation as managers try to restructure industry though mergers and acquisitions (Jovanovich and Rousseau 2004).

Arguably the UK merger booms of the late nineteenth century, the 1920s, the 1960s, the mid-1980s and the 1990s often occurred during periods characterized by industry-level shocks. However, although the industrial shock theory with its effects on expectations does give some indication of the forces at work in merger activity, it does not always give sufficient insight into the particular reasons behind such merger activity.

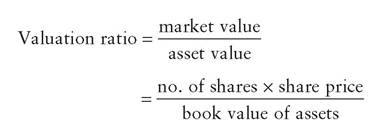

The valuation ratio

One factor which may affect the likelihood of takeover is the valuation ratio, as defined below:

If a company is ‘undervalued’ because its share price is low compared to the value of its assets, then it becomes a prime target for the ‘asset stripper’. If a company attempts to grow rapidly it will tend to retain a high proportion of profits for reinvestment, with less profit therefore available for distribution to shareholders. The consequence may be a low share price, reducing the market value of the firm in relation to the book value of its assets, i.e. reducing the valuation ratio. It has been argued that a high valuation ratio will deter takeovers, whilst a low valuation ratio will increase the vulnerability of the firm to takeover. In the early 1980s, for example, the property company British Land purchased Dorothy Perkins, the womenswear chain, because its market value was seen as being low in relation to the value of its assets (prime high street sites). After stripping out all the freehold properties for resale, the remainder of the chain was sold to the Burton Group.

In recent years the asset value of some companies has been seriously underestimated for other reasons. For example, many companies have taken years to build up brand names which are therefore worth a great amount of money; but it is often the case that

these are not given a money value and are thus not included in the asset value of the company. As a result, if the market value of a company is already low in relation to the book value of its assets, then the acquirer gets a double bonus. One reason why Nestle was prepared to bid £2.5bn (regarded as a ‘high’ bid, in relation to its book value) for Rowntree Mackintosh in 1988 was to acquire the ‘value’ of its consumer brands cheaply, because they were not shown on the balance sheet. Finally, it is interesting to note that when the valuation ratio is low and a company would appear to be a ‘bargain’, a takeover may originate from within the company; in this case it is referred to as a management buyout (MBO).

Evidence

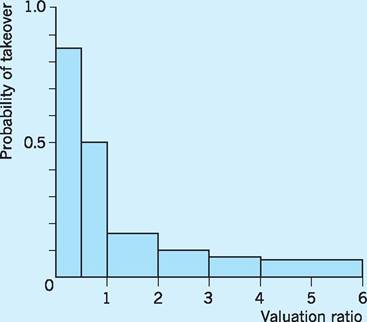

Kuehn (1975), in his study of over 3,500 companies in the UK (88% of companies quoted on the Stock Exchange) between 1957 and 1969, found that those firms which maintained a high valuation ratio were much less susceptible to takeover. Figure 5.1 indicates this inverse relation between valuation ratio and the probability of acquisition. The suggestion is that potential raiders are deterred by the high price to be paid, reflecting a more realistic market valuation of the potential victims’ assets. However, the valuation ratio may not be as important as Kuehn’s study implies. For example Singh (1971), in a study of takeovers in five UK industries (which included food, drink and electrical engineering industries) between

Fig. 5.1 Valuation ratio and probability of takeover.

1955 and 1960, found that a relatively high valuation ratio may not always guarantee protection against takeover. An even stronger conclusion against the valuation ratio hypothesis was drawn by Newbold (1970), when he compared the valuation ratios of ‘victim’ firms with those of the ‘bidding’ firms during the merger period of 1967 and 1968. His conclusion was that the valuation ratio of actual ‘victim’ firms exceeded the average for the industry in 38 cases but was below the average in only 26 cases. In other words, a high valuation ratio did not seem to deter takeover activity. Levine and Aaronovitch (1981) came to a similar conclusion in their study of 109 mergers in manufacturing and services, noting that as many as 14% of the successful ‘bidding’ firms had a valuation ratio below 1, which one might have expected to result in their becoming ‘victim’ firms.

Some confirmation of the view that a high valuation ratio may not deter takeover activity has come from a survey of merger activity in the US manufacturing and mining sectors, between 1940 and 1985. This survey related merger activity to a measure called the Tobin q. This measure is similar to the valuation ratio explained above, except that the market value of a company is measured against the ‘replacement value’ of the company’s assets. The study found a positive relationship between mergers and the Tobin q, i.e. a high Tobin q or valuation ratio was associated with a high level of merger activity - the reverse of the more usually accepted hypothesis (Golbe and White 1988).

The market power theory

The main motive behind merger activity may often be to increase monopoly control of the environment in which the firm operates. Increased market power may help the firm to withstand adverse economic conditions, and increase long-term profitability.

Three situations are particularly likely to induce merger activity aimed at increasing market power.

1 Where a fall in demand results in excess capacity and the danger of price-cutting competition. In this situation firms may merge in order to secure a better vantage point from which to rationalize the industry.

2 Where international competition threatens increased penetration of the domestic market by foreign firms. Mergers in electronics, computers and engineering have in the past produced combines large enough to fight off such foreign competition.

3 Where a tightening of legislation makes many types of linkages between companies illegal. Firms have in the past adopted many practices which involved collusion in order to control markets. Since restrictive practices legislation has made many of these practices illegal between companies, merger, by ‘internalizing’ the practices, has allowed them to continue.

For these reasons merger activity may take place to increase a firm’s market power. However, the very act of merging usually increases company size, both in absolute terms and in relation to other firms. It is clear, therefore, that increased size will be both a byproduct of the quest for increased market power, and itself a cause of increased market power.

Evidence

Newbold (1970), in his study of 38 mergers between 1967 and 1968, found that the most frequent reason cited by managers for merger activity was risk reduction (48% of all mergers), as firms sought to control markets along the lines of market power theory. These conclusions were substantiated in a study by Cowling et al. (1980) of nine major UK mergers, which concluded that the mergers did generate elements of market power, often to the detriment of consumers. Further support for this view has come from a study of UK merger trends across 200 industry sectors, ranging from pharmaceuticals to road haulage, which showed that merger activity over the period 1991-95 was closely related to industry concentration. Industries with lower concentration ratios tended to be the industries with the highest rates of merger activity as incumbent firms tried to grow larger in order to increase their market power (Schoenberg and Reeves 1999). Similarly, a global research report covering merger deals involving 107 companies worldwide by the accountancy firm KPMG found that as many as 54% of the executives concerned stated that mergers and acquisitions were aimed at gaining new market share, or protecting existing market share (KPMG 1999).

There is also fragmentary evidence that the termination of restrictive agreements encouraged some firms to combine formally. Elliot and Gribbin (1977) found that the five-firm concentration ratio increased faster in industries in which restrictive practices had been terminated than in those in which no such practices existed.

Empirical work does suggest that an increase in the size of a firm raises its market power. For example, Whittington (1980) found that large firms often experience less variability in their profits than small firms, indicating that large firms may be less susceptible to changing economic circumstances as a result of their greater market power. Studies by Aaronovitch and Sawyer (1975) also show that large firms are less likely to be taken over than small or mediumsized ones, and that a given percentage increase in size for an already large firm reduces the probability of takeover much more than the same percentage increase for a small to medium-size firm. It would appear that size, stability and market power are closely interrelated.

It may also be that profitability and market power are closely related. This would seem to be the implication of the results of a survey into 146 out of the top 500 UK firms. A questionnaire was sent to these companies asking for the responses of their respective Chief Executive Officers to a number of questions relating to merger activity (Ingham et al. 1992). From the responses to questions relating to the motives for mergers, the survey found that the single most important reason for mergers and acquisitions was the expectation of increased profitability. This was closely followed by the second most important reason - the pursuit of market power. It is therefore possible that the desire for market power and the profit motive are highly interrelated, or at least are thought to be so by significant ‘players’ in the market.

Nevertheless the actual results of merger activity provide little evidence that any increase in market power is effective in raising firm profitability. For example, Ravenscraft and Scherer (1987) conducted a detailed analysis of 6,000 acquisitions in the US between 1950 and 1976 and revealed that postmerger profitability was generally disappointing, with the profitability of around two-thirds of the merged companies below the average achieved prior to merger. Interestingly, the report by KPMG noted above (KPMG 1999) also found that only 17% of the mergers studied had resulted in an increase in shareholder value, with as many as 53% of the deals actually destroying shareholder value.

Economies of scale

It is often argued that the achievement of lower average costs (and thereby higher profits) through an increase in the scale of operation is the main motive for merger activity. As we noted in the earlier part of this chapter, such economies can be at two levels: first, at the level of the plant, the production unit, including the familiar technical economies of specialization, dovetailing of processes, engineers’ rule, etc.; and second, at the level of the firm, the business unit, including research, marketing, administrative, managerial and financial economies. To these plant- and firm-level economies we might add the ‘synergy’ effect of merger, the so-called ‘2 + 2 > 4’ effect, whereby merger increases the efficiency of the combined firm by more than the sum of its parts. Synergy could result from combining complementary activities as, for example, when one firm has a strong R & D team whilst another firm has more effective production control personnel.

Evidence

Economies of scale seem less important in merger activity than is traditionally supposed. Prais (1976) points out that technical economies, through increased plant size, have played only a small part in the growth of large firms. For instance, the growth of the 100 largest plants (production units) in net output has been much slower than the growth of the 100 largest firms (business units) in net output. Firms seem to grow not so much by expanding plant size to reap technical economies, but by acquiring more plants. Of course, evidence that firms seek to grow as an enterprise or business unit, through adding extra plants, could still be linked to securing ‘firm-level’ economies of scale.

Newbold (1970), however, found that only 18% of firms surveyed admitted to any motive that could be linked to plant- or firm-level economies of scale. Cowling et al. (1980) concluded in similar vein that the ‘efficiency gains’ (economies of scale) from mergers were difficult to identify in the firms examined. Finally, Whittington (1980) found profitability to be independent of firm size, and we have already noted that the study by Ravenscraft and Scherer (1987) saw a decline in the profitability of two-thirds of the now larger combined firms in the period following the mergers. This might also seem to argue against any significant economies of scale, otherwise larger firms, with much lower costs, might be expected to secure higher profits. Similarly, research carried out on the performance of 11 major media companies which had been actively involved in mergers during the period up to 2000 found no significant correlation between firm size (and thus the benefits of economies of scale and scope) and company performance (Peltier 2002).

Although we cannot test the synergy effect directly, there is case evidence that it plays a part in encouraging merger activity. Nevertheless, the hopes of substantial benefits through this effect are not always realized. Unsuccessful attempts at pursuing synergy are widespread, notably by companies who mistakenly believe that they have the management and marketing expertise to turn around loss-making companies into efficient, profitable ventures. Indeed the survey by Ingham et al. (1992), mentioned earlier, placed the ‘pursuit of marketing economies of scale’ as the third most important reason for mergers. However, this reason was given rather infrequently, i.e. it was ranked well behind ‘profitability’ and ‘market power’. Again, although recent EU annual reports on competition policy seem to indicate that the synergies to be derived from ‘combining complementary activities’ are an important motive for merger activity, this reason was also ranked well behind ‘strengthening of market share’ and ‘expansion’.

It is, of course, possible that economies of scale as a rationale for mergers might also be linked to the cyclical patterns of demand. For example, it has been shown that the increased benefits of size in industries in which economies of scale matter often drive mergers around cyclical patterns, with firms seeking to grow larger and benefit from economies of scale when they expect demand to be high and rising (Lambrecht 2004).

Managerial theories

In all the theories considered so far, the underlying principle in merger activity is, in one way or another, the pursuit of profit. For example, market power theory suggests that through control of the firm’s environment, the prospects of profit, at least in the long run, are improved. Economies of scale theory

concentrates on raising profit through the reduction of cost. Managerial theories, on the other hand (see also Chapter 3), lay greater stress on non-profit motives.

With the rise of the public limited company there has been a progressive divorce between ownership by shareholders and control by management. This has given managers greater discretion in control of the company, and therefore in merger policy. The suggestion by Marris, Williamson and others is that a prime objective of managers is growth of the firm, rather than absolute size. In these theories the growth of the firm raises managerial utility by bringing higher salaries, power, status and job security to managers (Marris 1964; Williamson 1967). Managers may therefore be more interested in the rate of growth of the firm than in its profit performance.

Managerial theories would suggest that fastgrowing firms, having already adopted a growthmaximization approach, are the ones most likely to be involved in merger activity. These theories would also suggest that fast-growing firms will give higher remuneration to managers, and will raise job security by being less prone to takeover.

Evidence

It does appear that it is the fast-growing firms that are mainly involved in merger activity. For example, Singh (1971, 1975) noted that the acquiring firms had a significantly higher growth rate than the acquired firms, and possessed many of the other attributes of a growth maximizer, such as a higher retention ratio (see Chapter 3), higher gearing and less liquidity (Chapter 2). Similarly, Aaronovitch and Sawyer (1975) reported that in the period before an acquisition, the acquiring firm generally grew much faster than the acquired firm. Ravenscraft and Scherer (1987) in their major study of 6,000 US acquisitions concluded that the pursuit of growth rather than profit was a key factor in explaining merger activity.

As regards higher managerial remuneration through growth, Firth (1980) found a significant increase in the salaries of directors of the acquiring company after merger. The chairman’s salary increased by an average of 33% in the two years following merger, compared to only 20% for the control group of companies not engaged in merger activity. More recent research carried out between 1985 and 1990 on a sample of 170 UK firms (Conyon and Gregg 1994) showed that the remuneration of the top director was closely related to sales growth. The research also showed that company sales growth through acquisition raised the top directors’ remuneration significantly above that which could have been achieved by internal or organic growth. The research by Schoenberg and Reeves (1999) into UK merger activity in some 200 industrial sectors, referred to above, also found that the frequency of industry-wide mergers was closely related to the growth of sales revenue. This is in line with the growth and managerial utility motives for mergers suggested by Marris and Williamson, respectively.

Managerial theories place less stress on profit performance, and more on growth of the firm. The fact that, at least in the short run, the profit level often deteriorates for the acquiring firms is taken by some as further evidence in support of the managerial approach. A number of studies have showed that firms involved in mergers tended to have lower profitability levels than non-merging firms; in studies by Meeks (1977), Kumar (1985), Cosh et al. (1985) and Ravenscraft and Scherer (1987), mergers were found to have negative effects on profitability.

We have already noted that large firms, whilst not necessarily the most profitable (Meeks and Whittington 1975), were less likely to be taken over than small to medium-sized firms. In fact, any given percentage increase in size was much more significant in reducing the probability of takeover for the large firm than it was for the small to medium-sized firm (Aaronovitch and Sawyer 1975; Singh 1975). The small to medium-sized firm has therefore an incentive to become large, and the large firm still larger, if takeovers are to be resisted. Further evidence in support of the suggestion that small to medium-sized firms are active in acquisitions came from a survey of some 2,000 firms in UK manufacturing industry between 1960 and 1976 (Kumar 1985). The study concluded that there was indeed a tendency for firm growth through acquisitions to be negatively related to firm size. Once firms become large they appear to be more ‘stable’ and less prone to takeover. Such evidence is consistent with managerial theories which stress the importance of growth as a means of enhancing job security for managers. However, it should be noted that the merger boom of the late 1980s showed that even large firms were no longer safe from takeovers; this was in part due to firms now having easier access to the finance required for takeover activity.

The evidence clearly points away from traditional economies of scale, whether at the level of ‘plant’ or ‘firm’, as the motive for merger. Survival of the firm, and control of its environment, seems to be at the heart of most merger activity. This often implies the sacrifice of profit, at least in the short run. Such an observation is consistent with market power and managerial theories, both of which concentrate on objectives other than short-run profit (see also Chapter 3).

I Mergers and the public interest

Although there is clearly much debate about the motivation behind merger activity, there is a broad consensus that the resulting growth in firm size will have implications for the ‘public interest’. Before a more detailed investigation into the legislation and institutions involved in regulating merger activity in the UK, EU and US, it may be helpful to consider the potential impacts of a merger on economic efficiency and economic welfare, which are two key elements in any definition of the ‘public interest’.

Economic efficiency

The idea of economic efficiency may usefully be broken down into two separate elements.

1 Productive efficiency. This involves using the most efficient combination of resources to produce a given level of output. Only when the firm is producing a given level of output with the least-cost methods of production available do we regard it as having achieved ‘productive efficiency’.

2 Allocative efficiency. This is often taken to mean setting a price which corresponds to the marginal cost of production. The idea here is that consumers pay firms exactly what it costs them to produce the last (marginal) unit of output; such a pricing strategy can be shown to be a key condition in achieving a so-called ‘Pareto optimum’ resource allocation, where it is no longer possible to make someone better off without making someone else worse off. Any deviation of price away from marginal cost is then seen as resulting in ‘allocative inefficiency’.

What may pose problems for policymakers is that the impacts of proposed mergers may move these two aspects of economic efficiency in opposite directions. For example, economies of scale may result from the merger having increased firm size, with a lower cost of producing any given output thereby improving productive efficiency. However, the greater market power associated with increased size may give the enlarged firm new opportunities to raise price above (or still further above) its costs of production, including marginal costs, thereby reducing allocative efficiency.

We may need to balance the gain in productive efficiency against the loss in allocative efficiency to get a better idea of the overall impact of the merger on the ‘public interest’.

Economic welfare

Economic welfare is a branch of economics which often involves ideas of consumer surplus and producer surplus.

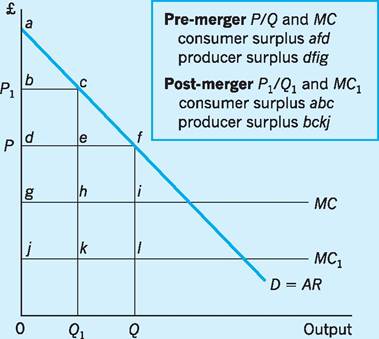

■ Consumer surplus. This is the benefit to consumers of being willing to pay more for a product than they actually have to pay in terms of the going market price. It is usually measured by the area underneath the demand (willingness to pay) curve and above the ruling market price. So in Fig. 5.2, if the ruling market price is P and quantity sold Q, then area afd corresponds to the ‘consumer surplus’, in the sense that consumers are willing to pay OafQ for Q units, but only have to pay OdfQ (price ? quantity), giving a consumer surplus of afd.

■ Producer surplus. This is the benefit to producers of receiving a price higher than the price they actually needed to get them to supply the product. In Fig. 5.2 we shall assume for simplicity that the MC curve is the firm’s supply curve (you should know that this actually is the case in a perfectly competitive industry!). So in Fig. 5.2, if the ruling market price is P and the quantity sold Q, then area dfig corresponds to the ‘producer surplus’, in the sense that producers are willing to supply Q units at a price of g but actually receive a price of P, giving them a producer surplus of dg per unit, and a total producer’s surplus of dfig on all Q units sold.

Fig. 5.2 Mergers, economic efficiency and economic welfare. Welfare gain (ghkj) and welfare loss (cflk) from merger.

Figure 5.2 is useful in illustrating the fact that a proposed merger might move productive and allocative efficiencies in opposite directions. For simplicity we assume the curves displayed to be linear, and the firm to be at an initial price/quantity equilibrium of P/Q with marginal cost MC (for a profit-maximizing firm MR would have intersected MC at point i). Now suppose that the merger/takeover results in the (enlarged) firm2 using its market power to raise price from P to P1, cutting output from Q to Q1, but that at the same time the newly available scale economies cut costs so that MC shifts downwards to MC1.

Clearly we have to balance a loss of allocative efficiency against a gain in productive efficiency in order to assess the overall impact on the ‘public interest’. To do this we can usefully return to the idea of economic welfare, and the associated consumer and producer surpluses.

If we regard the total welfare resulting from a resource allocation as being the sum of the consumer surplus and the producer surplus, we have:

■ pre-merger afd + dfig

■ post-merger abc + bckj

In terms of total welfare (consumer surplus + producer surplus) we can note the following impacts of the merger:

■ gain of welfare ghkj

■ loss of welfare cflk

The ‘gain of welfare’ (ghkj) represents the improvement in productive efficiency from the merger, as the Q1 units still produced require fewer resources than before, now that the scale economies have reduced costs (shifting MC down to MC1).

The ‘loss of welfare’ (cflk) represents the deterioration in allocative efficiency from the merger; price has risen (P to P1) and marginal costs have fallen (MC to MC1), further increasing the gap between price and marginal cost. As a result of the price rise from P to P1, output has fallen from Q to Q1. This loss of output has reduced economic welfare, since society’s willingness to pay for these lost Q - Q1 units (the area under the demand curve from Q - Q1, i.e. cfQQ1) exceeds the cost of producing them (the sum of all the marginal costs from Q - Q1, i.e. klQQ1) by cflk.

Clearly the overall welfare effect (‘public interest’) could be positive or negative, depending on whether the welfare gains exceed the welfare losses, or vice versa (in Fig. 5.2 the losses outweigh the gains). No pre-judgement can therefore be made that a merger will, or will not be, in the public interest. As Stewart (1996) notes, everything depends on the extent of any price rise and on the demand and cost curve configurations for any proposed merger. It is in this context that a Competition Commission (CC) investigation and other methods of enquiry into particular proposals might be regarded as important in deciding whether any merger should proceed or be abandoned.

In 2006 the CC attempted to place a money value on the potential welfare losses to consumers resulting from mergers. The summary of the commission’s findings can be seen in Table 5.1.

The four merger enquiries shown in Table 5.1 were carried out between March 2005 and March 2006. The SDEL/Coors merger involved the equipment used to dispense beer and some other drinks in pubs; the Somerfield/Morrisons deal involved the sale of 115 grocery stores in certain UK locations, raising the problem of local market power; the LSE/Euronext/ Deutsche Borse involved two bids for the London Stock Exchange; and Vue/Ster related to the transfer of six cinemas in the UK from Ster to Vue. The figures in the table attempt to assess the likely price rises resulting from the lessening of competition (SLC) and the associated welfare loss of consumer surplus.

Table 5.1 Estimated costs to consumers of the mergers against which the CC took action between March 2005 and March 2006.

| Inquiry | Estimated costs to consumers per annum (£) |

| SDEL/Coors | 13.9 |

| Somerfield/Morri sons | 5.5 |

| LSE/Euronext/Deutsche | |

| Borse | 11.8 |

| Vue/Ster | 0.3 |

| Total | 31.5 |

| Source: Competition Commission (2006) July, p. 2. | |

The combined welfare loss to the consumers of these projected mergers was calculated to be £31.5m per annum. For example, in the SDEL/Coors deal it was calculated that the merger would have increased the price of beer per barrel by £1, amounting to a loss of consumer surplus of £12m per annum in the UK - plus an estimated additional loss of £1.9m due to quality deterioration. None of these four cases was given permission to merge their activities because of the substantial estimated loss of consumer welfare.

Merger booms

The most notable features which have tended to galvanize merger and takeover activity have often included the following.

1 The growth of national and international markets has created circumstances favourable to economies of scale, while at the same time world tariff barriers have been reduced under the guidance of GATT (now the WTO). The result has been fierce competition between nations which has often led to a rationalization of production since larger firms have been seen as having important cost advantages.

2 Improved communication methods, often involving information/telecommunication technologies, have made it easier for large companies to grow, while the adoption by many companies of a multidivisional structure has encouraged horizontal mergers.

3 There has been a rapid growth in the number and type of financial intermediaries, such as insurance companies and investment trusts. They have begun investing heavily in company equity, thereby providing a ready source of finance for companies who want to issue more shares and then to use the money received to support a takeover bid. At the same time, there has been a dilution of managerial control (see Chapter 3). This ‘divorce of ownership from control’ has made takeover activity easier because directors now have a less close relationship with the company, and are therefore less committed to its continuing in an unchanged form.

4 Many of the periods of intense merger activity have seen an increase in the ‘gearing ratio’ of companies, i.e. an increase in the ratio of debt (debenture and bank borrowing) to shares (equity). Loan finance has proven attractive because the interest paid on debentures and loans has been deducted from company profits before it is taxed. Therefore companies have had a tax incentive to issue loan stock, the money from which they have then been able to use to mount a takeover bid.

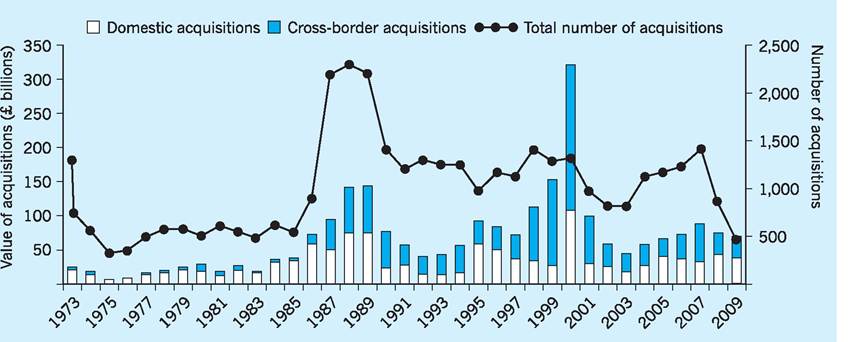

Figure 5.3 shows the trend in UK mergers between 1973 and 2009 in terms of number of acquisitions, their value and also the breakdown according to whether the acquisitions were domestic or cross border.

The motives for such intense takeover activity have been varied. For example, many of the 1985-89 mergers were of the horizontal type, suggesting that one important motive for such activity was production economies arising from rationalization. This motive may have been strengthened by the desire to integrate technology and to improve marketing expertise in order to increase market power. There is also some evidence that target companies in this period tended to be less dependent on debt finance, which suggests that some acquisitions may have been due to the desire of the acquirer to increase cashflow and to reduce its dependency on debt finance. A study of 38 UK takeovers between 1985 and 1987 (Manson et al. 1994) seemed to provide some evidence of such motives. These authors found that the takeovers studied did produce operating gains in terms of both cashflow and market values.

Fig. 5.3 UK mergers 1973-2009.

Source: ONS (2010) Mergers and Acquisitions involving UK Companies, September, and previous issues.

During this period, mergers were largely financed by share issues. The value of the more dynamic bidder’s share would often tend to be higher than the value of the target company’s share, giving the bidder the opportunity to exchange the minimum number of its shares for every one of the target company’s. This meant that the takeover deal was relatively ‘cheap’ for the bidder so that its earnings per share (EPS - total earnings/total number of shares) would not fall too much to worry its existing shareholders and the stock market in general. After the stock market crash in late 1987, however, the decrease in share prices and the rise in interest rates meant that takeovers increasingly involved cash deals rather than share issues.

Merger and acquisition activity during 1992-2009 has been triggered by many factors, including merger opportunities in utilities such as electricity and water, and attempts to secure greater market share in the pharmaceutical, telecommunications and finance industries in order to gain scale economies and provide a base for global expansion. Examples of such mergers in the UK utilities sector include the acquisition of the Lattice Group by the National Grid Group for £5.1bn in 2002 to form National Grid Transco plc, a major supplier of electricity and gas. In the telecommunication industry, the takeover of the German company Mannesmann AG by the UK’s Vodafone Air Touch plc in 2000 created Europe’s largest telecommunication company and accounted for much of the high value figure for mergers in that year. In the same year the £120bn merger of UK companies Glaxo Wellcome and SmithKline Beecham to form GlaxoSmithKline resulted in one of the largest pharmaceutical companies in the world. In the insurance industry, the £1.8bn merger of two UK firms, the Britannic Group and Resolution Life Group, in 2005 created a company with combined assets of over £35bn and helped to reflect the increased merger activity after 2003. The number of acquisitions rose until 2007 before decreasing both in number and value as a result of the insecurity of the global financial crisis and the slowdown in the major economies.

Another feature of the merger trends of the last 35 years is the increasing importance of cross-border acquisitions as a proportion of all mergers involving UK firms. The Single Market and the greater integration of the EU, together with the effects of globalization noted previously, have provided a platform for greater involvement by UK firms in international acquisitions, as was seen in Fig. 5.3.

The control of mergers and acquisitions

We have seen that mergers may be a means of extending market power. We now consider how the UK, the EU and the US have sought to exercise control over merger activity in order to prevent the abuse of such power.

The UK experience

United Kingdom legislation has been tentative in its approach to merger activity, recognizing the desirable qualities of some monopoly situations created through merger; it therefore seeks to examine each case on its individual merits. The first UK legislation, the Monopolies and Restrictive Practices (Inquiry and Control) Act, dates from 1948 and set up the Monopolies Commission. The power of the 1948 Act was extended to mergers by the Monopolies and Mergers Act of 1965 under which the newly established Monopolies and Mergers Commission (MMC) could now report on situations where a merger resulted in a combined market share of 25% or more of a particular good or service, or involved combined assets of over £30m.

The next major Act having implications for merger activity was the Fair Trading Act 1973, under which the Office of Fair Trading (OFT) was formed with a Director-General of Fair Trading (DGFT) as its head. Over the next quarter of a century, the DGFT advised the Secretary of State for Trade and Industry as to which mergers should be referred to the MMC for investigation. However, the Secretary of State could overrule both the DGFT and the MMC if he or she felt that the merger was in the ‘public interest’, which was nowhere clearly defined. This vague ‘public interest’ test often led to complaints by business of undue and arbitrary government involvement in the decision-making process as regards permitting or prohibiting merger activity.

Problems with UK merger policy

As already noted, by the 1990s the effectiveness of the MMC and the role of the Secretary of State in merger investigations were increasingly being called into question. For example, the MMC was criticized for lacking both resources and a professional attitude. It had one full-time chairman, three part-time deputy chairmen, 31 part-time commissioners and only 100 full-time staff. Many argued that the MMC was often ‘outgunned’ by lawyers representing firms under investigation and, with its scarce resources, was unable to properly scrutinize many potentially important merger proposals. For example, between 1950 and 1995 the MMC had investigated only 171 merger cases.

The traditional UK approach to mergers was based on the principle that they can be forbidden by the Secretary of State if they operate against the public interest. The vagueness of the term ‘public interest’, together with the differing approaches to mergers of individual Secretaries of State, led to what many saw as inconsistent decision-making in merger policy over time. For example, the Labour government had recommended in 1978 that the MMC should recognize the benefits as well as the costs of merger activity in their deliberations. However, the following Conservative government issued guidelines in 1984 suggesting that the MMC should concentrate on ‘loss of competition’ as the most important aspect when assessing mergers. By 1992, the Conservative government’s approach to mergers seems to have shifted ground yet again, with the DTI placing greater emphasis on creating ‘national champions’ capable of competing in international markets - thereby supporting larger mergers even when some ‘loss of competition’ was inevitable. Yet by 1996, Ian Laing, the new Conservative Secretary of State for Trade and Industry, announced that ‘fostering competition’ rather than the creation of national champions should be the guideline for assessing merger policy. This followed the refusal of the minister to allow either National Power’s £2.8bn bid for Southern Electric or PowerGen’s £1.9bn bid for Midland Electricity to proceed. These ever-shifting approaches to merger activity indicate some degree of strategic confusion in the implementation of merger policy.

In addition to the problems noted above, there were also increasing complications as regards the power of the Secretary of State during merger references. For example, the Secretary of State had the power to overrule recommendations from both the DGFT and the MMC if he or she was so minded. For example, in 1993 the then Secretary of State at the DTI, Michael Heseltine, rejected the recommendation of the DGFT to refer both GEC’s acquisition of Philips’ infra-red components business and the hostile bid by Airtours for Owners Abroad to the MMC. The Secretary of State argued that the mergers might help rationalize the industry and create strong competitive companies so that, despite the competition-based concerns of the DGFT, he declined to refer these proposed mergers to the MMC for further scrutiny.

Again, in August 1998 Margaret Beckett, the Secretary of State for Trade and Industry, overruled the recommendation of the MMC in the case of First Group, a transport company which had made a £96m acquisition of Glasgow-based SB Holdings. The MMC believed that First Group should be allowed to acquire SB Holdings only if it agreed to sell a division of its Scottish operations to decrease the company’s market power. However, the Secretary of State allowed the merger to proceed without any such restriction on the grounds that a rival company, Stagecoach, had entered the Glasgow bus market, thus creating sufficient competitive conditions.

These inconsistencies in merger policy continued even after the replacement of the MMC by the Competition Commission (CC) under the provisions of the 1998 Competition Act. Again there was criticism of inadequate resources in the CC, which had a relatively small staff of 78 persons and a grant income of only £5.9m, the concern being that it might become a ‘toothless tiger’, used only for appeals against merger decisions rather than itself being a key decision taker. A series of consultation documents were published between 1999 and 2001 culminating in the Enterprise Act of 2002, which received the Royal Assent on November 2002 and was brought into force, in stages, from the spring of 2003 onwards.

Current merger legislation: Enterprise Act 2002

The Enterprise Act 2002 overhauled UK competition law and, amongst other things, restated the UK merger control framework by introducing significant amendments to previous legislation in this area. The main aspects of current merger legislation now include the following.

1 Relevant merger situation. Under the Act, a ‘relevant merger situation’ to which the new procedures potentially apply is one in which three criteria are met:

■ First, that the two or more enterprises involved in the merger cease to be distinct as a result of the merger.

■ Second, that the merger must not have taken place, or have taken place not more than four months before the reference is made to the OFT.

■ Third, either that the enterprise being taken over has a UK turnover exceeding £70m (the ‘turnover test’) or that the merged enterprises together supply, or acquire, at least 25% of all those particular goods or services supplied in the UK or a substantial part of the UK (the ‘share of supply’ test). It is implicit in this criterion that at least one enterprise must trade within the UK.

2 Competition authorities evaluation test. Under the Act, for a ‘relevant merger situation’, the test which the OFT will apply when evaluating whether a merger should be referred to the CC is whether the merger or proposed merger has resulted, or may be expected to result, in a substantial ‘lessening of competition’ within the relevant market or markets in the UK. ‘Lessening of competition’ would generally mean a situation where product choice would be reduced, prices raised, or product quality or innovation reduced as the result of merger activity. However, the OFT might decide not to make a reference to the CC if it believes that customer benefits (e.g. higher choice, lower prices, higher quality or innovation) resulting from the merger outweigh the substantial lessening of competition noted above. Similarly, the CC when considering a merger in more depth will also weigh the ‘lessening of competition’ effect against the ‘public benefits effect’ before making its final decision.

3 Competition authorities. Under the Act, the OFT was established as an independent statutory body and the post of DGFT was abolished.

■ As a result of its new statutory power the OFT can require the provision of information and documents, enter premises under warrant, and seize material. It has explicit duties to keep markets under review and to promote competition. It publishes an annual report on its activities and performance which is laid before Parliament. It also has the functions of advising the Secretary of State on mergers which might fall under the scope of the ‘public interest’.

■ The CC, which was already an independent statutory body, continues its in-depth investigation of any merger cases referred to it by the OFT or less frequently by the Secretary of State. The CC determines the outcome of such cases and reports its decision to the Secretary of State.

■ The Secretary of State for Business, Innovation and Skills has retained power to make decisions for mergers involving newspaper transfers and in certain public interest cases such as those that deal with national security. Apart from these specified types of merger situations, the main decisions relating to mergers are now dealt with by the OFT and CC without resort to the Secretary of State.

■ There is also a new appeals mechanism giving a right to those parties involved in the merger to apply to the Competition Appeal Tribunal (CAT) for a statutory judicial review of a decision of the OFT, CC or the Secretary of State. There is also a further right of appeal (on a point of law only) to the Court of Appeal.

Putting merger policy into practice

To understand the main procedures for merger investigation, a brief account will be given here of the process. When the OFT is made aware of the ‘relevant merger situation’, it may choose to undertake a ‘first stage’ investigation. It might seek to assess the potential effect of the merger on market structure. For example, if it is a horizontal-type merger then market shares, concentration ratios or the Herfindahl-Hirschman Index (see below, p. 100) might be used as initial indicators of potential competition concerns. This market structure assessment could be followed by an examination of whether the entry of new firms into the market is easy or difficult and whether any ‘lessening of competition’ is likely to occur. The OFT will then make its own decision on the case without reference to the Secretary of State. The OFT will give one of three possible decisions.

1 The merger is given an unconditional clearance.

2 The merger is given a clearance only if the parties agree to modify their uncompetitive behaviour or decrease their market power.

3 The merger may turn out to be serious enough to refer it directly to the CC for a ‘second-stage’ investigation. At this point the Secretary of State can intervene in the proceedings, but under the new regime this intervention can be done only in very specific circumstances involving mergers with media, national security or other narrowly specified implications.

If the OFT refers the merger to the CC, the Commission will consider the evidence of the OFT but will also make its own in-depth report on the merger. After consideration of the evidence and basing its views on both the ‘lessening of competition’ and ‘customer benefits criteria’, the CC will recommend that one of three possible actions be taken: (i) an unconditional clearance, or (ii) a clearance subject to conditions proposed by the CC, or (iii) an outright prohibition. If the CC recommends conditional clearance then the companies involved may be asked to divest some of their assets or to ensure in some specified way that competition is maintained (e.g. giving licences to their competitors). Again, the Secretary of State may intervene only in very limited circumstances as in the media, national security or other specified issues (e.g. if one of the parties to the merger is a government contractor). If the decision of the CC is to prohibit the merger, the parties can appeal to the CAT.

In essence, the Enterprise Act has depersonalized competition authority by abolishing the post of DGFT. It has also improved the overall predictability of the mergers investigation procedure by de-politicizing the process of merger control. It has done this by severely curtailing the involvement of the Secretary of State and by giving expert independent bodies (the OFT and CC) more power. Basically, the OFT and CC have been transformed from essentially advisory bodies to the Secretary of State to independent bodies with their own decision-making powers. The Act has also clarified merger control policy by introducing the ‘lessening of competition’ test in place of the old ‘public interest’ test and by allowing potential benefits (including public benefits) to be considered. In addition, the Act made the mergers regime more transparent by obliging both the OFT and the CC to consult fully with companies involved in mergers and provide the parties involved with their provisional findings. Finally, the new mergers regime seeks to introduce a fairness criterion in that companies now have the right of appeal to the CAT.

However, an appeal to the CAT in 2004 created shock waves for the OFT. The OFT had decided not to refer to the Competition Commission a merger between two healthcare IT companies, namely iSOFT and Torax, involved in supplying data systems to the NHS. A third company, IBA Health Ltd, appealed to the CAT that the merger was unfair and would lessen competition. The CAT upheld IBA’s appeal and asked the OFT to reconsider its decision, arguing that the OFT needed to be satisfied that there had been no significant lessening of competition. The OFT then took the case to the Court of Appeal, arguing that the CAT had wrongly interpreted the Enterprise Act 2002. However, in February 2004 the Court of Appeal upheld the CAT’s findings so that this judgment may make the OFT more likely to refer future proposed mergers to the Competition Commission, which some see as leading to a less flexible system of merger control.

The City Code on Takeovers and Mergers

The City Code on Takeovers and Mergers (‘the Code’) was published by the Financial Services Authority (FSA) in April 2001 in order to reinforce London’s reputation for clean and fair financial markets and offer better protection to consumers. The Code is ‘designed to ensure that shareholders are treated fairly and are not denied an opportunity to decide on the merits of a takeover, and that shareholders of the same class are afforded equivalent treatment by an offeror’. In other words, the Code seeks to outline acceptable standards of commercial behaviour as regards the behaviour of offerors and offerees during takeovers or proposed takeovers.

The Code is administered by the Panel on Takeovers and Mergers (‘the Panel’) which was established in 1968 and which now carries out certain regulatory functions in relation to the EU Takeover Directive Regulations 2006. Prior to 2006 the Panel did not have statutory powers, although failure to observe the Code’s provisions could expose FSA-regulated firms to discipline. The Panel’s powers were originally limited to issuing a private reprimand, public censure, or reporting a breach of the Code to the FSA or another body by which the offender is regulated. Since 2006, however, the status of the Panel has been underpinned by legislation in respect of the EU Directive on Takeover Bids noted above. For bids falling within the scope of the EU Directive, the Panel has additional powers to require certain people to produce documents and information, and can apply to a court for enforcement where there is a reasonable likelihood that a person has contravened a Code rule contained within the EU Directive. Although the general aim of the Code continues to be to ensure that takeovers bids are conducted fairly (i.e. with equal treatment for all shareholders), with adequate production of relevant documentation and no special deals or false markets, the penalties for non-compliance are now much higher after adapting the Code to the EU Directive. For example, it will be a criminal offence if a takeover offer document in a bid falling within the scope of the EU Directive fails to contain all the information required by the relevant rules of the Code.

Insider dealing

On a wider issue, the whole question of ‘insider dealing’ came to the fore during this period. This type of dealing occurs when company shares are bought by those who have special privileged information about the future of the company, e.g. the possibility of an imminent takeover. By buying shares before a takeover announcement, for example, they can make huge gains as share prices rise when the excitement of the takeover begins. Basically, the UK has some of the most advanced insider-dealing regulations in the world.

Important UK legislation regulating insider dealing came into force in 1994 and extended the scope of the main Companies Securities (Insider Dealing) Act of 1985. Under the 1993 Criminal Justice Act it is a criminal offence for an individual who has inside information to deal in price affected securities (such as shares, debt securities, gilts and derivatives whose price movements could be sensitive to certain information), or to encourage another person to deal. It is also a criminal offence for such an individual to disclose the information to another person, other than as part of his or her professional work. The dealing in question must be either on a regulated market (basically all EU primary and secondary markets) or off-market but involving professional intermediaries who deal in securities.

However, it has proved difficult to prosecute cases under criminal law and so the Financial Services Markets Act 2000 (FSMA) was passed which provided the opportunity to transfer regulatory powers to the FSA and to overhaul the law. The FSA was given power to impose civil sanctions, including fines, on persons engaged in market abuse, which included insider dealing. The FSMA regime was changed again in January 2003 to comply with the EU Market Abuse Directive (MAD) of that year. MAD was finally implemented in the UK in 2005 through the Market Abuse Regulations 2005, appended to the Act of 2000. An insider is now defined as any person who has access to inside information as a result of certain positions held or activities undertaken. The UK maintains the requirement that for an offence to be committed, the inside dealer must ‘use’ the information when dealing - dealing merely when in possession of inside information is not sufficient to constitute an offence. In February 2006 an FSA committee found that a top manager at the London-based hedge fund GLG Partners LP was guilty of market abuse for selling borrowed Sumitomo Mitsui Financial Group (SMFG) securities after he received confidential information from a salesman at Goldman Sachs Group. The manager and the company were each fined £750,000. In March 2010 a former equities dealer at the stock broker Cazanove was found guilty of insider dealing, having made £103,883 profit from such activity between 2003 and 2004. In this case, criminal proceedings were instigated and the dealer was given a 21 months sentence.

The EU experience

Many European countries have long histories of state intervention in markets so it is hardly surprising that the European Commission accepts the case for intervention by member governments. Apart from agriculture, competition is the only area in which the EU has been able to implement effectively a common policy across member countries. The Commission can intervene to control the behaviour of monopolists and to increase the degree of competition through authority originally derived from the Treaty of Rome. However, the Treaty of Lisbon in 2007 amended the EU’s two core treaties, i.e. the Treaty on European Union (Maastricht Treaty) and the Treaty establishing the European Union (Treaty of Rome). The latter was renamed the Treaty on the Functioning of the European Union (TFEU) and contains three main articles which deal with monopoly and competition.

1 Article 101 prohibits agreements between enterprises which result in the restriction of competition (notably relating to price-fixing, market-sharing, production limitations and other restrictive practices). This article refers to any agreement affecting trade between member states and therefore applies to a large number of British industries.

2 Article 102 prohibits a dominant firm, or group of firms, from using their market power to exploit consumers.

3 Article 107 prohibits government subsidies to industries or individual firms which will distort, or threaten to distort, competition.

Mergers and EU industry

There are significant number of mergers which occur in Europe in any given year, most of which are completed without any problems. However, there are some mergers which may cause distortions in competition and are then notified to the Commission for scrutiny. There were 4,274 notifications to the Commission relating to merger activity between 1991 and 2009, of which some 87% have been given unconditional clearance to continue and only 5% were referred onwards for a more in-depth study. Of these, only 20 or 10% were prohibited. Looking at it another way, of the 4,274 early notifications to the Commission only 20 cases were finally prohibited. An in-depth breakdown of the nature of such notifications can be seen in a more limited sample of notifications to the EU Commission between 1990 and 2002 which were deemed by the Commission to exercise ‘unacceptable’ power within the EU.

The word ‘merger’ is often used to cover a wider range of different types of concentrative activity. In recent years joint ventures and acquisition of the majority of assets accounted for 86% of notifications of mergers and acquisitions to the EU Commission, while ‘agreed bids’ accounted for only 6% of total activity. Of course, mergers and acquisitions can take a variety of formal and less formal structures, with ‘alliances’ sometimes a more accurate term for the emerging relationship. Microsoft and Yahoo entered into an Internet search alliance in 2010, approved by US and EU regulation authorities. Daimler and Renault entered into a cross-shareholding alliance in March 2010 to gain scale economies in small car production, as did Mazda and Toyota in 2010 to share expensive R&D investment costs for hybrid and electric cars.

An interesting strategic view of the merger process has been indicated by surveys of top executives across six of Europe’s most actively acquisitive countries (Angwin and Savill 1997). The results showed that the top four reasons for expanding into other countries through acquisitions were, in order:

■ the growing similarity between both national and EU markets;

■ the ability to find a good strategic fit;

■ establishing a market presence overseas ahead of others; and

■ obtaining greater growth potential at a lower cost abroad than at home.

The most appropriate target company for acquisition was quoted as being a company which has a good strategic fit with the acquirer, is financially healthy, and has a relatively strong market (or market niche) position. Over the last decade corporate mergers have tended to involve the core activities of the merging companies, resulting in more horizontal-type mergers. For example, the purchase by Volkswagen of Rolls- Royce for £430m in 1998 was aimed at strengthening its core activities, with higher volumes permitting the scale economies which might allow more effective competition in world markets, while at the same time improving the strategic fit, since Volkswagen wanted to compete more actively in the luxury car market in which Rolls-Royce had a greater presence.

A number of advantages were cited by the top executives surveyed for using acquisitions rather than joint ventures or other methods of entry into other EU markets, with an important one being that acquisitions were seen as a faster and less risky method of building up a critical mass in another country.

European competition policy has been criticized for its lack of comprehensiveness, but in December 1989 the Council of Ministers agreed for the first time on specific cross-border merger regulations. The criteria for judging whether a merger should be referred to the European Commission covered three aspects. First, the companies concerned must have a combined world turnover of more than ˆ5bn (though for insurance companies the figure was based on total assets rather than turnover). Second, at least two of the companies concerned in the merger must have a Community-wide turnover of at least ˆ250m each. Third, if both parties to the merger have two-thirds of their business in one and the same member state, the merger was to be subject to national and not Community controls.

The Commission must be notified of merger proposals which meet the criteria noted above within one week of the announcement of the bid and it will vet each proposed merger against a concept of ‘a dominant position’. Any creation or strengthening of a dominant position will be seen as incompatible with the aims of the Community if it significantly impedes ‘effective competition’. The Commission has one month after notification to decide whether to start proceedings and then four months to make a final decision. If a case is being investigated by the Commission it will not also be investigated by national bodies such as the British Monopolies and Mergers Commission, for example. Member states may prevent a merger which has already been permitted by the Community only if it involves public security or some aspects of the media or if competition in the local markets is threatened.

Review of EU merger regulation

A number of reservations were expressed about the 1990 legislation. First, a main aim of the legislation was to introduce the ‘one stop shop’ which meant that merging companies would be liable to either European or national merger control and not both. However, as can be seen above, there were situations where national merger control could override EU control in certain instances so that there may be a ‘two stop shop’! Second, it was not clear how the rules would apply to non-EU companies. For example, it was quite possible that two US or Japanese companies each with the required amount of sales in the Community, but with no actual Community presence, could merge. While such a case would certainly fall within the EU merger rules, it was not clear how seriously the Commission would pursue its powers in such cases. Third, guidelines were also needed on joint ventures.

In March 1998 a number of amendments were made to the scope of EU cross-border merger regulations, in effect increasing the number of mergers which can be referred to the EU Commission. The threshold (turnover) figures noted earlier had been criticized for being set at too high a level, so that only large mergers could be referred exclusively to the Commission, thereby meeting the ‘one stop shop’ principle. Of course, such an approach suited many individual member countries of the EU which did not want to cede to the Commission their own national authority to investigate mergers. However, by 1996 the EU Commission had suggested a ‘middle road’ whereby the old higher thresholds could remain but in which other thresholds would be introduced to allow more mergers to be dealt with exclusively by the Commission.