The Value of Innovation in Partial Equilibrium

Let us now turn to the analysis of the value of innovation and R&D to a firm. The equilibrium value of innovation and the difference between this private value and the social value (i.e., the value to a social planner internalizing externalities) will play a central role in our analysis below.

All of the growth models we have studied so far, as well as most of those we will study next, are dynamic general equilibrium models. In fact, as emphasized at the beginning, economic growth is a process we can only understand in the context of general equilibrium analysis. Nevertheless, it is useful to start our investigation of the value of innovation in partial equilibrium, where much of the industrial organization literature starts.Throughout this section, we consider a single industry. Firms in this industry have access to an existing technology that enables firms to produce one unit of the product at the marginal cost ψ > 0. The demand side of the industry is modeled with a demand curve

where p is the price of the product and Q is the demand at this price. Throughout we assume that D (p) is strictly decreasing, continuously differentiable and satisfies the following conditions:

The first ensures that there is positive demand when price is equal to marginal cost, and the second ensures that the elasticity of demand, εD (p), is always greater than 1, so that when we consider monopoly pricing, there will exist a well-defined profit-maximizing price. Moreover, this elasticity is less than infinity, so that the monopoly price will be above marginal cost.

Throughout this chapter and whenever we analyze economies with monopolistic competition, oligopolies or potential monopolies, equilibrium refers to Nash equilibrium or subgame perfect Nash equilibrium (when the game in question is dynamic).

12.3.1. No Innovation with Pure Competition. Suppose first that there is a large number of firms, say N firms, with access to the existing technology. Now imagine that one of these firms, say firm 1, also has access to a research technology for generating a process innovation. In particular, let us simplify the discussion and suppose that there is no 452

uncertainty in research, and if the firm incurs a cost μ > 0, it can innovate and reduce the marginal cost of production to ψ∕λ, where λ > 1. Let us suppose that this innovation is non-rival and is also non-excludable, either because it is not patentable or because the patent system does not exist.

Let us now analyze the incentives of this firm in undertaking this innovation. We first look at the equilibrium without the innovation. Clearly, the presence of a large number of N firms, all with the same technology with marginal cost ψ, implies that the equilibrium price will be pN = ψ, where the superscript N denotes “no innovation”. The total quantity demanded will be D (ψ) > 0 and can be distributed among the N firms in any arbitrary fashion. Since price is equal to marginal cost, the profits of firm 1 in this equilibrium will be  where

where denotes the amount supplied by this firm.

denotes the amount supplied by this firm.

Now imagine that firm 1 innovates, but because of non-excludability, the innovation can be used by all the other firms in the industry. The same reasoning implies that the equilibrium price will be , and total quantity supplied by all the firms will equal

, and total quantity supplied by all the firms will equal

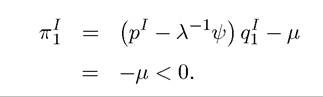

Then, the net profits of firm 1 following innovation will be

Then, the net profits of firm 1 following innovation will be

Therefore, if it undertakes the innovation, firm 1 will lose money.

The reason for this is simple. The firm incurs the cost of innovation, μ, but because the knowledge generated by the innovation is non-excludable, it is unable to appropriate any of the gains from innovation. This simple example underlies a claim dating back to Schumpeter that pure competition will not generate innovation.Clearly, this outcome is potentially very inefficient. For example, μ could be arbitrarily small (but still positive), while λ, the gain from innovation, can be arbitrarily large, but the equilibrium would still involve no innovation. For future reference, let us calculate the social value of innovation, which is the additional gain resulting from innovation. A natural measure of social value is in the sum of the consumer and producer surpluses generated from the innovation. Presuming that after innovation, the good will be priced at marginal cost, this social value is

The first term in the second line is the increase in consumer surplus because of the expansion of output as the price falls from ψ to λ-1ψ (recall that price is equal to marginal cost in this social planner’s allocation). The second term is the savings in costs for already produced units; in particular, there is a saving of λ-1 (λ — 1) ψ on D (ψ) units. Finally, the last term is the cost of innovation. Depending on the shape of the function D (p), the values of λ and μ, this social value of innovation can be quite large.

12.3.2. Some Caveats. The above example illustrates the problem of innovation under pure competition in a very sharp way. The main problem is the inability of the innovator to exclude others from using this innovation. One way of ensuring such excludability is via the protection of intellectual property rights or a patent system, which will create ex post monopoly power for the innovator. This type of intellectual property right protection is present in most countries and will play an important role in many of the models we study below.

Before embarking on an analysis of the implications of ex post monopoly power of innovators, there are a number of caveats we should emphasize. First, even without patents, “trade secrecy” may be sufficient to provide some incentives for innovation. Second, firms may engage in innovations that are only appropriate for their own firm, making their innovations de facto excludable. For example, imagine that at the same cost, the firm can develop a new technology that reduces the marginal cost of production by only λ0 < λ. But this technology is specific to the needs and competencies of the current firm and cannot be used by any other (or alternatively, λ∕λ0 is the “proportional” cost of making the innovation “excludable”). We will show that the adoption of this technology may be profitable for the firm, since the specificity of the innovation firm acts exactly like patent protection (see next subsection and also Exercise 12.5). Therefore, some types of innovations, in particular those protected by trade secrecy, can be undertaken under pure competition.

Finally, a number of authors have recently argued that innovations in competitive markets are possible, when firms are able to replicate the technology and sell it to competitors during a certain interval of time before being imitated by others (e.g., Hellwig and Irmen, 2001, Walde, 2002, and Boldrin and Levine, 2003).

12.3.3. Innovation and Ex Post Monopoly. Let us now return to the same environment as above, and suppose that if firm 1 undertakes a successful innovation it can obtain a fully-enforced patent. Once this happens, firm 1 will have better technology than the rest of the firms, and will possess ex post monopoly power. This monopoly power will enable the firm to earn profits from the innovation, potentially encouraging its research activity in the first place. This is the basis of the claim by Schumpeter, Arrow, Romer and others that there is an intimate link between ex post monopoly power and innovation.

Let us now analyze this situation in a little more detail.

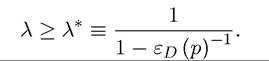

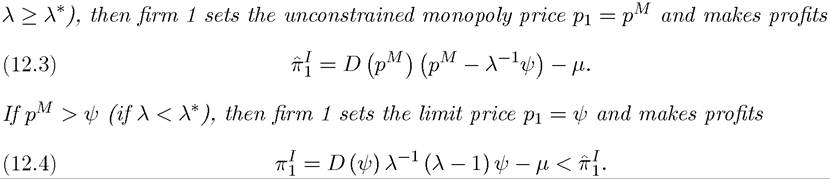

It is useful to separate two cases:(1) Drastic innovation: a drastic innovation corresponds to a sufficiently high value of λ such that firm 1 becomes an effective monopolist after the innovation. To determine which values of λ will lead to a situation of this sort, let us first suppose that firm 1 does indeed act like a monopolist. This implies that it will choose its price to maximize

The first-order condition of this maximization is

Clearly the solution to this equation gives the standard monopoly pricing formula (see Exercise 12.1):

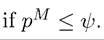

We say that the innovation is drastic It is clear that this will be the case

It is clear that this will be the case

when

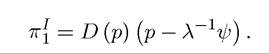

When the innovation is drastic, firm 1 can set its unconstrained monopoly price, pM, and capture the entire market.

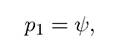

(2) Limit pricing: when the innovation is not drastic, so that or alternatively, when λ < λ*, the equilibrium will involve limit pricing, where firm 1 sets the price

or alternatively, when λ < λ*, the equilibrium will involve limit pricing, where firm 1 sets the price  so as to make sure that it still captures the entire market (since in this case if it were to set pi = pM, other firms can profitably undercut firm 1). This type of limit pricing arises in many situations. In the case we have just discussed, limit pricing results from process innovations by some firms that now have access to a better technology than their rivals.

so as to make sure that it still captures the entire market (since in this case if it were to set pi = pM, other firms can profitably undercut firm 1). This type of limit pricing arises in many situations. In the case we have just discussed, limit pricing results from process innovations by some firms that now have access to a better technology than their rivals.

We summarize this discussion in the next proposition. Recall that the difference between the drastic innovation and limit pricing cases corresponds to different values of λ—i.e., it depends on whether or not λ is greater than λ*.

PROPOSITION 12.1. Consider the above-described industry. Suppose that firm 1 undertakes an innovation reducing marginal cost of production from ψ U (or if

(or if

455

Proof. The proof of this proposition involves solving for the equilibrium of an asymmetric cost Bertrand competition game. While this is standard, it is useful to repeat it, especially to see why in equilibrium, all demand must be met by the low cost firm. Exercise 12.2 asks you to work through the steps of the proof. ?

The fact that is intuitive, since the former refers to the case where λ is greater than λ*, whereas in the latter, firm 1 has a sufficiently low λ that it is forced to charge a price lower than the profit-maximizing monopoly price because of the competition by the remaining firms (still producing at marginal cost ψ).

is intuitive, since the former refers to the case where λ is greater than λ*, whereas in the latter, firm 1 has a sufficiently low λ that it is forced to charge a price lower than the profit-maximizing monopoly price because of the competition by the remaining firms (still producing at marginal cost ψ).

It can also be easily verified that both can be strictly positive, so that with

can be strictly positive, so that with

ex post monopoly innovation becomes possible. This corresponds to a situation in which we start with pure competition, but one of the firms undertakes an innovation in order to escape competition and gains ex post monopoly power. The fact that the ex post monopoly power is important for providing incentives to undertake innovations is consistent with Schumpeter’s emphasis on the role of monopoly in generating innovations.

Now returning to the discussion in the previous subsection, we can also see that trade secrecy or innovations that are specific only for the needs of the firm in question will act in the same way as ex post patent protection in encouraging innovation (see Exercise 12.5).

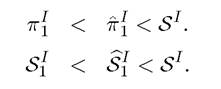

Note also that the expressions for and in this proposition also give the value of innovation to firm 1, since without innovation, it would make zero profits. Given this observation, we now contrast the value of innovation for firm 1 in these two regimes with the social value of innovation, which is still given by (12.1). Moreover, we can also compare social values in the equilibrium in which innovation is undertaken by firm 1 (who will charge the profit-maximizing price) to the full social value of innovation in (12.1), which applies when the product is priced at marginal cost. The equilibrium social surplus in the regimes with monopoly and limit pricing (again corresponding to the cases in which λ is greater than or less than λ*) can be computed as

and in this proposition also give the value of innovation to firm 1, since without innovation, it would make zero profits. Given this observation, we now contrast the value of innovation for firm 1 in these two regimes with the social value of innovation, which is still given by (12.1). Moreover, we can also compare social values in the equilibrium in which innovation is undertaken by firm 1 (who will charge the profit-maximizing price) to the full social value of innovation in (12.1), which applies when the product is priced at marginal cost. The equilibrium social surplus in the regimes with monopoly and limit pricing (again corresponding to the cases in which λ is greater than or less than λ*) can be computed as

We then have the following result:

456

Proposition 12.2. We have that

Proof. See Exercise 12.3. ?

This proposition states that the social value of innovation is always greater than the private value in two senses. First, the first line states that a social planner interested in maximizing consumer and producer surplus will always be more willing to adopt an innovation, because of an appropriability effect; the firm, even if it has ex post monopoly rights, will be able to appropriate only a portion of the gain in consumer surplus created by the better technology. Second, the second line implies that even conditional on innovation, the gain in social surplus is always less in the equilibrium supported by ex post monopoly than the gain that the social planner could have achieved (by also controlling prices). Therefore, even though ex post monopoly power (for example, generated by patents) can induce innovation, the incentives for innovation and the equilibrium allocations following an innovation are still inefficient. Note also that can be negative, so that a potentially productivity-enhancing process innovation can reduce social surplus because of the cost of innovation, μ. However, it can be shown that

can be negative, so that a potentially productivity-enhancing process innovation can reduce social surplus because of the cost of innovation, μ. However, it can be shown that which implies that excessive innovation is

which implies that excessive innovation is

not possible in this competitive environment (see Exercise 12.4). This will contrast with the results in the next subsection.

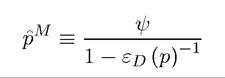

12.3.4. The Value of Innovation to a Monopolist: The Replacement Effect. Let us now analyze the same industry as in the previous subsection, but assuming that firm 1 is already an unconstrained monopolist with the existing technology. Then with the existing technology, this firm would set the monopoly price of  and make profits equal to

and make profits equal to

If it undertakes the innovation, it will reduce its marginal cost to and still remain an unconstrained monopolist. Therefore, its profits will be given by

and still remain an unconstrained monopolist. Therefore, its profits will be given by as in (12.3), with the monopoly price pM given by (12.2). Now the value of innovation to the monopolist is

as in (12.3), with the monopoly price pM given by (12.2). Now the value of innovation to the monopolist is

457

Proposition 12.3. We have that

so that a monopolist always has lower incentives to undertake innovation than a competitive firm.

Proof. See Exercise 12.6. ?

This result, which was first pointed out in Arrow’s (1962) seminal paper, is referred to as the replacement effect. The terminology reflects the intuition for the result; the monopolist has lower incentives to undertake innovation than the firm in a competitive industry because with its innovation will replace its own already existing profits. In contrast, a competitive firm would be making zero profits and thus had no profits to replace.

An immediate and perhaps more useful corollary of this proposition is the following:

Corollary 12.1. An entrant will have stronger incentives to undertake an innovation than an incumbent monopolist.

The potential entrant is making zero profits without the innovation. If it undertakes the innovation it will become the ex post monopolist and make profits equal to Both of

Both of

these are greater than the additional profits that the incumbent would make by innovating,  This is a direct consequence of the replacement effect; while the incumbent would be replacing its own profit-making technology, the entrant would be replacing the incumbent. The replacement effect and this corollary imply that in many models entrants have stronger incentives to invest in R&D than incumbents.

This is a direct consequence of the replacement effect; while the incumbent would be replacing its own profit-making technology, the entrant would be replacing the incumbent. The replacement effect and this corollary imply that in many models entrants have stronger incentives to invest in R&D than incumbents.

The observation that entrants will often be the engine of process innovations takes us to the realm of Schumpeterian models. Joseph Schumpeter characterized the process of economic growth as one of creative destruction, meaning a process in which economic progress goes hand-in-hand with the destruction of some existing productive units. Put differently, innovation is driven by the prospect of monopoly profits. Because of the replacement effect, it will be entrants, not incumbents, that undertake greater R&D towards inventing and implementing process innovations. Consequently, innovations will displace incumbents and destroy their rents. According to Schumpeter, this process of creative destruction is the essence of the capitalist economic system. We will see, especially in Chapter 14, that the process of creative destruction can be the essence of economic growth as well.

In addition to providing an interesting description of the process of economic growth and highlighting the importance of the market structure, the process of creative destruction is important because it also brings political economy interactions to the fore of the question of economic growth. If economic growth will take place via creative destruction, it will create losers, in particular, the incumbents who are currently enjoying profits and rents. Since we 458

expect incumbents to be politically powerful, this implies that many economic systems will create powerful barriers against the process of economic growth. Political economy of growth is partly about understanding the opposition of certain firms and individuals to technological progress and studying whether this opposition will be successful.

There is another, perhaps more surprising, implication of the analysis in this subsection. This relates to the business stealing effect, which is closely related to the replacement effect. The entrant, by replacing the incumbent, is also stealing the business of the incumbent. The above discussion suggests that this business stealing effect helps closing the gap between the private and the social values of innovation. It is also possible, however, for the business stealing effect to lead to excessive innovation by the entrant. To see the possibility of excessive innovation, let us first look at the total surplus gain from an innovation starting with the monopolist. Suppose to simplify the discussion that the innovation in question is drastic, so that if the entrant undertakes this innovation, it can set the unconstrained monopoly price pM as given by (12.2) above. Therefore, the social value of innovation is S1i as given by (12.5).

Proposition 12.4. It is possible that

so that the entrant has excessive incentives to innovate.

Proof. See Exercise 12.8. ?

Intuitively, the social planner values the profits made by the monopolist, since these are part of the “producer surplus”. In contrast, the entrant only values the profits that it will make if it undertakes the innovation. This is the essence of the business stealing effect and creates the possibility of excessive innovations. This result is important because it points out that, in general, it is not clear whether the equilibrium will involve too little or too much innovation. Whether or not it does so depends on how strong the business stealing effect is relative to the appropriability effect discussed above.

12.4.

More on the topic The Value of Innovation in Partial Equilibrium:

- The Value of Innovation in Partial Equilibrium

- The Dixit-Stiglitz Model and “Aggregate Demand Externalities”

- Contents

- Table of contents

- Innovation by Incumbents and Entrants and Sources of Productivity Growth

- References and Literature

- A Baseline Model of Schumpeterian Growth

- References and Literature

- The Lab-Equipment Model of Growth with Input Varieties

- Baseline Model of Directed Technological Change