digital competencies

Let us first focus on the ways banks could improve their operations to serve the digital customer better. Authors Henk Broeders and Somesh Kannah outline a framework consisting of four dimensions along which banks can create value with digital competencies.2 These dimensions are:

■ Connectivity

■ Decision making

■ Automation

■ Digitization

Broeders and Kannah believe banks need to build stronger connections to their customers by using digital technologies in their operations.

Opening new communication channels also improves the connectivity between their staff and their suppliers. By using Big Data and advanced analytics, banks may make better decisions, for instance in sales, product design, pricing, underwriting, and user experience for their customers. Paperless operations, automation and straight-through processing (STP) already help banks to streamline their workflows. But they can also automate recommendations to customers, such as information about new products or trading opportunities in their portfolios, which would reduce the overhead that banks need to spend on customer relations. The final goal is for banks to adopt a digitally centered business model in which digitization enables rapid innovation, automation, and communication. Does such a recommendation make sense? It does, but we believe it could still go farther.It becomes clear when looking at the Broeders and Kannah framework that banks already are keenly aware of those areas in their operations that need innovation. Many financial institutions already invest heavily to acquire these competencies and move aggressively to adopt new technology. Several securities exchanges and major banking houses have already integrated STP, the prime example of automation and digitization.3 Barclays launched its Pingit app for exchange marketplace payments by smartphone two years before most of the other banks even considered it.4 However, exactly where banks should invest to make the leap into the 21st century is a difficult decision.

The popularity of apps and their platforms can change within a few months, which can destroy years of development and investment in a specific infrastructure. It is less about ticking boxes to show that banks have fulfilled certain key performance indicators for their digital strategy, and more about creating long-lasting competitive advantage and value for customers.14.1.1 Banks lag in some areas and lead in others: Analytics

At the same time, online lenders already use technology heavily to improve their operations along the four dimensions we have just discussed. In that regard, they should be the ideal examples of companies that banks should emulate. However, lending platforms have glaring deficits in other areas, such as analytics and risk management. It might seem simple, but analytics for marketplace lending are extremely complex, much more so than assessing the risk in the loan book of a bank. Marketplace lending has no central entity—it connects lenders

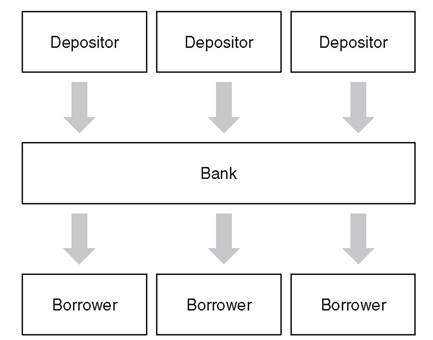

FIGURE 14.1 Financial system with banks as intermediators

and borrowers directly—so it is easy to argue that investors are solely responsible for the risk they take on. Still, even if each investor bears the risk of his own investments, the aggregate exposure to potentially risky assets weakens the stability of the financial system. If push comes to shove, we should have an idea what might happen with this exposure under stress conditions. Because many feedback loops exist between lenders and borrowers in marketplace lending, getting an idea of the risk that such lending imposes in the financial system is a complex exercise.

Compare Figure 14.1 and Figure 14.2: Figure 14.1 shows a simplification of how the formal financial sector works. With banks at the core of the interaction between depositors

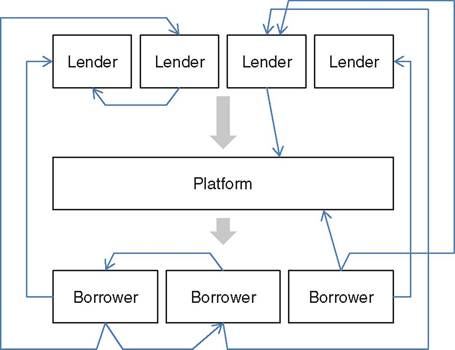

FIGURE 14.2 Complex system with marketplace platforms as intermediators

and borrowers, the system has relatively few feedback loops between individual parties in the economy. Sure, the financial crisis of 2007/8 was a harsh reminder that uncertainty still exists despite the claim of banks to have securitized risk and uncertainty.

However, instead of an implosion in the crisis, central banks stepped in and stabilized the system by infusing capital in banks. Banks can also be borrowers in their own right, and they can lend the capital they borrow. However, this introduces nothing new into the discussion about linear systems versus complex systems, and therefore we have left it out of Figure 14.1.Granted, banks are complex organisms in their own right, and so is the formal financial sector. Despite their complexity, both have succeeded in reducing uncertainty and shifted it towards risk that they can manage. By compartmentalizing the moving parts of a complex system into manageable and separate segments, banks have gotten a grip on uncertainty.

The picture is different when marketplace platforms facilitate credit between individual borrowers and lenders. In Figure 14.2, multiple interactions between individual parties in the economy exist. Even with a limited number of lenders, borrowers, and platforms, there will be countless permutations of possible linkages and feedback loops between agents. Of course, feedback can be positive or negative, where it either increases or decreases the actions of another party. Simply put, if individual borrowers default, they impose stress on individual lenders. If these lenders are also borrowers, perhaps even on other, seemingly unrelated platforms, the initial stress cascades from one actor to the next. Untangling the source of the stress can be extremely difficult, and it is unclear whose responsibility it is to mitigate stress and stabilize a complex system.

Compared to banks, platforms have not managed to reduce uncertainty. They may mitigate risk with diversification, but the uncertainty still remains in the system. Because of an almost unlimited number of feedback loops between the actors in marketplace lending, understanding the relationships of individual agents is difficult. More work is necessary to gain a clearer picture of the risk in complex financial systems.

We already know that platforms make the point that individual lenders are responsible for the risk they choose to take on. However, not even marketplace lending platforms themselves are modeling the complexity of the interactions they facilitate. They would have some of the necessary information to do so, but they often claim that their job in analytics only goes as far as rating borrowers. Risk management and risk analytics beyond counterparty risk are still entirely borne by lenders. At the same time, the only analytics available on platforms are limited. They mainly focus on expected rates of return, without taking into account expected nominal losses. Digging deeper and analyzing the loan books that some platforms make available—as we did by modeling potential losses in Chapter 13—adds a few more pieces to the analytics puzzle. Still, it hardly captures the overall picture of risk in the shadow banking sector.

Marketplace lending platforms recommend diversifying investments across many different loans. When investors do this, the risk in the underlying contracts still remains. What will happen if a crisis hits the economy and borrowers default en masse? In the absence of historical data, given the young age of the online lending sector, it is tricky to make a prediction of possible losses in a portfolio of marketplace loans under stress.

When it comes to financial regulation, marketplace lenders operate on a different playing field to the banks they are trying to disrupt. Most online lenders have a limited set of rules to comply with, and they are largely flying under the radar of regulators. It is unrealistic to assume they will be able to duck this oversight forever. The recommendations of Broeders and Kannah for banks to create value with digital competencies are a starting point. Stephen Hawking pointed out that he thought the next century would be the century of complexity5— coping with it will be the next challenge that banks and online lenders face.

14.2

More on the topic digital competencies:

- digital competencies

- FORCES OF COMPETITION IN THE DIGITAL AGE

- Index

- Contents

- WHY DO BANKS HAVE DIFFICULTY IN INNOVATING?

- Contributions

- P3.1 DANGERS OF A BIG BANG APPROACH TO CATCH UP WITH TECHNOLOGY INNOVATION

- Salient Features of the Legal Framework for the BPO

- DISENTANGLING BUSINESS STRATEGY FROM THE BUSINESS MODEL CONCEPT

- FRAMEWORKS TO ANALYZE THE IMPACT OF INNOVATION