Effective annual rate

To be really precise we need to note that this is not the effective annual rate (EAR) because we have failed to allow for the fact that after one-quarter of a year we receive £100 (after investing £99.902746) and this can be reinvested for a second, third and fourth three-month period within the year.

Interest can be earned accumulatively on each subsequent three-month period and added to the original capital invested. In other words, the original investment is compounded more than once in the year. To calculate the EAR (if we can assume that in the next three quarterly periods the interest rate is the same as in the first three months):

Another example

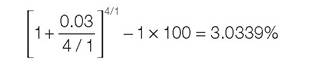

You invest for three months and receive a ‘simple' annual yield of 3%. This is an annual rate that does not take into account compounding over the year - i.e. interest received on interest, added after each quarter. With compounding the effective annual rate is:

Thus, over a period of one year you receive an extra 0.0339% because after the first three-month period you reinvest the maturity amount, including interest from the first investment, in an identical investment for the next three of the remaining nine months. And do the same after six months and nine months. Thus you receive interest on interest received of 0.0339%. This is, of course, assuming identical investments every three months. While this is unrealistic, at least the EAR provides a gauge of the ‘true' annual rate offered on short-term securities.

Purchase price

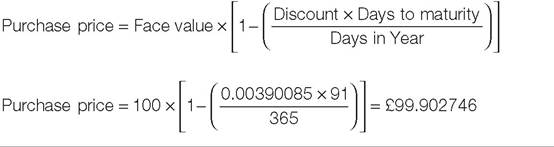

To calculate the price to be paid if the discount yield is 0.390085% we need to start with the face value and take away the discount that applies when the term is only one-quarter of the year or, more strictly, for 91/365th of the year.

The annualised rate of discount of 0.390085 is decreased by multiplying by 91/365.

The purchase price is the face value of 100 multiplied by 1 minus the discount for this portion of the year:

Note that the purchase price is often called the settlement amount. This is because the bill is paid for on the settlement day rather than the transaction or bargain day, which is usually one day earlier in the secondary market.

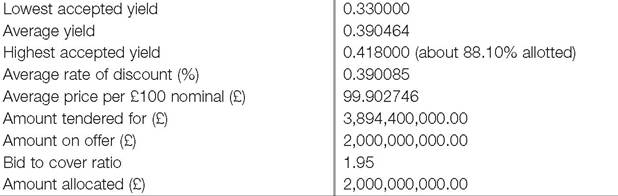

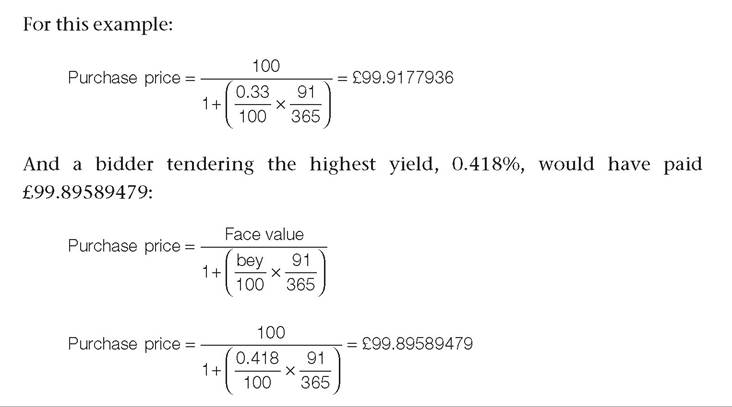

The results for the tender of this 24 March bill are in Table 14.2. The actual bids from buyers varied from a yield (bey) of 0.33% to a high of 0.418% with an average yield of 0.390464%.

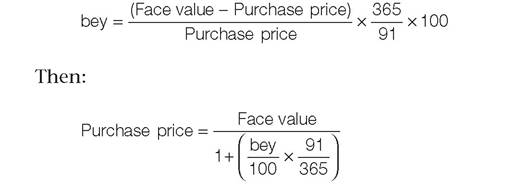

A bidder tendering the lowest accepted yield, 0.33%, would have paid £99.9177936 for their bills:

If:

Table 14.2 Results of tender on three-month T-bill

3 months Treasury bill maturing on 23-Jun-2014, ISIN CODE: GB00B7P4VP73

During the life of a bill, its value fluctuates daily as it is traded between investors - see Table 14.3, which gives the daily March and April 2014 figures for this particular bill.

Table 14.3 Data for Treasury bill GB00B7P4VP73, 21 March to 16 April 2014

| ISIN code | Redemption date | Close of business date | Price (£) | Yield (%) |

| GB00B7P4VP73 | 23-Jun-14 | 21-Mar-14 | 99.903464 | 0.388 |

| GB00B7P4VP73 | 23-Jun-14 | 24-Mar-14 | 99.905141 | 0.385 |

| GB00B7P4VP73 | 23-Jun-14 | 25-Mar-14 | 99.906352 | 0.384 |

| GB00B7P4VP73 | 23-Jun-14 | 26-Mar-14 | 99.907558 | 0.384 |

| GB00B7P4VP73 | 23-Jun-14 | 27-Mar-14 | 99.908762 | 0.383 |

| GB00B7P4VP73 | 23-Jun-14 | 28-Mar-14 | 99.911712 | 0.384 |

| GB00B7P4VP73 | 23-Jun-14 | 31-Mar-14 | 99.913389 | 0.381 |

| GB00B7P4VP73 | 23-Jun-14 | 01-Apr-14 | 99.914615 | 0.380 |

| GB00B7P4VP73 | 23-Jun-14 | 02-Apr-14 | 99.915802 | 0.380 |

| GB00B7P4VP73 | 23-Jun-14 | 03-Apr-14 | 99.916987 | 0.379 |

| GB00B7P4VP73 | 23-Jun-14 | 04-Apr-14 | 99.919921 | 0.380 |

| GB00B7P4VP73 | 23-Jun-14 | 07-Apr-14 | 99.921688 | 0.376 |

| GB00B7P4VP73 | 23-Jun-14 | 08-Apr-14 | 99.922855 | 0.376 |

| GB00B7P4VP73 | 23-Jun-14 | 09-Apr-14 | 99.924018 | 0.375 |

| GB00B7P4VP73 | 23-Jun-14 | 10-Apr-14 | 99.925176 | 0.374 |

| GB00B7P4VP73 | 23-Jun-14 | 11-Apr-14 | 99.926169 | 0.385 |

| GB00B7P4VP73 | 23-Jun-14 | 14-Apr-14 | 99.929775 | 0.372 |

| GB00B7P4VP73 | 23-Jun-14 | 15-Apr-14 | 99.930889 | 0.371 |

| GB00B7P4VP73 | 23-Jun-14 | 16-Apr-14 | 99.932055 | 0.370 |

The price increases as the days to maturity decrease (all else remaining the same) and on redemption day, in this case 23 June 2014, the holder will receive the face value of £100.

The yield in Table 14.3 is the (annual) return (bey) that a purchaser in the secondary market will achieve between purchase date (the settlement date is one day after the close of business transaction date) and maturity date. We can check these figures, using 8 April as the purchase date:

More on the topic Effective annual rate:

- Bill of exchange

- Pressures for Depreciation and Appreciation Since 1994

- Chapter 59 Impact of Microfinance Bank Credit Scheme

- Bahrain