In Terms of Budget Performance and Its Macroeconomic Results

The pandemic process stopping life, which is an important obstacle to the economy, is tried to be controlled all over the world through the measures taken. This way, it is intended to stimulate economic life and particularly unemployment.

The most important tool for this is demand-side policies. Maintaining the purchasing power, production and demand is considered lifesaver for the economy.The economic stimulus packages announced all over the world provide for compensation of the compulsory liabilities of the enterprises during the pandemic, no job loss in employment and supporting the segments with reduced purchasing power. Stable and regular income promises of some countries are stuck to various management levels.

Indicators in the economy will provide information about the actual situation from past to present. The determining effect of economic expectations, moral values and other intangible factors on the economy should not be neglected as well as the actual situation. This is also observed in many studies on the effect of the trust atmosphere on the economy. Therefore, the opinions that explain the economy as a result of expectations and positive developments are remarkable. The behaviours of the owners of the factors of production, formed by the information and impressions they receive from the markets, also shape the economy. The behaviour of decisionmaking units in the economy will also be a guide about developments. In this part of the study, evaluations will be made on Confidence Indices, Capacity Utilization Rates and Budget Balances.

8.5.1 Evaluation on Confidence Indexes

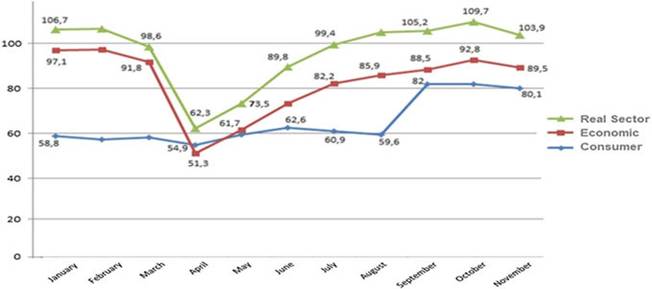

We can have an opinion about the effect of the support structures in Turkey, by referring to the developments in Real Sector Confidence Index, Consumer Confidence Index and Economic Confidence Index. It is important, for the evaluations to be made by sectors, in terms of showing which sectors it affects.

The great impact of

Fig. 8.1 Trends of confidence index. Source 1t was compiled from TU1K data and prepared by US

the epidemic showed itself by stopping life in the second quarter of the year. Therefore, the pessimistic outlook drawn by all three confidence indices examined can be seen in the figure below (Fig. 8.1).

The first index to be evaluated under this title is the Consumer Confidence Index, which has been followed since the beginning of the pandemic, since all citizens are essentially consumers. Seasonally adjusted net consumer trends survey conducted in cooperation with Turkish Statistical 1nstitute and the Central Bank of Republic of Turkey, monthly measures, by means of consumer trends survey, financial situation of consumers and current situation assessments of the overall economy. Future expectations, spending and saving trends are also included in this index. Confidence index reacted in the same way in times of great breakdowns during the pandemic. Its weight in the Economic Confidence Index is 20%.

All confidence indices calculated from the survey results take values between 0 and 200. 100 represents the mean. The fact that the consumer confidence index is above 100 reflects optimism in consumer confidence. A value under 100 indicates a pessimistic situation in consumer trust. The recovery in domestic demand is directly reflected in consumer confidence. The low level of consumer confidence compared to all other indicators for a long time caused the intervention by those concerned with the indicators and distribution. It is observed that the results of the new data set developed since September are also reflected in the index.

The second index to be considered is the Real Sector Confidence Index (RSCI). It is a survey that gives an idea about the general impression of real sector representatives on the economic outlook. In the real sector confidence index, which has a share of 40% in Economic Confidence, the answers given to different questions under the Business Tendency Survey are evaluated together.

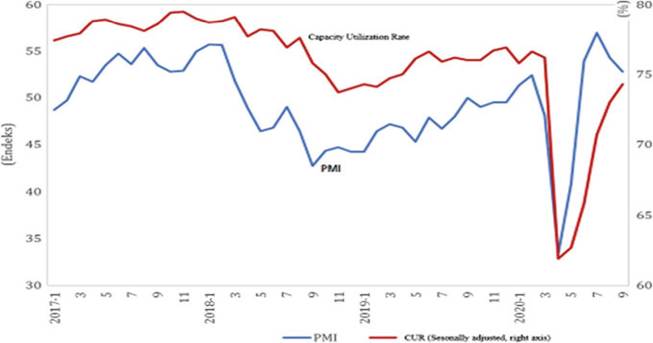

Considering the developments in Fig. 8.1, it is clear that industrial production continues to increase with the liberalization following the measures in the second half of the year. Especially since July, the reference value has been exceeded. 1t is observed that the demand has increased with

Fig. 8.2 PMI and capacity utilization rate. Source Republic of Turkey Presidency Strategy and Budget Directorate (2020)

the effect of the economic support packages provided. As a result, the RSCI score exceeded 100 even in the pandemic period (Fig. 8.2).

Developments in Capacity Utilization Ratios also support RSCI developments. These developments in capacity utilization are important in showing how prepared the economy is to respond positively. The slowdown seen in all sectors during the pandemic process resulted in a rapid recovery response for some sectors. These observations for 24 sub-sectors show that 21 sub-sectors have recovered positively.

The developments, which include the developments in Capacity Utilization Ratios, together with the Purchasing Managers Index (PMI) results announced by the Istanbul Chamber of Industry, show that the process is parallel to each other.

The favourable outlook of the data on RSCI, PMI and Capacity Utilization Rates for the third quarter of the year is a result of optimistic expectations in industrial production. This will affect other developments in the manufacturing industry.

The recovery in domestic demand is observed towards the end of the second quarter, when the pandemic bans were relatively lifted, reflected in the figures. Growth figures from the second half have also accompanied this revival.

Undoubtedly, low levels of interest rates have been the trigger for economic activity. Thus, a consumption-side demand increase is observed in loan utilization rates. Especially, the cuts in loan interest rates in June, a development that affects many sectors together, increased sales from automotive to housing, from white goods to furniture and even to the tourism sector (Fig.

8.3).However, considering to Turkey’s employment structure, the largest share of employment belongs the services sector (55%). As regards the share of other sectors in employment, it is seen that the share of industry is 20%, agriculture 19% and construction 6%. Consequently, the services sector is naturally the sector that is highly affected by the pandemic process, since it includes tourism, entertainment,

Fig. 8.3 Sectoral confidence index. Source Prepared by the authors with the data obtained frιm Turkish Statistical Institute

food and beverage. 2020 is a lost year for the industry. It is not possible to meet the expectations.

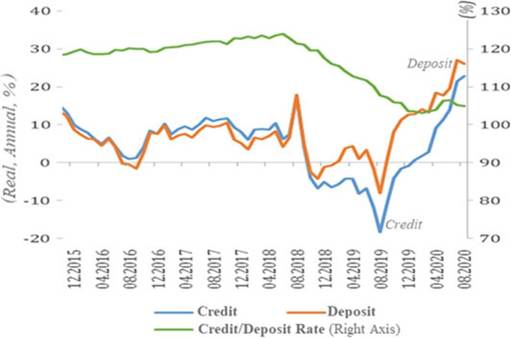

8.5.2 Evaluations on Credit Usage Rates and Tourism Data

The recovery in domestic demand started to be reflected in controlled environments as of the second half of the year. Growth will be supported in this process. The reduction in loan rates, especially in June, has been a sign of revival, especially in automobile and white goods sales. The deferred consumption demand has also improved with low loan rates. 1n this period, it was observed that the Central Bank of Republic of Turkey interest rate cuts created an abundance of liquidity and limited the negative impact on funding costs. Consumption trend limited due to the pandemic has entered an increasing trend with low interest loans, whose usage have been facilitated. However, the negativity and uncertainties prevailing in the international markets undoubtedly suppress the domestic market.

As regards the loans/deposits balance, which shows how much of the deposits in banks are used as loans and which is one of the indicators of the long-term liquidity position of the sector, the deposits have been below the loans since the exchange rate spikes in 2018. 1t is observed that loans, which were above deposits in previous years, increased significantly, and it is led by the public banks during the pandemic (Fig.

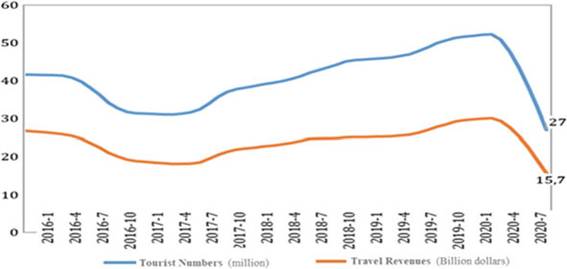

8.4).Tourism revenues, which have been deemed as smokeless industry for years and considered as an important revenue factor in the current account deficit, are far from expectations in 2020. Considering 2020 Tourism data, the number of tourists

Fig. 8.4 Credit and deposit rates balance. Source Republic of Turkey Presidency Strategy and Budget Directorate (2020)

and tourism revenues declined by 70% as of September compared to 2019, due to closures and since the tourists could not come. Year-end tourist expectation also increases the negativity in employment data. As a result, 3.5 million people actively working in tourism are either employed in other sectors or willing to agree to partial work allowance.

Achieving one-third of the Turkey’s $50 billion tourism potential should even be seen as a great success for the current pandemic period. However, the weight of service sector in employment is considerably high in Turkey, as noted above. The sector most affected by the pandemic is the travel and tourism sector due to restrictions.

The tourism sector contributes to the current account balance, which should be evaluated separately. Especially in foreign trade, deficits arising from the balance of goods can reach 100 billion from time to time. However, tourism is an important resource in compensating these amounts. In this period, due to insufficient resources from tourism, it can be expected to have a negative result on the 2020 current account deficit balance of 20 billion dollars for now (Fig. 8.5).

8.5.3 Evaluations on Public Balances

When Turkey faced the pandemic in 2020, along with the rest of the world, it had already been making effort, in 2018, to overcome the effect of the exchange rate experienced in 2019. Fight against inflation, which was the Turkey’s main focus, was suddenly put to the backburner, and combatting the pandemic and its consequences came to the fore.

However, the fragile nature of the ongoing financial stability and

Fig. 8.5 Tourist numbers and tourism revenue. Source Republic of Turkey Presidency Strategy and Budget Directorate (2020)

vulnerability, ongoing due to Turkey’s geopolitical risks, has led to an exchange rate-interest impasse. As a result, an interest rate increase has become inevitable. 1n the short term, this will mean inflation. This means that all financial policy scenarios will have to be handled from scratch. 1t will not be easy to focus on growth on the one hand and become vulnerable to interest pressure on the other to curb the exchange rate and use all these tools during such a pandemic process.

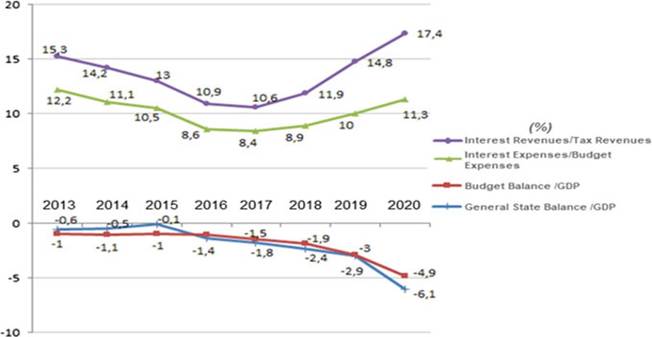

1t is not easy to combat the socio-economic effects of the pandemic that has been going on since March 2020, to manage this without cutting expenses while having income losses. The wide-ranging tax and cash supports announced by the state mean the state gives up some revenues, and cash supports can be interpreted as the continuation of expenditures. 1n addition, cheap loans offered with a low interest policy can be considered a kind of support. All these combatting policies have an aspect to increase budget expenditures and decrease the revenues. The compensation for declining budget revenues is also made through borrowing, which increases the state’s debt burden (Fig. 8.6).

The pandemic process has caused a significant erosion in the state’s revenue sources. Tax amnesty announced as required by the period will not be sufficient to compensate for the revenue. The budget deficit will continue, which is already seen in the 2020 realization estimates and projections for 2021.

The Maastricht Criteria, which the government has long regarded as a criterion, has been exceeded for 2020. The share of budget deficits in GDP is 4.9%. The general government deficit is 6.1%. Although 3% has been maintained for 2019, it does not seem easy to overcome the effects of this pandemic process in a short time.

The interest burden is increasing. The share of interest in budget expenditures is 11.3%. The interest approached again the main budget items such as education and health expenditures. Approximately 1/5 of the taxes is spent for interest, which means both insufficient tax collection and high interest expense. Decreases in the collection/accrual rates of taxes, especially during the pandemic, may also mean revenue and service weakness for the state. 1t is inevitable for the state which cannot

Fig. 8.6 Budget balance and interest expenses. Source Republic of Turkey Presidency Strategy and Budget Directorate (2020)

collect taxes to borrow in this period. Therefore, borrowing will also increase interest expenditures.

8.5.4 Managing the Risks

All the economies hurled by the pandemic in 2020 had the risk of losing their assets first. They could not fulfil their due obligations as well as their normal current liabilities. Speaking of loans, instalments and taxes, they also could not pay their dated cash debts. First of all, the businesses that defer their obligations due to the state both for themselves and through support packages have been effective in declining collection/accrual rates. This led the state, as the biggest decision-making unit and managing the crisis, to be more cautious and make controlled decisions considering its current revenue losses.

While businesses are trying to survive, “concentration in the service sector”, which is a general trend in the employment of all developed economies, has been effective in the service sector coming to the fore as the most affected sector of the pandemic process. This rate is 52%, even for Turkey. Although it varies from country to country in Europe, the share of the services sector, which reaches 60%, in total employment, has decreased to 40% in this process. Job losses at the level of 15% are well above the current unemployment figures.

Although the positive atmosphere of the vaccine is promising, the destructive effects of the epidemic do not seem to easily recover in a short time. Even 2021 contains signs that this struggle will continue. Inadequate demand and income distribution disorders, especially ongoing unemployment, continue to be a significant threat (Pehlivanli 2020).

8.6

More on the topic In Terms of Budget Performance and Its Macroeconomic Results:

- What Macroeconomists Do

- Some Instances of Technological Innovations in the Complex Market Economy

- Theory of the firm

- References

- The Open Corporation

- The Invisible Hand in the Self-Organization of the Market

- Chapter 65 An Empirical Investigation on Credit Card Adoption in Indi

- SOCIAL STRUCTURE IN SCIENCE

- XAT 2009

- SUBJECT INDEX