FACTORS CONTRIBUTING TO NPAS

The banking sector has been facing the serious problems of the rising NPAs. But the problem of NPAs is more in public sector banks when compared to private sector banks and foreign banks (Pradeep, 2007).

The NPAs in PSB are growing due to external as well as internal factors.External Factors

• Ineffective Recovery Tribunal: The Govt. has numbers of recovery tribunals which works for recovery of loans and advances. Due to their negligence and ineffectiveness in their work the bank suffers the consequence of non-recovery, thereby reducing their profitability and liquidity.

• Willful Defaults: There are borrowers who are able to pay back loans but are intentionally withdrawing it. These groups of people should be identified and proper measures should be taken in order to get back the money extended to them as advances and loans.

• Natural Calamities: This is the major factor which is creating alarming rise in NPAs of the PSBs. Every now and then India is hit by major natural calamities thus making the borrowers unable to pay back loans. Thus, banks have to make large amount of provisions in order to compensate loans, hence, reduces profit. Mainly our farmers depend on rain fall for croing. Due to irregularities of rainfall the farmers are not achieving the production level thus they are not repaying the loans.

• Industrial Sickness: Improper project handling, ineffective management, lack of adequate resources, lack of advance technology, day to day changing govt. policies give birth to industrial sickness. Hence, the banks that finance those industries ultimately end up with a low recovery of their loans reducing their profit and liquidity.

• Lack of Demand: Entrepreneurs in India could not foresee their product demand and starts production which ultimately piles up their product thus making them unable to pay back the money they borrow to operate these activities.

The banks recover the amount by selling off their assets which covers a minimum level. Thus, the banks record the non-recovered part as NPAs and have to make provision for it.• Change on Govt. Policies: With every new govt. banking sector gets new policies for its operation. Thus, it has to cope with the changing principles and policies for the regulation of the rising of NPAs. The fallout of handloom sector is continuing as most of the weavers co-operative societies have become defunct largely due to withdrawal of state patronage. The rehabilitation plan worked out by the Central government to revive the handloom sector has not yet been implemented. So the over dues due to the handloom sectors are becoming NPAs.

Internal Factors

Defective Lending Process

There are three cardinal principles of bank lending that have been followed by the commercial banks since long.

Principles of safety: By safety it means that the borrower is in a position to repay the loan (both principal and interest). The repayment of loan depends upon the borrowers:

◦ Capacity to pay.

◦ Willingness to pay.

Capacity to pay depends upon

◦ Tangible assets

◦ Success in business

Willingness to pay depends on

Character

Honesty

Reputation of borrower

The banker should, therefore, take utmost care in ensuring that the enterprise or business for which a loan is sought is a sound one and the borrower is capable of carrying it out successfully. He should be a person of integrity and good character.

Inappropriate Technology

Due to inappropriate technology and management information system, market driven decisions on real time basis cannot be taken. Proper MIS and financial accounting system is not implemented in the banks, which leads to poor credit collection, thus resulting in NPA. All the branches of the banks should be computerized whether urban or rural.

Improper SWOT Analysis

The improper strength, weakness, opportunity and threat analysis is another reason for the rise in NPAs.

While providing unsecured advances the banks depend more on the honesty, integrity, financial soundness and credit worthiness of the borrower. Banks should consider the borrowers own capital investment and should collect credit information of the borrowers:1. From the bankers.

2. Enquiry from market/segment of trade, industry, business.

3. From external credit rating agencies.

Poor Credit Appraisal System

Poor credit appraisal is another factor for the rise in NPAs. Due to poor credit appraisal the bank gives advances to those who are not able to repay. They should use good credit appraisal to decrease the NPAs.

Managerial Deficiencies

The banker should always select the borrower very carefully and should take tangible assets as security to safeguard its interests. When accepting securities banks should consider the:

1. Marketability

2. Acceptability

3. Safety

4. Transferability.

The banker should follow the principle of diversification of risk based on the famous maxim “do not keep all the eggs in one basket”; it means that the banker should not grant advances to a few big firms only or to concentrate them in few industries or in a few cities. If a new big customer meets misfortune or certain traders or industries affected adversely, the overall position of the bank will not be affected (Prasad, 2004).

Position of Scheduled Commercial Banks

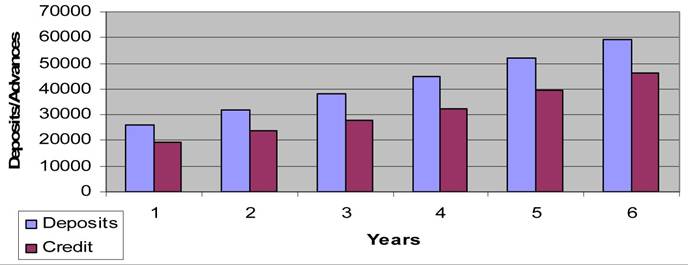

Table 1 reveals the details of deposits and advances of scheduled commercial banks in India from the last six years. The figures exhibits that the deposits of SCBs increased from Rs. 26119.33 Table 1. Deposits and advances of scheduled commercial banks in India (in billion)

| Years | Deposits | Credit |

| 2007 | 26119.33 | 19311.89 |

| 2008 | 31969.39 | 23619.14 |

| 2009 | 38341.10 | 27755.49 |

| 2010 | 44928.26 | 32447.88 |

| 2011 | 52079.69 | 39420.82 |

| 2012 | 59090.82 | 46118.52 |

Source: www.rbi.org.in

billion in 2007 to Rs. 59090.82 billion in 2012.

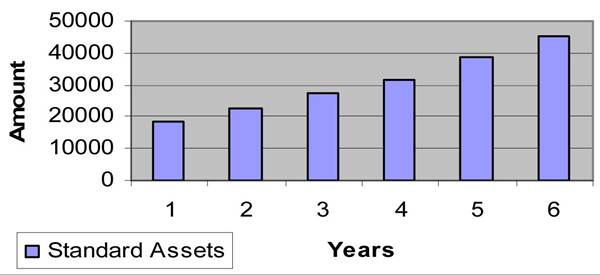

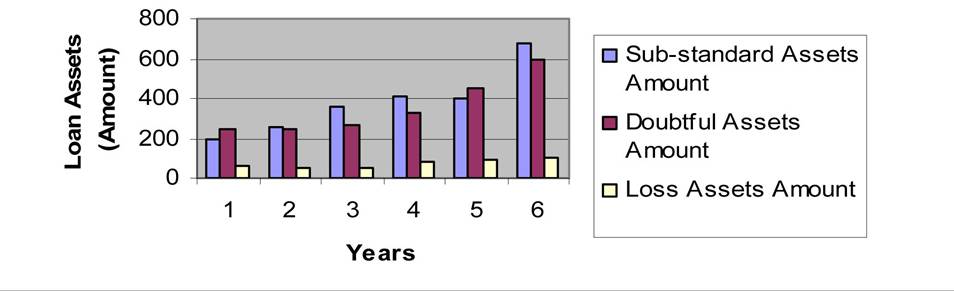

The advances also shows an increasing trend i.e. the amount increased from Rs. 19311.89 billion in 2007 to Rs. 46118.52 billion in 2012. Thus, it can be concluded that both (i.e. deposits and advances) have been increasing but the amount of advances as compared to the deposits is less (Figure 1).Table 2 represents the classification of loan assets of scheduled commercial banks in India. Standard assets generate continuous income and repayments as and when they fall due. So, no special provision is required for them. As per the table above the amount of standard assets register a hike of 18,433.97 billion in 2007 to Rs. 45,284.48 billion in 2012. This shows that the SCBs are in good position The amount of sub-standard assets also increased from Rs. 196.80 billion in 2007 to Rs. 675.84 billion in 2012. The amount of doubtful assets increased from Rs. 245.31billion in 2007 to Rs 596.20 billion in 2012. The amount of loss assets increased from Rs. 59.05 billion in 2007 to Rs. 98.92 billion in 2012 (Figures 2 and 3).

Figure 1. Deposits and advances of SCBs

Figure 2. Classification of loan assets (standard assets) of SCBs

Figure 3. Classification of loan assets of SCBs

Table 2. Classification of loan assets of SCBs (Amt in billion)

| Years | Standard Assets | Sub-standard Assets | Doubtful Assets | Loss Assets | ||||

| Amount | Per Cent | Amount | Per Cent | Amount | Per Cent | Amount | bgcolor=white>Per Cent||

| 2007 | 18433.97 | 97.4 | 196.80 | 1.0 | 245.31 | 1.3 | 59.05 | 0.3 |

| 2008 | 22759.79 | 97.6 | 261.13 | 1.1 | 242.87 | 1.0 | 52.99 | 0.2 |

| 2009 | 27210.94 | 97.6 | 359.21 | 1.3 | 267.29 | 1.0 | 55.64 | 0.2 |

| 2010 | 31825.68 | 97.5 | 412.92 | 1.3 | 326.63 | 1.0 | 78.50 | 0.2 |

| 2011 | 38973.84 | 97.6 | 398.75 | 1.0 | 448.02 | 1.1 | 94.40 | 0.2 |

| 2012 | 45284.48 | 97.1 | 675.84 | 1.4 | 596.20 | 1.3 | 98.92 | 0.2 |

Source:www.rbi.org.in

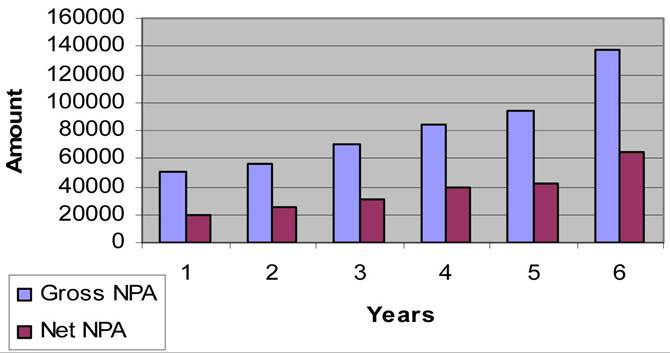

Figure 4.

Gross and net NPAs of SCBs

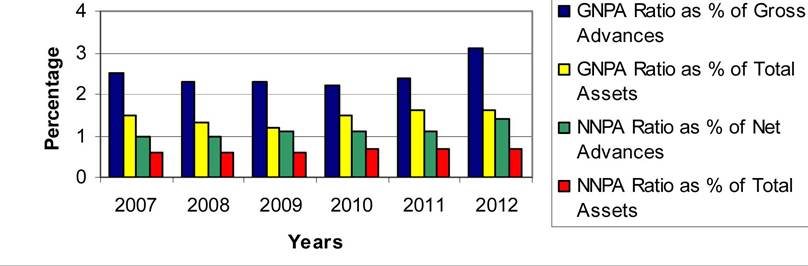

Figure 5. Percentage of GNPA and NNPA in ratio to advances and total assets

In India, non-performing assets of commercial banks gradually declined over the years, such as, Gross NPAs (GNPAs) as % to Gross Advances from 2.5% as on 31st March 2007 to 2.2% as on 31st March, 2010 but it increased in the next couple of years with 2.4% in 2011 and 3.1% in 2012. The Gross NPAs as % of Total Assets also declined from 1.5% in 2007 to 1.2% in 2009 but again increased to 1.5% in 2010 and 1.6% thereafter. The Net NPAs (NNPAs) as % of Net Advances and Net NPAs as % of Total Assets exhibited a meager fluctuation (exhibited in Table 4 along with Figures 4 and 5).

The analysis showed a declining trend in the ratio of GNPAs and NNPAs in the initial years which are a clear indication that the measures adopted by the banks are effective in controlling the menace created by NPAs. It is very important to control the problem of NPAs as there are many problems which are magnified like, Owners and Depositors do not receive a market return on their capital. In worst cases they lose their assets. Nonperforming asset may spill over the banking system and contract the money stock, which may lead to economic contraction and affect its liquidity and profitability which haened in the later years because of the increase in both the ratios.

More on the topic FACTORS CONTRIBUTING TO NPAS:

- Identifying Contributing Factors

- Identifying Contributing Factors

- Discussions of the factors contributing to violence usually focus on the role of men, ignoring women participants or portraying them as silent onlookers and victims.

- KINDS OF NPAS

- CATEGORIES OF NPAS

- Contributing Authors

- Chapter 20 Impact of NPAs on Bank Profitability: An Empirical Study

- General laws of environmental factors effect on organisms. Limiting factors. Minimum law of Liebig, tolerance law of Shelford

- Environmental factors and their classification

- SOCIAL FACTORS

- STRUCTURAL FACTORS

- HEMATOPOIETIC GROWTH FACTORS

- TECHNOLOGICAL FACTORS

- Perpetuating Factors

- Factors affecting the level of dower

- Host and Pathogen Factors in Paratuberculosis