Bubbles in Linear Rational Expectations Models

Consider a linear model in which a non-predetermined endogenous variable y depends on the rational expectation of its future value and on another exogenous variable x. The model, which is the same as the one analyzed in chapter 9 on models with rational expectations, is described by a first-order linear difference equation of the form

where Et denotes the rational expectations of a variable, conditional on the information set available in period t, and a and b are constant parameters.

The rational expectations hypothesis implies that economic agents know that the variable y is determined by (22.1). We also assume that all economic agents have access to the same information set.4Repeatedly substituting the future expectations of y, until time t + T, we get

To have convergence of the last term in (22.2) as T tends to infinity, the absolute value of a must be less than one (i.e., |a| < 1), and the expected value of x should not increase too quickly. If the expected value of x increases exponentially, its growth rate should not exceed (1/a) − 1. Under these conditions, it follows that

Then a solution of (22.1) can be derived from (22.2):

Equation (22.4) satisfies condition (22.3) and is thus a solution of (22.1). It suggests that the current value of the endogenous variable y is the discounted sum of the expected future values of the exogenous variable x, with a discount factor equal to a.

This solution is usually called the fundamental solution and is denoted by superscript f.22.1.1 Bubbles versus Fundamentals

However, note that (22.4) is not the only solution of (22.1). The fundamental solution is based only on the minimum number of variables (x in our case), the so-called fundamentals, and satisfies the convergence condition (22.3). If (22.3) is not satisfied, then a host of other, nonfundamental, solutions exists.

Suppose there is an alternative solution to (22.1) that consists of (22.4) plus an extraneous variable z. This solution takes the form

One can easily demonstrate that for any extraneous variable z that satisfies

or equivalently,

(22.5) is also a solution of (22.1). To demonstrate this, express (22.5) as

where F is the forward shift operator. Substituting (22.6) in (22.7) gives us back the original model (22.1). Hence, (22.5) is also a solution of (22.1).

However, note that because − 1 < a < 1, the mathematical expectation of the future z explodes over time. This can be proven by taking the limit of the mathematical expectation as time tends to infinity. This limit is given by

depending on whether z is positive or negative.

Hence, solutions like (22.5), based on nonfundamental variables such as z, do not satisfy the convergence condition (22.3). Such solutions are called bubbles, as opposed to solutions like (22.4), which are based only on the fundamentals.

Any variable z that satisfies (22.6) qualifies as one that can affect the solution of the model in (22.1).

Hence, (22.1) admits a multiplicity of solutions, although only the fundamental solution leads to convergence.22.1.2 Deterministic versus Stochastic Bubbles

Bubbles result in multiple equilibria and can be either deterministic or stochastic. What can be done to exclude solutions involving bubbles? The answer is to impose convergence conditions like (22.3), which ensure that yt does not explode over time. In almost all the models with perfect foresight or rational expectations that we have analyzed so far, we have ruled out bubbles: Bubbles are explosive and do not satisfy conditions like (22.3), which are required by the models to ensure that agents respect their intertemporal budget constraints.

A deterministic bubble z evolves according to the difference equation

The variable defined by (22.8) clearly satisfies (22.6) and qualifies as a bubble for the model in (22.1). The solution of the difference equation (22.8) is given by

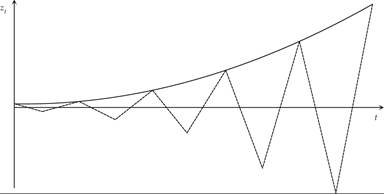

Because |a| < 1, zt explodes over time. Figure 22.1 depicts its time path, assuming both a positive a (solid line) and a negative a (dotted line). For a positive a, zt explodes monotonically; for a negative a, it explodes cyclically.

Figure 22.1 Deterministic bubbles.

In a nonfundamental solution that involves zt, like (22.5), yt also explodes over time. However, this violates the convergence condition (22.3), because

Hence, even if the fundamental solution converges, the nonfundamental solution does not.

Deterministic bubbles can be ruled out by appropriate transversality conditions that rule out explosive paths.

This is the assumption that we adopted in the deterministic growth models of chapters 4–8 to rule out bubbles and concentrate on the fundamental solution.Another type of bubble is a stochastic bursting bubble. Consider the following stochastic process:

where 0 < q < 1 is the probability that the bubble will not burst, which is constant for each period, and ε is a zero mean stochastic process that satisfies Et(εt+1) = 0. This stochastic process clearly satisfies (22.6), because

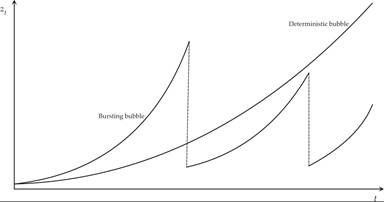

A single realization of this stochastically bursting bubble along with the deterministic bubble is presented in figure 22.2 for a positive a. In the absence of white noise disturbances, this bursting bubble has a higher slope than the deterministic bubble to compensate for the probability that the bubble will burst. This stochastically bursting bubble also does not satisfy the convergence condition (22.3) and can therefore be ruled out by appropriate transversality conditions.

Figure 22.2 A stochastically bursting bubble versus a deterministic bubble.

If we are prepared to impose a nonexplosion condition like (22.3), bubbles can be ruled out in many models. However, as we shall see below, bubbles cannot always be ruled out.

22.1.3 Bubbles as Self-Fulfilling Prophecies in Inherently Unstable Models

Bubbles may be useful in stabilizing inherently unstable models. Take, for example, the model in (22.1) for the case |a| > 1. In this case, the fundamental solution does not necessarily converge. However, an infinity of bubbles z are stable rather than exploding in this case, because 1/|a| < 1. The multiplicity of solutions is now even more perplexing, as bubbles help convergence to a steady state.

As an example, consider the model in (22.1) and assume that a > 1 and that xt follows a stationary AR(1) process of the form

where 0 < λ < 1, and Etεt+1 = 0.

The fundamental solution of the model in (22.1) when the exogenous variable xt follows (22.13) is given by

The fundamental solution converges only if aλ < 1, or equivalently, if λ < 1/a. In such a case, the fundamental solution converges to

Assume now that λ > 1/a. Then the model has to be solved backward rather than forward, as it does not satisfy the saddle point property. The fundamental solution takes the form

A host of other convergent paths exists, depending on bubbles of the type (22.6). Because a > 1, these are convergent bubbles, and they do not hinder the convergence of the endogenous variable to its steady state value given by (22.15).

Hence, in inherently unstable models that do not satisfy the saddle point property, there are multiple convergent paths depending on bubbles. Such bubbles are often called self-fulfilling prophecies and cannot be ruled out by the usual convergence arguments that we have utilized in the case of inherently stable models.5

22.1.4 Higher-Order Linear Models

The first-order linear model (22.1) is inherently stable if |a| < 1. Then the fundamental solution is characterized by the saddle point property, and provided the transversality condition (22.3) is satisfied, the economy jumps immediately to its unique fundamental solution, which is a saddle point.

This conclusion generalizes to higher-order linear models, such as the ones examined in chapter 9. In a system with n + m endogenous variables, where n is the number of predetermined (state) variables, and m the number of non-predetermined (or costate) variables, then the system must have exactly m roots outside the unit circle to have a unique nonexplosive solution.

As for the first-order linear model, bubbles can be excluded by appropriate transversality conditions that rule out explosive paths.

Inherently unstable higher-order linear models can be characterized by self-fulfilling prophecies.

22.2

More on the topic Bubbles in Linear Rational Expectations Models:

- Bubbles in Linear Rational Expectations Models

- In most of the models analyzed so far, we have concentrated on unique steady states and unique convergent paths toward the steady state.

- Conclusion

- Rational Expectations for Linear Autoregressive Processes

- Contents

- Alogoskoufis George. Dynamic Macroeconomics. The MIT Press,2019. — 800 p., 2019

- References

- Optimal Investment under Uncertainty

- Indeterminacy, Self-Fulfilling Prophecies, and Sunspots

- The Monetarist Counter-Revolution