CREDIT RATINGS

Counterparties have at certain points in time (PIT) a specific default probability. Credit rating is a credit risk factor that reflects the counterparty default probability within single or multiple time horizons.

Ratings are usually defined based on scoring systems, which use different sources of information to identify the credit profile of the counterparty, e.g., the counterparty descriptive characteristics, statistical observed data of past behavior, etc.Driven by default probabilities, credit ratings indicate the probabilities of the counterparties to honor contractual obligations under different market conditions at given time horizons. These default/non-default probabilities vary within different time horizons. Normally, such probabilities increase exponentially when the borrower has a low rating, and exposes the lender to counterparty risks for a longer time. However, it may also depend on the type of financial contract; for instance, in a loan that pays back the principal at frequent time intervals, the default probability decreases with the duration of the contract and converges to zero toward the maturity date.

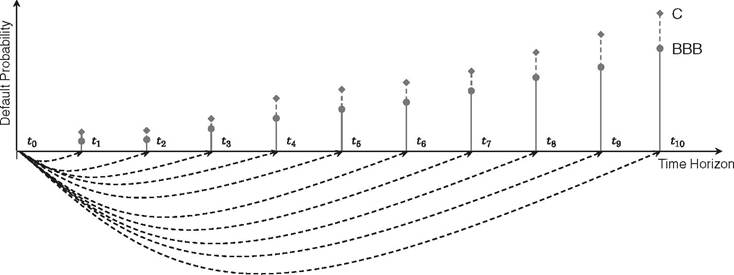

The evolution of default probability for multiple time horizons is aligned to the counterparty credit rating. An example that illustrates the discrete changes of default probabilities, for two credit ratings, within ten time horizons is shown in Figure 7.3. Moreover, the default

FIGURE 7.3 Degrees of default probabilities for two credit ratings BBB (») and C (♦) within ten time horizons

probability of each obligor can be conveniently determined by its credit rating at corresponding time horizons.

Credit ratings of counterparties have some probability of changing, i.e., downgrade or upgrade, within a time horizon. Such probabilities are defined on a matrix called migration or transition matrix discussed in Chapter 8. The definition of such matrices can be a rather complex process based on statistical observation, economic assumptions, market conditions, idiosyncratic characteristics of the counterparties, etc.

The link between the counterparty ratings is based on their sensitivities to certain market risk factors, as well as the correlations among them using common and correlated sector analysis. This will be covered later in the section discussing the link of counterparties via markets. Finally, credit ratings in the view the risk-neutral default probabilities are associated with the counterparty credit spreads used in the valuation of the investments that contain the credit portfolio.

7.5

More on the topic CREDIT RATINGS:

- Article 3.11 Local authorities turn to capital markets

- INDEX

- Commercial paper

- References

- COUNTERPARTY SYSTEMIC RISK

- Article 15.7 Rebound in sales of risky assets raises fears over quantitative easing's legacy

- Article 15.1 Sunshine-backed bond to go on sale

- Article 6.8 Great Portland strikes with convertible bond

- LITERATURE REVIEW AND HYPOTHESES DEVELOPMENT

- The Mechanics of Monetary Policy