Chapter 51 The Role of Relational Mediators in the CRM- Performance Link: Evidence from Indian Retail Banks

Chandrasekaran Padmavathy Vellore Institute of Technology, India

ABSTRACT

CRM literature has considered the role of relationship quality (satisfaction, trust and commitment), but its respective effects on relationship maintenance (retention) and relationship development (cross-buying) are unnoticed.

This research proposes an integrated model of CRM and investigates its impact on relationship quality, relationship maintenance, and relationship development. Specifically, it examines the effect of CRM on satisfaction, trust, retention and cross-buying. The results indicate significant and positive effect of CRM on satisfaction; satisfaction has a positive effect on trust, retention and cross-buying, and trust positively influences retention. Satisfaction plays a mediating role in the relationship between CRM and its outcomes. The results imply bank managers to focus on satisfying customers primarily to maintain and develop customer relationships.INTRODUCTION

Marketing has witnessed a paradigm shift towards relationship approach a decade ago (Gronroos, 1994). Hence, the concept of customer relationship management (CRM) is a constant theme in marketing. Today, many firms adopt CRM strategies with the aim of understanding customers better and building better relationships (Fitzgibbon and White, 2004). It provides number of benefits including increased customer satisfaction, trust, loyalty, sales effectiveness, cross selling opportunities, and profitability. Concisely, CRM efforts increase length, depth and breadth of a relationship (Bolton, Lemon, & Verhoef, 2004).

CRM is applicable more in banking industry as it is known to be highly human intensive and customer interactive industry (Dowling, 2002) and banks represent the economic stability and prosperity of a country (Rootman, Tait, & Bosch, 2008). But, global banking environment has been changed due to regulatory, structural and technological factors (Rao, 2008).

Consequently, without exception, Indian banking sector has also been transformed to a greater extent following deregulation, liberalization and globalization of the economy. These challenges together with increasing demanding customers compel banks to maintain customer relationship for improving business performance. Accordingly, most of the Indian banks are investing heavily in CRM technology (Khare, 2010) with a view to maintain and develop relationship with customers (Roy & Shekhar, 2010). On the contrary, the importance of developing such relationships and the outcomes of the relationships are largely ignored by Indian banks (Khare, 2010).DOI: 10.4018/978-1-4666-6268-1.ch051

.

Theoretically, numerous empirical studies have reported positive effect of CRM on customer behavioral outcomes such as customer satisfaction (Mithas, Krishnan, & Fornell, 2005), customer trust (Sin, Tse, & Yim, 2005), and customer retention (Yim, Anderson, & Swaminathan, 2004); and financial performance outcomes such as return on assets (ROA) (Sin, Tse, & Yim, 2005), profitability (Reimann, Schilke, & Thomas, 2010), and return on equity (ROE) (Minami & Dawson, 2008). However, firstly, previous research has tested only partial impact of CRM either on satisfaction or retention and failed to address sequential effect of CRM, which is expected from customer satisfaction to firm financial benefit (Minami & Dawson, 2008). Secondly, CRM model tends to combine the effect of CRM on both customer metrics and financial metrics, and often used financial measures such as ROA and profitability to measure financial performance. But, it is argued that customer metrics like cross-buying or cross sell ratio is an important outcome of CRM efforts (Bohling et al., 2006) and it contributes to firm profits (Blattberg, Getz, & Thomas, 2001; Liang, Wang, & Farquhar, 2009). Thirdly, Aurier and N’Goala (2010) articulate that CRM theory has considered the role of relationship quality perceptions (satisfaction, trust and commitment), but ignored to examine their respective effects on relationship maintenance (customer retention) and relationship development (cross-buying).

Moreover, in relationship efforts model, it is stated that the roles of relational mediators (satisfaction, trust and commitment) vary according to different relational perspectives (Palmatier, 2006). Fourthly, it is believed that perception of relationship and behavior is context specific (Dimitriadis, 2010; Palmatier et al., 2006) and therefore CRM performance has to be studied in Indian context (Jham & Khan, 2008). And finally, studies on CRM have considered firm perception, leaving open the issue of how customers perceive CRM efforts (Chan, 2005; Sin, Tse, & Yim, 2005). To the best of our knowledge, till date, none of the empirical studies on CRM have examined its impact on relationship quality, relationship maintenance and relationship development.These gaps necessitate a rationale for developing and testing a more integrative conceptual framework containing the relationship between CRM, relationship quality; maintenance; and development in Indian retail bank setting from customer perception. The framework allows us to simultaneously investigate the respective impacts of relational mediators on both relationship maintenance and development. Specifically, we examine the impact of CRM on customer satisfaction, customer trust, customer retention and customer cross-buying. We believe that our study findings would shed light and add substantive theory to the body of knowledge on CRM. To realize this, we first review previous research on CRM followed by the proposed model and hypothesis construction. Second, we present the research methodology, including the instruments used for hypothesis testing. Finally, the empirical results are examined, key managerial and research implications are provided.

LITERATURE REVIEW

Concept of CRM

CRM is an integral part of relationship marketing (RM) and many of the scholars use the term RM and CRM interchangeably (Parvatiyar & Sheth, 2001). But RM becomes CRM when it is targeted towards customer market especially (Lindgreen & Antioco, 2005).

CRM means different thing to different people, for sales community, it means sales-force automation; for marketing people, it signifies customer selection, and for information technology group, it may suggest database management (Sharma & Iyer, 2007). Nonetheless, the basic premise of CRM is to maintain a mutually beneficial relationship (Soper, 2002).CRM research can be divided into two streams. One is process approach and the other is relationship approach (Lin, Chen, & Chiu, 2010). Process approach contains initiating, maintaining and terminating relationship with customers (Reinartz, Krafft, & Hoyer, 2004). Relationship approach refers to activities such as understanding customers, giving privilege to key customers and delivering superior services from the use of available information technology (Sin, Tse, & Yim, 2005). Our study follows the tradition of relationship approach.

CRM and its Outcomes

Empirical studies report positive influence of CRM on its performance measures under various perspectives. For instance, in process related perspective, Reinartz, Krafft, and Hoyer (2004) conceptualize CRM as a process that contains three different stages including relationship initiation; maintenance; and termination. It is found that initiating the relationship and maintaining it improve firm’s economic performance. In this context, Becker et al. (2009) report that technological and organizational implementation positively influences CRM performance at each of the three stages. Reimann, Schilke, and Thomas (2010) conclude that three stage CRM process has an indirect impact on customer satisfaction and profitability through differentiation and cost leadership. In a process oriented framework of CRM effectiveness, Chen et al. (2009) discover that elements of CRM effectiveness like RM, information technology and organizational climate increase customer loyalty.

In relational activities perspective, the study by Yim, Anderson, and Swaminathan (2004) reveal that CRM dimensions such as focusing on customers and managing knowledge influence customer satisfaction; and managing knowledge and organizing around CRM increase customer retention levels.

The results also support that CRM dimensions have an indirect relationship to sales growth through satisfaction and retention. On the similar note, Sin, Tse, and Yim (2005) find that CRM positively influences customer satisfaction, customer trust, return on investment and ROA. Jayachandran et al. (2005) report that relational information process increases customer relationship performance. Minami and Dawson (2008) identify that integration of customer data and loyalty scheme with the use of IT (relationship orientation) increase CRM implementation, which is found to have an indirect impact on ROE.In the perspective of technology, CRM system implementation containing BPR and organizational learning increase the level of relationship quality (satisfaction, trust and commitment) and organizational performance (Chang and Ku, 2009). In B-to-B context, Richard, Thirkell, and Huff (2007) find that CRM technology adoption increases relationship strength (trust and commitment) and relationship performance (satisfaction, retention and loyalty). CRM system investment and CRM capability is positively significant to customer satisfaction in a retail context (Srinivasan and Moorman, 2005). CRM contains legacy and new application that increases customer satisfaction levels (Mithas, Krishnan, & Fornell, 2005).

In sum, review of CRM and its outcomes reveal that the majority of the studies have concentrated on customer satisfaction, customer trust and customer retention, leaving other expected outcomes of CRM. Moreover, studies with two or more outcome variables combine both financial as well as non-financial measures.

CRM in Financial Services Context

Effective implementation of CRM reduces cost, complexity and waiting time; increase performance and service levels; and increase bank customer relationships (Blery & Michalako- poulos, 2006). It also helps in increasing firms’ profit efficiency but unhelpful in improving cost efficiency (Krasnikov, Jayachandran, & Kumar, 2009).

Use of CRM software improves productivity and performance quality (McNally, 2007) and the adoption of right technology will result in enhanced customer management of relationships (Ellis-Chadwick, McHardy, & Wiesehofer, 2002).CRM enablers are found to affect CRM success. For example, firms engaged in effective project management, realistic time scheduling and perfect programming will reap the benefits of CRM success such as customer satisfaction and retention (Blery & Michalakopoulos, 2006). Similarly, critical enablers such as realistic CRM implementation schedule, personalization, customer orientation and clear CRM strategy contribute to increased customer retention (Eid, 2007).

Bank employees’ knowledgeability and attitude are the crucial factors in improving effectiveness of CRM strategy (Rootman, Tait, & Bosch, 2008) when combined with IT infrastructure, and business architecture (Coltman, 2007). Affective commitment and loyalty programs enhance customer retention and customer share development (Verhoef, 2003). Furthermore, assertiveness and affiliation of the service provider increase customer retention and share of wallet.

Adoption of mobile banking as a CRM tool assists banks in acquiring and retaining customers (Riivari, 2005). Existence of online banking, virtual banking and non-banking may make the bank to lose customers and yet it is useful to identify high net worth customers from the usage of e-banking (Sciglimpaglia & Ely, 2006). In Indian financial services context, recently, Khare (2010) explores that Indian customers are skeptical to use online banking. Support of bank employees in educating the importance and value of online banking will change customer perception and improve CRM strategy.

In conclusion, CRM in financial services context reveal that it is devoid of a complete conceptual model reflecting the impact of CRM on possible non-financial outcomes. So, we try to examine the influence of CRM on its expected customer outcome variables.

CONCEPTUAL MODEL AND RESEARCH HYPOTHESIS

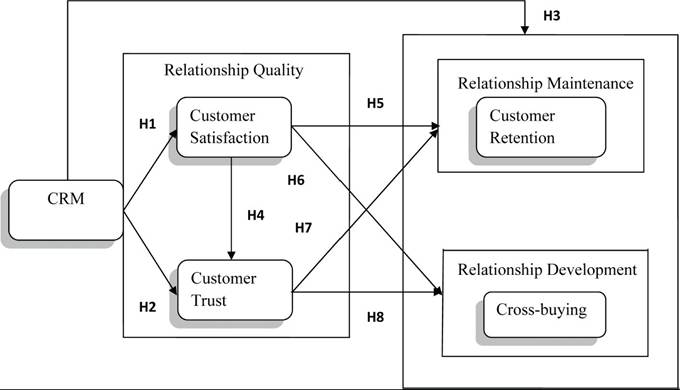

Figure 1 represents our extended and advanced CRM model. The causal model depicts the relationships between CRM and relationship quality, relationship maintenance and relationship development. We now discuss the theoretical underpinnings for our hypothesis.

Relationship Quality

Relationship quality (RQ) has been used frequently in buyer-seller relationship literature (Athanaso- poulou, 2008) and it is considered as relationship strength (Garbarino & Johnson, 1999). Earlier, it has been conceptualized mainly of trust and satisfaction (Crosby et al., 1990). Later, commitment has been added as one more indicator of RQ (Beatson, Lings, & Gudergan, 2008). We assume RQ as satisfaction and trust of customers with the bank since they are widely used in financial services context (Bejou, Wray, & Ingram, 1996; Wray, Palmer, & Bejou, 1994).

Figure 1. Conceptual model

Relationship Maintenance

Banks try to maintain and expand relationship for achieving long-term profitability of a customer (J arrar & Neely, 2002). Aurier and N’Goala (2010) conceptualize customer retention as one of the patronage behaviors in relationship maintenance phase. McNally (2007) considers customer retention as one of the maintenance phase activities. In line with above studies, we consider customer retention as an indicator of relationship maintenance.

Relationship Development

Retaining existing customers is not sufficient for developing relationship and enhancing profitability. Making retained customers to buy additional products (cross-buying) helps in relationship development and it will generate financial benefit to the firm (Bolton, Lemon, & Verhoef, 2004). Crossbuying is considered as relationship development or extension (Verhoef & Donkers, 2005). Ngobo (2004) conceptualizes it as expansion of the relationship and Bolton, Lemon, and Verhoef (2004) consider it as breadth of the relationship. Similar to Verhoef and Donkers (2005), we conceptualize cross-buying as relationship development.

Effect of CRM on Customer Satisfaction

Customer satisfaction has been considered as an important goal of CRM activity (Yim, Anderson, and Swaminathan, 2004) and it is a focal outcome in buyer-seller relationship (Smith & Barclay, 1997). In banking context, relationship efforts made by a retailer would have an effect on customer satisfaction (Liang & Wang, 2007) and several studies have reported positive impact of CRM on customer satisfaction (e.g., Mithas, Krishnan, & Fornell, 2005; Sin, Tse, & Yim, 2005; Srinivasan & Moorman, 2005). Therefore, we hypothesize:

H1: There is a positive relationship between CRM and customer satisfaction.

Effect of CRM on Customer Trust

Trust plays a major role in the success and benefit of developing customer relationships (Hulten, 2007; Morgan & Hunt, 1994) and it is the single most powerful RM tool available to the service providers (Berry, 1995). Furthermore, empirical studies on CRM find positive association between CRM and customer trust (e.g. Richard, Thirkell, & Huff, 2007; Sin, Tse, & Yim, 2005). Therefore, we hypothesize:

H2: There is a positive relationship between CRM and customer trust.

Effect of CRM on

Customer Retention

Every relationship management activities are focused at increasing customer retention. Menon and O’ Connor (2007) argue that CRM efforts such as assertiveness and affiliation will generate retention of customers. Empirical studies in the context of banking have also reported positive relationship between CRM and retention. For instance, Yim, Anderson, and Swaminathan (2004) find positive effect of CRM dimensions on retention. Eid (2007) find positive impact of CRM effectiveness on customer retention. Based on these arguments and findings, we hypothesize:

H3: There is a positive relationship between CRM and customer retention.

Effect of Customer Satisfaction on Trust, Retention and Cross-Buying

Satisfied customers tend to develop their affiliation with the service provider and their association in the service relationship (Bolton, 1998). In a banking context, overall satisfaction arrived from service quality influences trust (Aurier & N’Goala, 2010). In the study of Liang and Wang (2007), it is found that satisfaction arrives out of relationship benefits have positive effect on customer trust.

In satisfaction literature, it has been explored that a key determinant to customers’ decisions to continue or terminate a business relationship arrives from satisfaction (e.g., Bolton, 1998). Greater customer satisfaction is generally believed to increase customer retention levels (Yim, Anderson, & Swaminathan, 2004). Number of empirical studies finds positive influence of satisfaction on retention (e.g. Hennig-Thurau, 2004; Mohd Kas- sim & Souiden, 2007).

When customers are satisfied in the initial stages, they build necessary trust and expand their relationship through cross-buying behavior (Bendapudi & Berry, 1997; Reinartz, Thomas, & Bascoul, 2008). In a recent study, Dimitriadis (2010) finds that satisfaction with a bank influences cross-buying. Some studies have reported direct or indirect relationship between satisfaction and cross-buying (Bloemer et al., 2002; Ngobo, 2004). On the other hand, insignificant relationship between satisfaction and cross-buying is also reported (Liu & Wu, 2007; Soureli et al., 2008). However, based on the argument that satisfied customers tend to buy additional products (Liu & Wu, 2007), we expect the relationship between customer satisfaction and cross-buying to be positive. Therefore, we hypothesize the following:

H4: Customer satisfaction will have a positive influence on customer trust.

H5: Customer satisfaction will have a positive influence on customer retention.

H6: Customer satisfaction will have a positive influence on cross-buying.

Effect of Trust on Retention and Cross-Buying

Trust is generally considered as a fundamental requirement for successful relationship maintenance and enhancement (Gronroos, 1999). Several studies in RM consider trust as a determinant of customer retention (Doney & Cannon, 1997; Johnson & Grayson, 2005). The positive effect of trust on customer retention has been examined in literature (e.g. Liu & Wu, 2007).

Many studies have reported that trust influences cross-buying intention (Crosby et al., 1990; Liang, Chen, & Wang, 2008; Liu & Wu, 2007; Soureli et al., 2007). Whereas Verhoef, Franses, and Hoekstra (2002) report insignificant relationship between trust and cross-buying and argued that trust is important for clients only in choosing a new service provider. Nevertheless, trust is regarded as a scope for extending relationship (Selnes, 1998). Therefore, we hypothesize the following:

H7: Customer trust will have a positive influence on customer retention.

H8: Customer trust will have a positive influence on cross-buying.

and Cadogan (2000). All the statements were measured on a five-point Likert scale ranging from 1 ‘strongly disagree to 5 ‘strongly agree’.

Pretest

Items and definitions were given to three marketing professors and two bank managers to assess item wordings and applicability of measures to suit the banking context. Word changes were carried

METHODOLOGY

Sample and Data Collection Procedure

To empirically test the model proposed in Figure 1, we collected survey data on CRM, customer satisfaction, customer trust, customer retention and cross-buying. The study sample consisted of retail bank customers. A self-completion web questionnaire was mailed to a convenience sample of 1100 respondents. Due to lack of population information or sample frame, convenience sampling was used to improve the precision of the estimates as suggested by Cooper and Schindler (1998). Web survey resulted in usable 426 responses, yielding a response rate of 38.7 per cent. Table 1 describes the demographic profile of the respondents.

Measurements

Measurements for all constructs were taken from existing literature. To measure CRM, 9 items were adopted from Sin, Tse, and Yim (2005). 3 items were adapted from Singh (1990) and Verhoef, Franses, and Hoekstra (2001) to measure customer satisfaction. Based on Crosby et al. (1990) and Morgan and Hunt (1994), we adopted 3 items for measuring customer trust. 3 customer retention items were based on Zeithaml, Berry, and Parasuraman (1996) and finally for measuring cross-buying, 2 items were adopted from Foster

Table 1. Demographic profile

| Demographic Information n = 426 | N | % | |

| Gender | Male | 286 | 67.1 |

| Female | 140 | 32.9 | |

| Age | Less than 20 years | 3 | 0.70 |

| 21-30 years | 322 | 75.6 | |

| 31-40 years | 57 | 13.4 | |

| 41-50 years | 26 | 6.1 | |

| More than 50 years | 18 | 4.2 | |

| Education | Undergraduate | 83 | 19.5 |

| Post-graduate | 264 | 62 | |

| Professional Degree | 64 | 15 | |

| Others | 15 | 3.5 | |

| Employment | Private sector | 202 | 47.4 |

| 54 | 12.7 | ||

| Self-employed | 30 | 7 | |

| Student | 92 | 21.6 | |

| Others | 48 | 11.3 | |

| Primary Bank | SBI | 103 | 24.2 |

| HDFC | 82 | 19.2 | |

| ICICI | 64 | 15 | |

| Punjab National Bank | 25 | 5.9 | |

| Karur Vysya Bank | 18 | 4.2 | |

| Others | 134 | 31.5 | |

| Duration with primary Bank | Less than 1 year | 48 | 11.3 |

| Between 1-4 years | 218 | 51.2 | |

| Between 4-7 years | 98 | 23 | |

| Between 7-10 years | 33 | 7.7 | |

| More than 10 years | 29 | 6.8 | |

out based on the comments received. Instrument containing all 20 items were pretested by 210 MBA students. 3 items from the initial battery of 9 items of CRM were deleted based on item-to- total correlation criterion (< 0.4), factor loading of less than 0.4, cross-loading of less than 0.4 (Hair et al., 1998) and Cronbach’s alpha less than 0.7. EFA using principal component extraction and varimax rotation performed on the remaining 6 items of CRM resulted in one single factor.

ANALYSIS AND RESULTS

Measurement Model

In order to test the validity of measures used in the study, we conducted confirmatory factor analysis using AMOS 16.0 and by employing maximum likelihood method. The model fit the data well with a (chi-square value (103) = 260.08, p = 0.000, GFI = 0.94, AGFI = 0.91, CFI = 0.96, TLI = 0.94 and RMR = 0.027). Measurement reliability was confirmed by assessing Cronbach’s alpha values. All the alphas exceeded the threshold limit of.70 (Table 2). All the items were loaded on their respective factors, thus validating the unidimensionality of the constructs (Anderson & Gerbing, 1988). The t-values for the loadings were high, demonstrating adequate convergent validity. All measures of composite reliability and all average variance-extracted (AVE) estimate were exceeded the threshold limit of 0.6 and 0.5 respectively (Hair et al., 1998; Fornell & Larcker, 1981) (Table 2). Moreover, AVE for each dimension was higher than the squared correlation among the five factors, confirming discriminant validity (Fornell & Larcker, 1981) (Table 3).

Structural Model and Hypothesis Results

Given a valid and reliable scale to measure, we tested the overall model. The model fit the data well with a (chi-square value (106) = 315.85, p = 0.000, GFI = 0.93, AGFI = 0.90, CFI = 0.94, TLI = 0.92 and RMR = 0.03).

Structural model evaluation shows that as hypothesized, CRM was found to positively affect customer satisfaction (p= 0.000, t-value = 10.98), thus supporting H1. As predicted, satisfaction positively influences customer trust (p= 0.000, t-value = 6.77), customer retention (p= 0.003, t- value = 4.52) and cross-buying (p= 0.000, t-value = 8.53), supporting H4, H5 and H6. In case of customer trust, it did influence customer retention (p= 0.002, t-value = 3.05), supporting H7.

However, we find no direct relationship between CRM and customer trust (p= 0. 585, t-value = -0.55), customer retention (p= 0.679, t-value = -0.414). Therefore, H2 and H3 are rejected. Trust did not have relationship with cross-buying (p= 0.584, t-value = 0.548), rejecting H8. Moreover, the indirect effect of CRM on trust was 0.539 (0.77 * 0.70). CRM also had an indirect effect on retention through satisfaction and trust (0.42 * 0.12 = 0.54).

DISCUSSION

Although previous research has extensively studied relationships between CRM and customer satisfaction, customer trust and customer retention, they were incomplete by considering partial impact of CRM on its performance outcomes. Moreover, only few studies have addressed the impact of CRM purely on customer outcome variables and provided empirical evidence. The primary contribution of this study is in the development of an extended conceptual model for CRM with its expected customer outcomes. The model included five variables such as CRM, customer satisfaction, customer trust, customer retention and cross-buying. As one step further, besides replicating CRM model in Indian context, we expanded the model by considering all the possible non-financial indicators. Empirical

Table 2. Measurement model

| Item | Standardized Loadings | t-Value | Cronbach’s Alpha | AVE | CR |

| CRM | 0.87 | 0.64 | 0.70 | ||

| My bank employees are committed in providing prompt service to me | 0.88 | ||||

| My bank carefully evaluates my evolving needs | 0.86 | 11.353 | |||

| My bank offers customized products/services to me | 0.80 | 11.304 | |||

| My bank employees are willing to help me in a responsive manner | 0.78 | 12.889 | |||

| My bank employees effectively communicate with me | 0.76 | 12.180 | |||

| My bank makes effective use of information technology for fast and quality service. | 0.75 | 12.442 | |||

| Customer Satisfaction | 0.83 | 0.70 | 0.73 | ||

| I am satisfied with my relationship with the bank | 0.86 | ||||

| I am satisfied with the willingness of my bank to explain procedures | 0.88 | 17.734 | |||

| I am satisfied with the personal attention of my bank towards me | 0.76 | 15.485 | |||

| Customer Trust | 0.81 | 0.67 | 0.72 | ||

| My bank has high integrity. | 0.76 | bgcolor=white> | |||

| My bank is trustworthy. | 0.85 | 14.982 | |||

| My bank puts my interest first. | 0.85 | 15.062 | |||

| Customer Retention | 0.73 | 0.65 | 0.70 | ||

| I say positive things about my bank | 0.78 | ||||

| I encourage friends and relatives to invest with my bank | 0.84 | 11.976 | |||

| I consider my bank as my first choice when comes to banking products | 0.80 | 10.896 | |||

| Cross-buying | 0.73 | 0.75 | 0.78 | ||

| I have intention to increase the volume of business with my bank | 0.89 | ||||

| I have intention to buy more products from my bank | 0.84 | 13.174 |

Table 3. Discriminant validity and descriptive statistics

| Constructs | CRM | Customer Satisfaction | Customer Trust | Customer Retention | Cross-buying |

| CRM | 0.64 | 0.35 | 0.16 | 0.16 | 0.23 |

| Customer Satisfaction | .59[‡] | 0.70 | 0.29 | 0.23 | 0.30 |

| Customer Trust | .40* | 0.54* | 0.67 | 0.20 | 0.15 |

| Customer Retention | .40* | 0.48* | 0.45* | 0.65 | 0.29 |

| Cross-buying | .48* | 0.55* | 0.39* | 0.54* | 0.75 |

| Mean | 21.75 | 11.58 | 11.78 | 10.58 | 7.15 |

| SD | 3.76 | 1.93 | 1.88 | 2.18 | 1.46 |

evidence examining CRM effect on relationship development (cross-buying) has been very modest, but cross-buying behavior is specifically indispensable to banks where establishing, maintaining and developing relationship is important (Sin, Tse, & Yim, 2005). Therefore, to the best of our knowledge, this is the first empirical study to investigate relational mediators sequentially in the CRM-performance link as well as to examine CRM from the perception of customers in Indian retail bank setting.

Empirical results of this study show that CRM positively influences customer satisfaction and this is consistent with previous research (Sin, Tse, & Yim, 2005; Yim, Anderson, & Swaminathan, 2004). The negative and insignificant effect of CRM on trust and retention is offset by its indirect effect through customer satisfaction and this indicates that satisfaction mediates the relationship between CRM and its outcomes. This finding support the views of Morgan and Hunt, 1994 that impact of RM strategies on outcomes are fully mediated by one or more of the relational constructs such as satisfaction, trust and commitment. Moreover, Chan (2005) and Chen and Popovich (2003) suggest that the mere use of CRM does not automatically lead to customer retention. Aurier and N’Goala (2010) and Bolton (1998) suggest that satisfaction is a basic and necessary condition in developing affiliation and reinforcing trust with the service provider.

This study also provides support for the link between satisfaction, trust, retention and crossbuying. Satisfaction positively predicts trust and it is in line with prior studies (Aurier & Gilles N’Goala, 2010; Liang & Wang, 2007). Satisfaction and trust have direct positive association with retention, exhibiting similar results of Liu and Wu (2007). Influence of satisfaction on crossbuying is supported by Bloemer et al. (2002) and Ngobo (2004). Somewhat surprisingly, we found insignificant impact of trust on cross-buying. This is in contrast with the results of Liu and Wu

(2007). Yet, this can be explained by the fact that relationship between trust and cross-buying varies to different contexts of the studies (Verhoef, Franses, & Hoekstra, 2002).

MANAGERIAL IMPLICATIONS

Results of the study show that CRM aids in the improvement and development of relationship through customer satisfaction. This hints the bank marketers that the fore most goal of CRM is to satisfy the customer, which in turn, provides financial benefit to them. Our results indicate that managers who focus on building, maintaining and developing relationship with customers should note that delivery of prompt services; effective communication; customized products/services; and efficient use of information technology are the most vital CRM strategies. Precisely, bank marketers can concentrate on the orchestration of people, process and technology in implementing CRM activities (Chen & Popovich, 2003; Sin, Tse, & Yim, 2005). By focusing on higher levels of customer satisfaction, managers can develop trust with customer, retain existing customers, convince customers for repeat business and thereby, cutting cost by keeping current customers than acquiring a new.

This study also provides evidence for the impact of satisfaction and trust on retention. Notably, satisfaction dominantly increases retention levels, while trust is the secondary one. This means that satisfaction should be the primary aim of the service provider, since customer develops trust only for the first time they involve in the relationship (Verhoef, Franses, & Hoekstra, 2002). In the later stages of relationship, satisfaction plays an important role in developing relationship as satisfied customers will evaluate the risk associated with the service provider and decide to maintain or develop relationship (Aurier & N’ Goala, 2010). Our study results have shown that satisfaction also affects cross-buying behavior. This implies that for persuading existing customers to buy additional products, satisfying customers should be the mantra for bank mangers. Altogether, managers can achieve customer profitability through retention and cross-buying (Liang, Chen, & Wang, 2008). In conclusion, the study proved the long held belief that CRM increases business performance. And customer satisfaction appears as a pivotal concept and remains as an important basis for building trust; maintaining and developing customer relationship.

Limitations and future

RESEARCH DIRECTIONS

Our study has included only 6 items for measuring customer perception towards CRM activities. Future research can develop a standardized scale for measuring CRM in Indian retail banking context and investigate it impacts on both objective and subjective outcomes. The chosen set of factors in our framework is not exhaustive nor a list of the most important factors. For example, customer loyalty and customer commitment could also be added in the CRM-performance link. Convenience sampling warrant caution before generalizing the results beyond the population studied. This study is limited to banking context and warrant caution before generalizing to other industries and nations. The study is cross sectional and future research can consider longitudinal observations.

REFERENCES

Athanasopoulou, P. (2008). Antecedents and consequences of relationship quality in athletic services. Managing Service Quality, 18(5), 479-495. doi:10.1108/09604520810898848

Aurier, P., & N’Goala, G. (2010). The differing and mediating roles of trust and relationship commitment in service relationship maintenance and development. Journal of the Academy of Marketing Science, 38(3), 303-325. doi:10.1007/ s11747-009-0163-z

Beatson, A. T., Lings, I., & Gudergan, S. (2008). Employee behaviour and relationship quality: Impact on customers. The Service Industries Journal, 28(2),211-223. doi:10.1080/02642060701842282

Bejou, D., Wray, B., & Ingram, T. N. (1996). Determinants of relationship quality: An artificial neural network analysis. Journal of Business Research, 36(2), 137-143. doi:10.1016/0148- 2963(95)00100-X

Bendapudi, N., & Berry, L. L. (1997). Customers motivations for maintaining relationships with service providers. Journal of Retailing, 73(1), 15-37. doi:10.1016/S0022-4359(97)90013-0

Berry, L. L. (1995). Relationship marketing of services-growing interest, emerging perspectives. Journal oftheAcademy ofMarketing Science, 23(4), 236-245. doi:10.1177/009207039502300402

Blattberg, R. C., Getz, G., & Thomas, J. S. (2001). Customer equity: Building and managing relationships as valuable assets. Boston, MA: Harvard Business School Press.

Blery, E., & Michalakopoulos, M. (2006). Customer relationship management: A case study of a Greek bank. Journal of Financial Services Marketing, 11(2), 116-124. doi:10.1057/palgrave. fsm.4760014

Bloemer, J., Brijs, T., Swinnen, G., & Vanhoof, K. (2002). Identifying latently dissatisfied customers and measures for dissatisfaction management. International Journal of Bank Marketing, 20(1), 27-37. doi:10.1108/02652320210415962

Bohling, T., Bowman, D., LaValle, S., Mittal,

V., Narayandas, D., Ramani, G., & Varadara- jan, R. (2006). CRM Implementation. Journal of Service Research, 9(2), 184-194. doi:10.1177/1094670506293573

Bolton, R. N. (1998). A dynamic model of the duration of the customers relationship with a continuous service provider: The role of satisfaction. Marketing Science, 17(1), 45-65. doi:10.1287/ mksc.17.1.45

Bolton, R. N., Lemon, K. N., & Verhoef, P.

C. (2004). The theoretical underpinnings of customer asset management: a framework and propositions for future research. Journal of the Academy of Marketing Science, 32(3), 271-292. doi:10.1177/0092070304263341

Chan, J. O. (2005). Toward a unified view of customer relationship management. Journal of American Academy of Business, 6(1), 32-38.

Chang, H. H., & Ku, P. W. (2009). Implementation of relationship quality for CRM performance: Acquisition of BPR and organisational learning. Total Quality Management and Business Excellence, 20(3), 327-348. doi:10.1080/14783360902719758

Chen, I. J., & Popovich, K. (2003). Understanding customer relationship management (CRM): People, process and technology. Business Process Management Journal, 9(5), 672-688. doi:10.1108/14637150310496758

Chen, J. S., Yen, H. J. R., Li, E. Y., & Ching, R.

K. H. (2009). Measuring CRM effectiveness: Construct development, validation and application of a process-oriented model. Total Quality Management and Business Excellence, 20(3), 283-299. doi:10.1080/14783360902719451

Coltman, T. (2007). Can superior CRM capabilities improve performance in banking. Journal of Financial Services Marketing, 12(2), 102-114. doi:10.1057/palgrave.fsm.4760065

Cooper, D. R., & Schindler, P. S. (2003). Business research methods. New York, NY: McGraw-Hill.

Crosby, L. A., Evans, K. R., & Cowles, D. (1990). Relationship quality in services selling: An interpersonal influence perspective. Journal of Marketing, 54(3), 68-81. doi:10.2307/1251817

Dimitriadis, S. (2010). Testing perceived relational benefits as satisfaction and behavioural outcomes drivers. International Journal of Bank Marketing, 28(4), 297-13. doi:10.1108/02652321011054981

Doney, P. M., & Cannon, J. P. (1997). An examination of the nature of trust in buyer-seller relationships. Journal of Marketing, 61(2), 35-51. doi:10.2307/1251829

Dowling, G. (2002). Customer relationship management: In B2C markets, often less is more. California Management Review, 44(3), 87-104. doi:10.2307/41166134

Eid, R. (2007). Towards a successful CRM implementation in banks: An integrated model. The Service Industries Journal, 27(8), 1021-1039. doi:10.1080/02642060701673703

Ellis-Chadwick, F., McHardy, P., & Wiesehofer, H. (2002). Online customer relationships in the European financial services sector: A cross-country investigation. Journal of Financial Services Marketing, 6(4), 333-345. doi:10.1057/palgrave. fsm.4770063

Fitzgibbon, C., & White, L. (2005). The role of attitudinal loyalty in the development of customer relationship management strategy within service firms. Journal of Financial Services Marketing, 9(3), 214-230. doi:10.1057/palgrave. fsm.4770155

Fornell, C., & Larcker, D. F. (1981). Evaluating structural equation models with unobservable variables and measurement error. JMR, Journal of Marketing Research, 18(1), 39-50. doi:10.2307/3151312

Foster, B. D., & Cadogan, J. W. (2000). Relationship selling and customer loyalty: An empirical investigation. Marketing Intelligence & Planning, 18(4), 185-199.doi:10.1108/02634500010333316

Garbarino, E., & Johnson, M. (1999). The different roles of satisfaction, trust and commitment for relational and transactional consumers. Journal of Marketing, 63(2), 70-87. doi:10.2307/1251946

Gronroos, C. (1994). From marketing mix to relationship marketing: towards a paradigm shift in marketing. Management Decision, 32(2), 4-20. doi:10.1108/00251749410054774

Gronroos, C. (1999). Relationship marketing: Challenges for the organization. Journal of Business Research, 46(3), 327-335. doi:10.1016/ S0148-2963(98)00030-7

Hair, J. F., Black, W. C., Babin, B. J., Anderson, R. E., & Tatham, R. L. (1998). Multivariate data analysis. Upper Saddle River, NJ: Prentice Hall.

Hennig-Thurau, T. (2004). Customer orientation of service employees: Its impact on customer satisfaction, commitment, and retention. International Journal of Service Industry Management, 15(5), 460-478. doi:10.1108/09564230410564939

Hulten, B. (2007). Customer segmentation: The concepts of trust, commitment and relationships. Journal of Targeting. Measurement and Analysis for Marketing, 15(4), 256-269. doi:10.1057/ palgrave.jt.5750051

Jarrar, Y. F., & Neely, A. (2002). Cross-selling in the financial sector: Customer profitability is key. Journal of Targeting. Measurement and Analysis for Marketing, 10(3), 282-296. doi:10.1057/ palgrave.jt.5740053

Jayachandran, S., Sharma, S., Kaufman, P., & Raman, P. (2005). The role of relational information processes and technology use in customer relationship management. Journal of Marketing, 69(4), 177-192. doi:10.1509/jmkg.2005.69.4.177 Jham, V., & Khan, K.bM. (2008). Determinants of performance in retail banking: Perspectives of customer satisfaction and relationship marketing. Singapore Management Review, 30(2), 35-45.

Johnson, D., & Grayson, K. (2005). Cognitive and affective trust in service relationships. Journal of Business Research, 58(4), 500-507. doi:10.1016/ S0148-2963(03)00140-1

Khare, A. (2010). Online banking in India: An approach to establish CRM. Journal of Financial Services Marketing, 15(2), 176-188. doi :10.1057/ fsm.2010.13

Krasnikov, A., Jayachandran, S., & Kumar, V. (2009). The impact of customer relationship management implementation on cost and profit efficiencies: Evidence from the US commercial banking industry. Journal of Marketing, 73(6), 61-76. doi:10.1509/jmkg.73.6.61

Liang, C. J., Chen, H. J., & Wang, W. H. (2008). Does online relationship marketing enhance customer retention and cross-buying? The Service Industries Journal, 28(6), 769-787. doi:10.1080/02642060801988910

Liang, C. J., & Wang, W. H. (2007). An insight into the impact of a retailers relationship efforts on customers attitudes and behavioural intentions. International Journal of Bank Marketing, 25(5), 336-366. doi:10.1108/02652320710772998

Liang, C. J., Wang, W. H., & Farquhar, J. D. (2009). The influence of customer perceptions on financial performance in financial services. International Journal of Bank Marketing, 27(2), 129-149. doi:10.1108/02652320910935616

Lin, R. J., Chen, R. H., & Chiu, K. K. S. (2010). Customer relationship management and innovation capability: An empirical study. Industrial Management & Data Systems, 110(1), 111-133. doi:10.1108/02635571011008434

Lindgreen, A., & Antioco, M. (2005). Customer relationship management: The case of a European bank. Marketing Intelligence & Planning, 23(2), 136-154. doi:10.1108/02634500510589903

Liu, T. C., & Wu, L. W. (2007). Customer retention and cross-buying in the banking industry: An integration of service attributes, satisfaction and trust. Journal of Financial Services Marketing, 12(2), 132-145. doi:10.1057/palgrave.fsm.4760067

McNally, R. C. (2007). An exploration of call centre agents CRM software use, customer orientation and job performance in the customer relationship maintenance phase. Journal of Financial Services Marketing, 12(2), 169-184. doi:10.1057/palgrave. fsm.4760069

Menon, K., & OConnor, A. (2007). Building customers affective commitment towards retail banks: The role of CRM in each moment of truth. Journal of Financial Services Marketing, 12(2), 157-168. doi:10.1057/palgrave.fsm.4760068

Minami, C., & Dawson, J. (2008). The CRM process in retail and service sector firms in Japan: Loyalty development and financial return. Journal of Retailing and Consumer Services, 15(5), 375-385. doi:10.1016/j.jretconser.2007.09.001

Mithas, S., Krishnan, M. S., & Fornell, C. (2005). Why do customer relationship management applications affect customer satisfaction? Journal of Marketing, 69(4), 201-209. doi:10.1509/ jmkg.2005.69.4.201

Mohd Kassim, N., & Souiden, N. (2007). Customer retention measurement in the UAE banking sector. Journal of Financial Services Marketing, 11(3), 217-228. doi:10.1057/palgrave.fsm.4760040

Morgan, R. M., & Hunt, S. D. (1994). The commitment-trust theory of relationship marketing. Journal of Marketing, 58(3), 20-38. doi:10.2307/1252308

Ngobo, P. V. (2004). Drivers of customers cross-buying intentions. European Journal of Marketing, 38(9/10), 1129-1157. doi:10.1108/03090560410548906

Palmatier, R. W., Dant, R. P., Grewal, D., & Evans,

K. R. (2006). Factors influencing the effectiveness of relationship marketing: A meta-analysis. Journal of Marketing, 70(4), 136-153. doi:10.1509/ jmkg.70.4.136

Parvatiyar, A., & Sheth, J. N. (2001). Customer relationship management: Emerging practice, process, and discipline. Journal of Economic and Social Research, 3(2), 1-34.

Rao, K. N. (2008). Global banking: Emerging trends. Hyderabad, India: The Icfai University Press.

Reimann, M., Schilke, O., & Thomas, J. S. (2010). Customer relationship management and firm performance: The mediating role of business strategy. Journal of the Academy of Marketing Science, 38(3), 326-346. doi:10.1007/s11747-009-0164-y

Reinartz, W., Krafft, M., & Hoyer, W. D. (2004). The customer relationship management process: Its measurement and impact on performance. JMR, Journal of Marketing Research, 41(3), 293-05. doi:10.1509/jmkr.41.3.293.35991

Reinartz, W., Thomas, J. S., & Bascoul, G. (2008). Investigating cross-buying and customer loyalty. Journal of Interactive Marketing, 22(1), 5-20. doi:10.1002/dir.20106

Richard, J. E., Thirkell, P. C., & Huff, S. L. (2007). An examination of customer relationship management (CRM) technology adoption and its impact on business-to-business customer relationships. Total Quality Management and Business Excellence, 18(8), 927-945. doi:10.1080/14783360701350961

Riivari, J. (2005). Mobile banking: A powerful new marketing and CRM tool for financial services companies all over Europe. Journal of Financial Services Marketing, 10(1), 11-20. doi:10.1057/ palgrave.fsm.4770170

Rootman, C., Tait, M., & Bosch, J. (2008). Variables influencing the customer relationship management of banks. Journal of Financial Services Marketing, 13(1), 52-62. doi:10.1057/fsm.2008.5

Roy, S. K., & Shekhar, V. (2010). Dimensional hierarchy of trustworthiness of financial service providers. International Journal of Bank Marketing, 28(1), 47-64. doi:10.1108/02652321011013580

Sciglimpaglia, D., & Ely, D. (2006). Customer account relationships and e-retail banking usage. Journal of Financial Services Marketing, 10(4), 109-122. doi:10.1057/palgrave.fsm.4760026

Selnes, F. (1998). Antecedents and consequences of trust and satisfaction in buyer-seller relationships. European Journal of Marketing, 32(3/4), 305-322. doi:10.1108/03090569810204580

Sharma, A., & Iyer, G. R. (2007). Country effects on CRM successes. Journal of Relationship Marketing, 5(4), 63-78. doi:10.1300/J366v05n04_05

Sin, L. Y. M., Tse, A. C. B., & Yim, F. H. K. (2005). CRM: Conceptualization and scale development. European Journal of Marketing, 39(11/12), 1264-1290. doi:10.1108/03090560510623253

Singh, J. (1990). Voice, exit, and negative word- of-mouth behaviors: An investigation across three service categories. Journal of the Academy of Marketing Science, 18(1), 1-15. doi:10.1007/ BF02729758

Smith, J. B., & Barclay, D. W. (1997). The effects of organizational differences and trust on the effectiveness of selling partner relationships. Journal of Marketing, 61(1), 3-21. doi:10.2307/1252186 Soper, S. (2002). Practice papers: The evolution of segmentation methods in financial services: Where next? Journal of Financial Services Marketing, 7(1), 67-74. doi:10.1057/palgrave.fsm.4770073

Soureli, M., Lewis, B. R., & Karantinou, K. M. (2008). Factors that affect consumers cross-buying intention: A model for financial services. Journal of Financial Services Marketing, 13(1), 5-16. doi:10.1057/fsm.2008.1

Srinivasan, R., & Moorman, C. (2005). Strategic firm commitments and rewards for customer relationship management in online retailing. Journal of Marketing, 69(4), 193-200. doi:10.1509/ jmkg.2005.69.4.193

Verhoef, P. C. (2003). Understanding the effect of customer relationship management efforts on customer retention and customer share development. Journal of Marketing, 67(4), 30-45. doi:10.1509/ jmkg.67.4.30.18685

Verhoef, P. C., & Donkers, B. (2005). The effect of acquisition channels on customer loyalty and cross-buying. Journal of Interactive Marketing, 19(2), 31-43. doi:10.1002/dir.20033

Verhoef, P. C., Franses, P. H., & Hoekstra, J. C. (2001). The impact of satisfaction and payment equity on cross-buying: A dynamic model for a multi-service provider. Journal of Retailing, 77(3), 359-378. doi:10.1016/S0022-4359(01)00052-5

Verhoef, P. C., Franses, P. H., & Hoekstra, J. C. (2002). The effect of relational constructs on customer referrals and number of services purchased from a multiservice provider: Does age of relationship matter? Journal of the Academy of Marketing Science, 30(3), 202.

Wray, B., Palmer, A., & Bejou, D. (1994). Using neural network analysis to evaluate buyer-seller relationships. European Journal of Marketing, 28(10), 32-48. doi:10.1108/03090569410075777 Yim, F. H., Anderson, R. E., & Swaminathan, S. (2004). Customer relationship management: Its dimensions and effect on customer outcomes. Journal of Personal Selling & Sales Management, 24(4), 263-278.

Zeithaml, V. A., Berry, L. L., & Parasuraman, A. (1996). The behavioural consequences of service quality. Journal of Marketing, 60(2), 31-46. doi:10.2307/1251929

This work was previously published in International Journal of Customer Relationship Marketing and Management (IJCRMM), 4(2); edited by Riyad Eid, pages 21-35, copyright 2013 by IGI Publishing (an imprint of IGI Global).

More on the topic Chapter 51 The Role of Relational Mediators in the CRM- Performance Link: Evidence from Indian Retail Banks:

- Chapter 51 The Role of Relational Mediators in the CRM- Performance Link: Evidence from Indian Retail Banks

- Oxford Learning Link

- Critical events link gait IMPAIRMENTS TO POSSIBLE INTERVENTIONS

- Evidence on US Banks in the Great Recession

- Justice as Performance

- The Surprise Effect

- The Changing Role of the Big Four State-Owned Banks

- LINK OF COUNTERPARTIES VIA MARKETS

- Section 6 Emerging Trends

- Relational greatness