MAXIMIZING GROWTH EXPECTATIONS

Imagine a corporation that is currently reporting annual net earnings of $20 million. Assume that five years from now, when its growth has leveled off somewhat, the corporation will be valued at 15 times earnings.

Further assume that the company will pay no dividends over the next five years and that investors in growth stocks currently seek returns of 25% (before considering capital gains taxes).Based on these assumptions, plus one additional number, the analyst can place an aggregate value on the corporation’s outstanding shares. The final required input is the expected growth rate of earnings. Suppose the corporation’s earnings have been growing at a 30% annual rate and app ear likely to continue increasing at the same rate over the next five years. At the end of that period, earnings (rounded) will be $74 million annually. Applying a multiple of 15 times to that figure produces a valuation at the end of the fifth year of $1.114 billion. Investors seeking a 25% rate of return will pay $365 million today for that future value.

These figures are likely to be pleasing to a founder/chief executive officer who owns, for sake of illustration, 20% of the outstanding shares. The successful entrepreneur is worth $73 million on paper, quite possibly up from zero just a few years ago. At the same time, the newly minted multimillionaire is a captive of the market’s expectations.

Suppose investors conclude for some reason that the corporation’s potential for increasing its earnings has declined from 30% to 25% per annum. That is still well above average for Corporate America. Nevertheless, the value of corporation’s shares will decline from $365 million to $300 million, keeping previous assumptions intact.

Overnight, the long-struggling founder will see the value of his personal stake plummet by $13 million.

Financial analysts may shed few tears for him. After all, he is still worth $60 million on paper. If they were in his shoes, however, how many would accept a $13 million loss with perfect equanimity? Most would be sorely tempted, at the least, to avoid incurring a financial reverse of comparable magnitude via every means available to them under GAAP.That all-too-human response is the one typically exhibited by ownermanagers confronted with falling growth expectations. Many, perhaps, most, have no intention to deceive. It is simply that the entrepreneur is by nature a self-assured optimist. A successful entrepreneur, moreover, has had this optimism vindicated. Having taken his company from nothing to $20 million of earnings against overwhelming odds, he believes he can lick whatever short-term problems have arisen. He is confident that he can get the business back onto a 30% growth curve, and perhaps he is right. One thing is certain—if he were not the sort who believed he could beat the odds one more time, he would never have built a company worth $300 million.

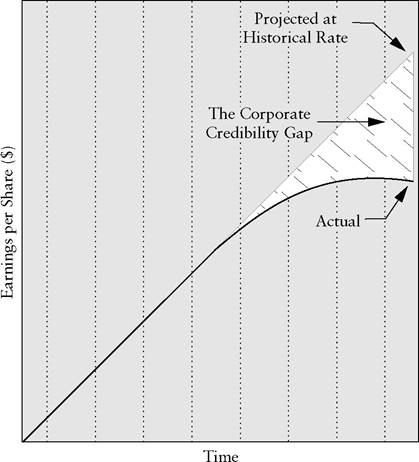

Financial analysts need to assess the facts more objectively. They must recognize that the corporation’s predicament is not unique, but on the contrary, quite common. Almost invariably, senior managers try to dispel the impression of decelerating growth, since that perception can be so costly to them. Simple mathematics, however, tends to make false prophets of corporations that extrapolate high growth rates indefinitely into the future. Moreover, once growth begins to level off (see Exhibit 1.1), restoring it to the historical rate requires overcoming several powerful limitations.

EXHIBIT 1.1 The Inevitability of Deceleration

Shifting investors’ perceptions upward through the Corporate Credibility Gap between actual and management-projected growth is a potentially valuable but inherently difficult undertaking for a company.

Liberal financial reporting practices can make the task somewhat easier. In this light, analysts should read financial statements with a skeptical eye.Limits to Continued Growth

Saturation Sales of a hot new consumer product can grow at astronomical rates for a time. Eventually, however, everybody who cares to will own one (or two, or some other finite number that the consumer believes is enough). At that point, potential sales will be limited to replacement sales plus growth in population, that is, the increase in the number of potential purchasers.

Entry of Competition Rare is the company with a product or service that cannot either be copied or encroached on by a “knockoff” sufficiently similar to tap the same demand, yet different enough to fall outside the bounds of patent and trademark protection.

Increasing Base A corporation that sells 10 million units in Year I can register a 40% increase by selling just 4 million additional units in Year 2. If growth continues at the same rate, however, the corporation will have to generate 59 million new unit sales to achieve a 40% gain in Year 10.

In absolute terms, it is arithmetically possible for volume to increase indefinitely. On the other hand, a growth rate far in excess of the gross domestic product’s annual increase is nearly impossible to sustain over any extended period. By definition, a product that experiences higher-than-GDP growth captures a larger percentage of GDP each year. As the numbers get larger, it becomes increasingly difficult to switch consumers’ spending patterns to accommodate continued high growth of a particular product.

Market Share Constraints For a time, a corporation may overcome the limits of growth in its market and the economy as a whole by expanding its sales at the expense of competitors.

Even when growth is achieved by market share gains rather than by expanding the overall demand for a product, however, the firm must eventually bump up against a ceiling on further growth at a constant rate. For example, suppose a producer with a 10% share of market is currently growing at 25% a year while total demand for the product is expanding at only 5% annually. By Year 14, this supergrowth company will require a 115% market share to maintain its rate of increase. (Long before confronting this mathematical impossibility, the corporation’s growth will likely be curtailed by the antitrust authorities.)Basic economics and compound-interest tables, then, assure the analyst that all growth stories come to an end, a cruel fate that must eventually be reflected in stock prices. Financial reports, however, frequently tell a different tale. It defies common sense yet almost has to be told, given the stakes. Users of financial statements should acquaint themselves with the most frequently heard corporate versions of “Jack and the Beanstalk,” in which earnings—in contradiction to a popular saw—do grow to the sky.

Commonly Heard Rationalizations for Declining Growth

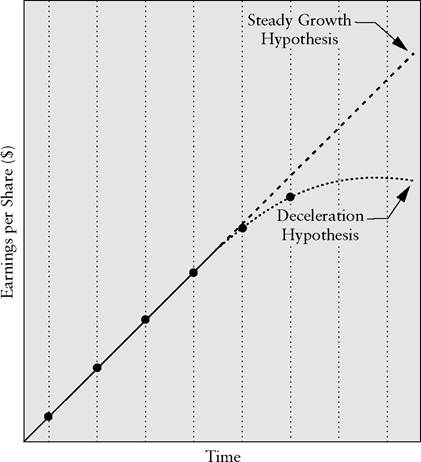

“Our Year-over-Year Comparisons Were Distorted” Recognizing the sensitivity of investors to any slowdown in growth, companies faced with earnings deceleration commonly resort to certain standard arguments to persuade investors that the true, underlying profit trend is still rising at its historical rate (see Exhibit 1.2). Freak weather conditions may be blamed for supposedly anomalous, below-trendline earnings. Alternatively, the company may

EXHIBIT 1.2 “Our Year-over-Year Comparisons Were Distorted”

Is the latest earnings figure an outlier or does it signal the start of a slowdown in growth? Nobody will know for certain until more time has elapsed, but the company will probably propound the former hypothesis as forcefully as it can.

allege that shipments were delayed (never canceled, merely delayed) because of temporary production problems caused, ironically, by the company’s explosive growth.

(What appeared to be a negative for the stock price, in other words, was actually a positive. Orders were coming in faster than the company could fill them—a high-class problem indeed.) Widely publicized macroeconomic events such as the Y2K problem18 receive more than their fair share of blame for earnings shortfalls. However plausible these explanations may sound, analysts should remember that in many past instances, short-term supposed aberrations have turned out to be advance signals of earnings slowdowns.''New Products Will Get Growth Back on Track" Sometimes, a corporation’s claim that its obviously mature product lines will resume their former growth path becomes untenable. In such instances, it is a good idea for management to have a new product or two to show off. Even if the products are still in development, some investors who strongly wish to believe in the corporation will remain steadfast in their faith that earnings will continue growing at the historical rate. (Such hopes probably rise as a function of owning stock on margin at a cost well above the current market.) A hardheaded analyst, though, will wait to be convinced, bearing in mind that new products have a high failure rate.

“We're Diversifying Away from Mature Markets” If a growth-minded company’s entire industry has reached a point of slowdown, it may have little choice but to redeploy its earnings into faster-growing businesses. Hunger for growth, along with the quest for cyclical balance, is a prime motivation for the corporate strategy of diversification.

Diversification reached its zenith of popularity during the “conglomerate” movement of the 1960s. Up until that time, relatively little evidence had accumulated regarding the actual feasibility of achieving high earnings growth through acquisitions of companies in a wide variety of growth industries.

Many corporations subsequently found that their diversification strategies worked better on paper than in practice. One problem was that they had to pay extremely high price-earnings multiples for growth companies that other conglomerates also coveted. Unless earnings growth accelerated dramatically under the new corporate ownership, the acquirer’s return on investment was fated to be mediocre. This constraint was particularly problematic for managers who had no particular expertise in the businesses they were acquiring. Still worse was the predicament of a corporation that paid a big premium for an also-ran in a “hot” industry. Regrettably, the number of industry leaders available for acquisition was by definition limited.By the 1980s, the stock market had rendered its verdict. The priceearnings multiples of widely diversified corporations carried a “conglomerate discount.” One practical problem was the difficulty security analysts encountered in trying to keep tabs on companies straddling many different industries. Instead of making 2 + 2 equal 5, as they had promised, the conglomerates’ managers presided over corporate empires that traded at cheaper prices than their constituent companies would have sold for in aggregate had they been listed separately.

Despite this experience, there are periodic attempts to revive the notion of diversification as a means of maintaining high earnings growth indefinitely into the future. In one variant, management makes lofty claims about the potential for “cross-selling” one division’s services to the customers of another. It is not clear, though, why paying premium acquisition prices to assemble the two businesses under the same corporate roof should prove more profitable than having one independent company pay a fee to use the other’s mailing list. Battle-hardened analysts wonder whether such corporate strategies rely as much on the vagaries of mergers-and-acquisitions accounting (see Chapter 10) as they do on bona fide synergy.

All in all, users of financial statements should adopt a “show-me” attitude toward a story of renewed growth through diversification. It is often nothing more than a variant of the myth of above-average growth forever. Multi-industry corporations bump up against the same arithmetic that limits earnings growth for “focused” companies.

More on the topic MAXIMIZING GROWTH EXPECTATIONS:

- MAXIMIZING POSTACQUISITION REPORTED EARNINGS

- Exchange Rate Expectations, Capital Flows, and Pressure for Appreciation

- Wealth, utility and revealed preferences: the choice of maximand

- Basicframework

- Step-by-Step Innovations*

- Macro Regression Models for M0 and H

- Synopsis

- TAKING ECONOMIC THEORY SERIOUSLY

- THE LONG GERMINATION OF THE IDEA OF A WORLD FREE OF POVERTY

- Oligopoly in theory and practice