Macroeconomic Policy and the Phillips Curve

Discuss whether the Phillips curve offers a “menu” of inflationunemployment combinations from which policymakers can choose.

In Touch with Data and Research

The Lucas Critique

Suppose that a particular tennis player, RN, has consistently won the French Open tournament, which is played on a clay surface, for the last five years.

However, you notice that RN has not won any tournaments played on other surfaces. Based on this knowledge, placing a bet on RN winning the next French Open would seem safe. Now, consider a hypothetical situation where, aiming to decrease on-court injuries, the organizers decide to change all the surfaces to grass. Clearly, it would be foolhardy to place a huge bet on RN winning the next tournament under this new arrangement. Simply put, when the tournament rules change, people's expectations and subsequent behavior change as well.How important are expectations and behavior for effective policymaking when it comes to the macroeconomy? In 1976, Robert E. Lucas of the University of Chicago published a seminal paper[219] critiquing the use of econometric models such as the Phillips curve for policymaking and policy evaluation. In what has become known as the Lucas Critique, he argued that agents' expectations of the policy process were unlikely to remain stable when policymakers changed their behavior. In other words, when new policies are implemented or expected, economic behavior is affected, and an assumption that the historical relationships will remain the same is likely to be misplaced.

The observation of what seemed to be a historic trade-off between inflation and unemployment led some policymakers to believe that unemployment could be permanently reduced by increasing inflation. However, expected changes in inflation will shift the Phillips curve rather than move along it, so the short-run Phillips curve breaks down.

New economic policies, like the tournament's replacement of the playing surface in the hypothetical example above, can change the economic landscape, which in turn influences expectations, behaviors, and outcomes.The Lucas critique thus emphasizes the need for caution when anticipating the effectiveness of policies, because rational agents tend to anticipate the consequences of new policies and will adapt their behaviors in ways that will affect the effectiveness of those policies. It is therefore important that economists and policymakers consider the potential impact of policy change on behavior—this is particularly important when new policies are being introduced. Notably, the Lucas critique has been influential in helping to reorientate macroeconomic research toward models with explicit considerations of expectations and taste.

10"Econometric Policy Evaluation: A Critique,” in K. Brunner and A. H. Meltzer, eds., Carnegie- Rochester Conference Series on Public Policy 1, 1976, pp. 19-46. information. In the meantime, some prices reflect older information, and the rate of inflation is higher than the expected inflation rate based on this older information. In response to increased inflation, therefore, unemployment may remain below the natural rate for a while.

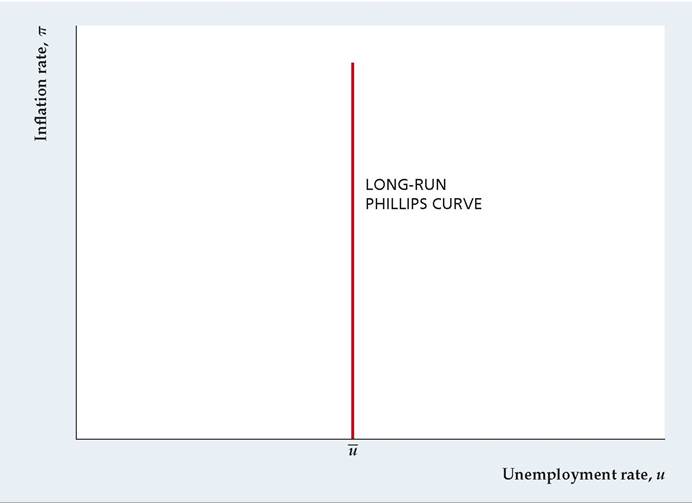

The Long-Run Phillips Curve

Although classicals and Keynesians disagree about whether the Phillips curve relationship can be exploited to reduce unemployment temporarily, they agree that policymakers can't keep the unemployment rate permanently below the natural rate by maintaining a high rate of inflation. Expectations about inflation eventually will adjust so that the expected and actual inflation rates are equal, or πe = π. The expectations-augmented Phillips curve (Eq. 12.1) implies that, when πe = π, the actual unemployment rate, u, equals the natural unemployment rate, U. Thus the actual unemployment rate equals the natural rate in the long run regardless of the inflation rate maintained.

The long-run relationship of unemployment and inflation is shown by the long-run Phillips curve. In the long run, because unemployment equals the natural rate regardless of the inflation rate, the long-run Phillips curve is a vertical line at u = U, as shown in Figure 12.8.

The vertical long-run Phillips curve is related to the long-run neutrality of money, discussed in Chapters 10 and 11. Classicals and Keynesians agree that changes in the money supply will have no long-run effects on real variables, including unemployment. The vertical long-run Phillips curve carries the notion of monetary neutrality one step further by indicating that changes in the growth rate of money, which lead to changes in the inflation rate, also have no real effects in the long run.

FIGURE 12.8

The long-run Phillips curve

People won't permanently overestimate or underestimate the rate of inflation, so in the long run the expected and actual inflation rates are equal and the actual unemployment rate equals the natural unemployment rate. Because actual unemployment equals the natural rate in the long run, regardless of the inflation rate, the long-run Phillips curve is vertical.

12.3

More on the topic Macroeconomic Policy and the Phillips Curve:

- Macroeconomic Policy and the Phillips Curve

- CHAPTER SUMMARY

- The Phillips Curve and Inflationary Expectations

- Unemployment and Inflation: Is There a Trade-Off?

- Detailed Contents

- Fighting Inflation: The Role of Inflationary Expectations

- The Theory of Discretionary Monetary and Fiscal Policy

- Conclusion

- As already noted, following the Great Depression of the 1930s, the analysis of aggregate fluctuations evolved into macroeconomics, on the basis of Keynesian models.

- 24 Macroeconomic Policies