THE POLITICAL ECONOMY CHANNEL

We have already seen in the previous sections some channels through which the distribution of income and wealth is interconnected with the aggregate performance of the economy. In this section, we discuss one particular channel through which inequality affects economic activities, that is, through the political and institutional system.

Because many policies have redistributive consequences, the degree of inequality plays a central role in the choice of policies because societies with more unequal distributions of resources might demand greater redistribution. Because redistributive policies are often distortionary, the result is that more unequal societies tend to experience lower income or growth (or both).Many contributions emphasize this mechanism, starting with Meltzer and Richard (1981). Examples are Persson and Tabellini (1994), Alesina and Rodrik (1994), Krusell and Rios-Rull (1996), and Krusell et al. (1997). Many of these contributions, however, ignore individual uncertainty, which in a dynamic environment could play an important role in affecting the demand for redistribution as well as the distortions associated with redistributive policies. The goal of this section is to present a simple framework that illustrates the central idea ofthe early literature. It shows how the consideration of idiosyncratic uncertainty enriches the analysis and makes the relation between inequality and redistribution more complex than in these early studies.

14.5.1 A Simple Two-Period Model

Suppose that there is a continuum of agents who are alive for two periods. Agents value consumption, ct, but dislike working, ht, according to the utility function

There are two sources of income: endowment, ηt, and labor, ht.

Individual endowments evolve according to

Ncquaiiy ∏MV∣αuucLUHumιcs 1^.0:2

distribution (inequality) constant. This parameter determines the degree of mobility: higher values of ρ imply lower mobility.

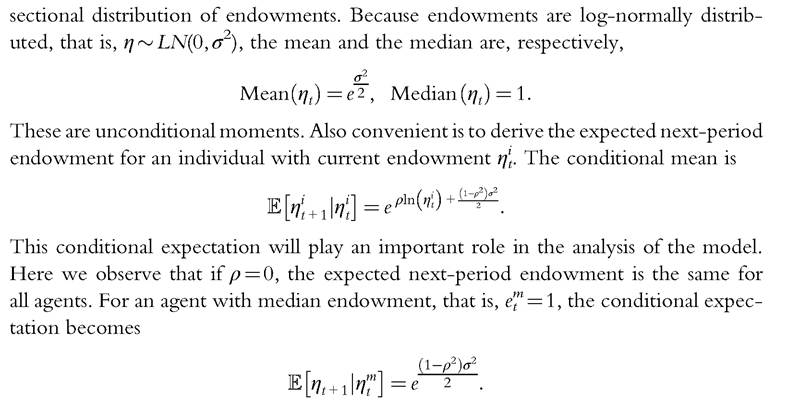

Before continuing, it will be helpful to derive some of the key moments of the cross-

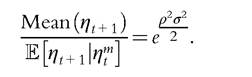

We can then compute the ratio of the next period economywide average endowment over the next period endowment expected by an agent whose current endowment is the median value. This is equal to

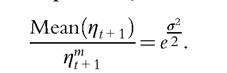

This expression makes it clear that the difference between the average endowment and the endowment expected by the agent with the median endowment in the current period depends on the persistent parameter ρ. The difference becomes zero if there is no persistence, that is, ρ = 0, and it is maximal when ρ = 1. Although the parameter ρ affects the ratio between the average endowment and the expected endowment by the median agent, ex post inequality does not depend on ρ. In fact, we have that

We will use these moments below, after completing the description of the model.

The government taxes incomes, from endowment and labor, at rate τt and redistributes the revenues as lump-sum transfers. The budget constraint for the government is  where i is the index for an individual agent.

where i is the index for an individual agent.

Agents do not save and solve a static optimization problem. Given the tax rate and the transfer, an individual agent i maximizes the period utility by choosing the labor supply htt, subject to the following budget constraint:

Taking first order conditions with respect to ht for an individual worker with endowment η't, we get the supply of labor ht = 1 — τt.

Substituting in the utility function and using the equation that defines the government transfers, we get the indirect utility for period t:

Now suppose that agents vote for the next period tax rate τt+1. The tax rate preferred by an agent with current endowment η't maximizes the expected next period indirect utility, that is,

where we have denoted by F(η) the distribution of endowments. Because the logendowments are normally distributed, F(η) is a log-normal distribution.

Notice that the voter forms expectations about the future endowment conditional on the current endowment. Of course, the higher is the persistence, the higher the dependence of the expected value from the current value.

Taking the first order condition, we derive

next-period tax rate. Notice that this term also depends on the tax rate. The above condition implicitly determines the tax rate.

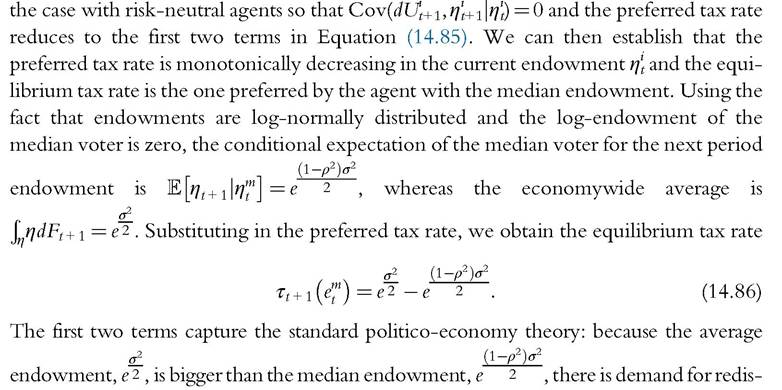

The first term on the right-hand side of Equation (14.85) is the mean value of the economywide endowment, which is equal to This term is the same for all agents. The second term is the expected endowment of agent i given the current endowment. This term is increasing in ηt, unless ρ ≤ 0, which is excluded by assumption. Therefore, ignoring the third term, the preferred tax rate decreases with the current endowment.

This term is the same for all agents. The second term is the expected endowment of agent i given the current endowment. This term is increasing in ηt, unless ρ ≤ 0, which is excluded by assumption. Therefore, ignoring the third term, the preferred tax rate decreases with the current endowment.

The third term captures the role of risk aversion.Because the utility function is strictly concave and its derivative is strictly decreasing, decreases with the realization of

decreases with the realization of

next period endowment implying that the covariance term is negative.

implying that the covariance term is negative.

14.5.1.1 The Case of Risk Neutrality

Because the third term in the first order condition (14.85) is itself a function of τtt+1, it is difficult to derive an analytical expression for the tax rate. Therefore, we first specialize to  tribution. If we increase inequality by raising σ, the demand for redistribution increases. Because the optimal effort chosen by all agents is h = 1 — τ, higher taxes discourage effort with negative effects on aggregate production. In some of the models proposed in the literature, taxes distort the accumulation of capital instead of effort, but the idea is similar.

tribution. If we increase inequality by raising σ, the demand for redistribution increases. Because the optimal effort chosen by all agents is h = 1 — τ, higher taxes discourage effort with negative effects on aggregate production. In some of the models proposed in the literature, taxes distort the accumulation of capital instead of effort, but the idea is similar.

The mechanism described above links inequality to redistribution and macroeconomic activity and captures the key features of the model studied in Meltzer and Richard (1981). In addition to this mechanism, the model presented here emphasizes the role of mobility captured by the parameter ρ. Ifwe reduce ρ so that the economy experiences higher mobility, the cross-sectional inequality does not change. In fact, the ratio of average endowment and median endowment remain However, the tax rate preferred by the median voter declines, as we can see from Equation (14.86). Even if the median voter has low endowment in the current period, what matters for next period taxes is the future endowment. If mobility is high, the median voter does not expect to keep the low endowment in the future. Thus, it is not optimal to choose high tax rates. In the limiting case with ρ = 0, the expected future endowment for all agents will be the average endowment and, in expected terms, the future benefit of redistribution is zero for all agents.

However, the tax rate preferred by the median voter declines, as we can see from Equation (14.86). Even if the median voter has low endowment in the current period, what matters for next period taxes is the future endowment. If mobility is high, the median voter does not expect to keep the low endowment in the future. Thus, it is not optimal to choose high tax rates. In the limiting case with ρ = 0, the expected future endowment for all agents will be the average endowment and, in expected terms, the future benefit of redistribution is zero for all agents.

The importance of mobility for political preferences has received less attention than cross-sectional inequality. But the simple model presented here shows that mobility is also an important factor in the determination of political preferences. More importantly, if inequality and mobility are not independent, either across countries or across times, by focusing only on inequality we may reach inaccurate conclusions. Suppose, for example, that an increase in cross-sectional inequality, σ, is associated with a decrease in ρ, that is, with an increase in mobility. Therefore, we have two contrasting effects: the increase in σ leads to higher taxes, whereas the decrease in ρ leads to lower taxes.

This example may help to explain why, in certain episodes of increasing inequality, such as in the United States before the recent crisis, we do not see a significant increase in demand for redistribution. Perhaps the reason is that voters perceive higher mobility as coincident with greater inequality. Then, thanks to the perceived mobility, voters do not demand higher taxes and the economy continues to perform well even if income becomes more concentrated. However, if the performance of the economy changes and voters start to perceive lower mobility, they will start demanding more redistribution, which will further deteriorate the performance of the economy. This idea has been developed in Quadrini (1999) in a model that features two equilibria. The first equilibrium is characterized by high growth, high inequality, and low redistribution. The second equilibrium is characterized by low growth, low inequality, and high redistribution.[19] The idea that the prospect of upward mobility reduces the demand for redistribution has also been studied in Benabou and Ok (2001).

14.5.1.2 ThecaseofRiskAversion

We now assume that the utility function is concave and takes the following form:

where the parameter ν captures the curvature of the utility function.

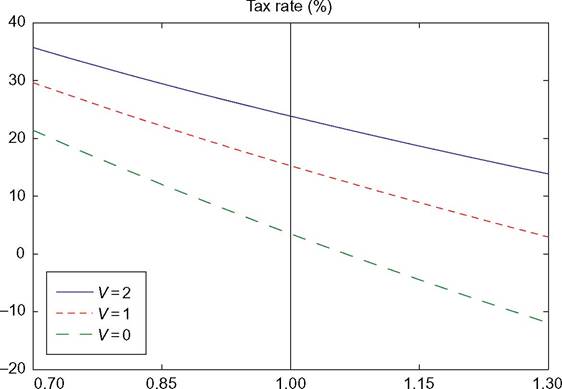

Figure 14.6 plots the preferred tax rate as a function of current endowment ηtt for different values of ν. As can be seen from the figure, the preferred tax rate is monotonically decreasing in current endowment, and therefore, the median voter theorem also applies in the case of risk-averse agents. Furthermore, we see that, for each endowment level η^, the preferred tax rate increases with risk aversion.

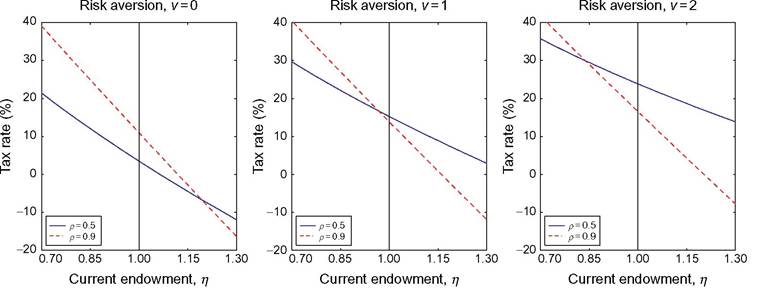

Figure 14.7 plots the preferred tax rate as a function of current endowment for different degrees of mobility and risk aversion. The first panel is for the case of risk neutrality. In this case, we see that lower mobility (ρ changes from 0.5 to 0.9) increases the equilibrium tax rate, that is, the tax rate preferred by the median voter, which in the figure is identified by the vertical line. These are the properties we have shown analytically in the previous subsection. However, when agents are risk averse, lower mobility reduces

Current endowment, η

Figure 14.6 Preferred tax rates for different degrees of risk aversion. The inequality and mobility parameters are σ=0.5 and p=0.5. The vertical line denotes the median endowment.

Figure 14.7 Preferred tax rates for different degrees of mobility, p∈{0.5,0.9}, and risk aversion, n∈{0,1,2}. The inequality parameter is σ=0.5. The vertical line denotes the median endowment.

the equilibrium tax rate. The reason is that, conditional on the current endowment, lower mobility means that agents face lower risk. In fact, with ρ = 1, next period endowment is equal to current endowment. Thus, there is less demand for insurance.

This example shows that mobility affects equilibrium policies through two mechanisms. The first mechanism works through the impact of mobility on the redistributive gains from next period taxes. When mobility is low, the expected redistributive gains are high. These gains vanish if mobility is perfect, that is, ρ = 0. The second mechanism works through the impact of mobility on individual risk. Given the current endowment, higher mobility (lower ρ) increases the conditional volatility of next period endowment and the median agent faces higher risk. Thus, greater redistribution is preferred if preferences are concave. This second mechanism is irrelevant when agents are risk neutral but becomes important when agents are risk averse. For a sufficiently high degree of risk aversion, the second mechanism dominates and the equilibrium tax rate declines with lower mobility.

Corbae et al. (2009) and Bachmann and Bai (2013) are two papers that study infinite horizon political economy models with income taxes and uninsurable idiosyncratic risks. Thus, these two papers are potentially capable of capturing the mechanisms described in this section.

14.5.2 More on the Political Economy Channel

Some theories formulate channels through which redistributive taxes have a beneficial effect on the macroeconomy in the presence of financial constraints. For example, in the Schumpeterian view where entrepreneurship is central to economic growth, financial constraints and the absence of insurance markets make entrepreneurial investment suboptimal. Under these conditions, redistribution may provide extra resources to constrained entrepreneurs and could facilitate more investments in growth-enhancing activities. At the same time, a redistributive system provides an implicit mechanism for consumption smoothing (a person pays high taxes when he or she earns high profits but receives payments in case of losses). Therefore, it provides insurance. Thus, if entrepreneurs are risk averse, redistribution could encourage investment.

A similar mechanism applies to the investment in education or human capital. If education is important for economic growth, and parents choose suboptimal levels of education because of financial constraints, then government transfers may allow for greater investment and growth. A more direct mechanism could work through the financing of public education, as in Glomm and Ravikumar (1992).

Political economy forces are also important for the choice of government borrowing. Azzimonti et al. (2014) propose a theory of public debt where greater income inequality could increase the incentive of the government to borrow more if the higher inequality is associated with greater individual risk. This is because higher risk increases the demand for safe assets, which are undersupplied when markets are incomplete. If financial markets are integrated, the increase in inequality (risk) in a few countries could induce a worldwide increase in public debt. In this way, the paper proposes one of the possible mechanisms for explaining the rising public debt observed in most of the industrialized countries since the early 1980s.

We close this section by mentioning that, although a large branch of the political economy literature has been developed on the assumption that voters are self-motivated and agree on their views of the world, so that their assessment of a policy is based on how much they benefit, some authors have proposed alternative frameworks. Especially interesting is Piketty (1995). This study develops a model in which agents prefer different policies not because they are selfish but because they have different beliefs. All voters care about social welfare, but some believe that luck is more important in generating income, whereas others believe that effort is more important. These beliefs evolve over time based on personal experience, but they never converge. Thus, at any point in time, preferences are heterogeneous. Although not explicitly explored in the original article, it is possible to introduce factors that could change the distribution of beliefs and with them the properties of the macro economy. This could be an interesting direction for future research.

14.6.

More on the topic THE POLITICAL ECONOMY CHANNEL:

- Contents

- Otoscopy

- Conclusion

- Index

- CONTENTS

- THEORETICAL CONSIDERATIONS

- Empiricalanalysis

- DIGESTION

- Cicero on Gyges’ ring and how Plutarch deals with the Puzzles

- Chapter 27 The Price of Freedom