Deficits and Inflation

Explain the link between deficits and inflation.

In this final section of the chapter we discuss one more concern that has been expressed about government budget deficits: that deficits are inflationary.

We show that the principal link between deficits and inflation is that in some circumstances deficits lead to higher rates of growth in the money supply and that high rates of money growth in turn cause inflation.The Deficit and the Money Supply

Inflation—a rising price level—results when aggregate demand increases more quickly than does aggregate supply. In terms of the AD-AS framework, suppose that the long-run aggregate supply curve (which reflects the productive capacity of the economy) is fixed. Then for the price level to rise, the aggregate demand curve must rise over time.

Both the classical and Keynesian models of the economy imply that deficits can cause aggregate demand to rise more quickly than aggregate supply, leading to an increase in the price level. In both models a deficit owing to increased government purchases reduces desired national saving, shifting the IS curve up and to the right and causing aggregate demand to rise. This increase in aggregate demand causes the price level to rise.[301] If we assume (as Keynesians usually do) that Ricardian equivalence doesn't hold, a budget deficit resulting from a cut in taxes or an increase in transfers also reduces desired national saving, increases aggregate demand, and raises the price level. Thus deficits resulting from expansionary fiscal policies (increased spending or reduced taxes) will be associated with inflation.

However, an increase in government purchases or a cut in taxes causes only a one-time increase in aggregate demand. Therefore, although we expect expansionary fiscal policies to lead to a one-time increase in the price level (that is, a temporary burst in inflation), we don't expect an increase in government purchases or a cut in taxes to cause a sustained increase in inflation.

In general, the only factor that can sustain an increase in aggregate demand, leading to continuing inflation, is sustained growth in the money supply. Indeed, high rates of inflation are almost invariably linked to high rates of national money growth (recall the Application "Money Growth and Inflation in European Countries in Transition," in Chapter 7). The key question therefore is: Can government budget deficits lead to ongoing increases in the money supply?The answer is "yes." The link is the printing of money to finance government spending when the government cannot (or does not want to) finance all of its spending by taxes or borrowing from the public. In the extreme case, imagine a government that wants to spend $10 billion (say, on submarines) but has no ability to tax or borrow from the public. One option is for this government to print $10 billion worth of currency and use this currency to pay for the submarines. The revenue that a government raises by printing money is called seignorage. Any government with the authority to issue money can use seignorage; governments that do not have the authority to issue money, such as state governments in the United States, can't use seignorage.

Actually, governments that want to finance their deficits through seignorage don't simply print new currency but use an indirect procedure. First, the Treasury authorizes government borrowing equal to the amount of the budget deficit ($10 billion in our example), and a corresponding quantity of new government bonds is printed and sold. Thus the deficit still equals the change in the outstanding government debt (Eq. 15.3). However, the new government bonds aren't sold to the public. Instead, the Treasury asks (or requires) the central bank to purchase the $10 billion in new bonds. The central bank pays for its purchases of new bonds by printing $10 billion in new currency,[302] which it gives to the Treasury in exchange for the bonds. This newly issued currency enters general circulation when the government spends it on its various outlays (the submarines).

Note that the purchase of bonds by the central bank increases the monetary base by the amount of the purchase (see Chapter 14), as when the central bank purchases government bonds on the open market.The precise relationship between the size of the deficit and the increase in the monetary base is

Equation (15.6) states that the (nominal) government budget deficit equals the total increase in (nominal) government debt outstanding, which can be broken into additional government debt held by the public,

which can be broken into additional government debt held by the public, p, and by the central bank, ABcb. The increase in government debtheld by the central bank in turn equals the increase in the monetary base,

p, and by the central bank, ABcb. The increase in government debtheld by the central bank in turn equals the increase in the monetary base, The increase in the monetary

The increase in the monetary

base equals the amount of seignorage collected by the government.

The final link between the budget deficit and the money supply has to do with the relationship between the money supply and the monetary base. To make the link as simple as possible, we consider an all-currency economy. Specifically, in an all-currency economy there are no banks, and all money is held in the form of currency. In an all-currency economy, the money supply equals the amount of currency outstanding (because there are no deposits) and the monetary base equals the amount of currency outstanding (because there are no bank reserves), so the money supply and the monetary base are equal. Therefore, in an all-currency economy, Eq. (15.6) implies that

Why would governments use seignorage to finance their deficits, knowing that continued money creation ultimately leads to inflation? Under normal conditions developed countries rarely use seignorage.

For example, in recent years (preceding the financial crisis of 2008) the monetary base in the United States increased on average by about $40 billion per year, which equals about 2% of Federal government receipts. Heavy reliance on seignorage usually occurs in war-torn or developing countries, in which military or social conditions dictate levels of government spending well above what the country can raise in taxes or borrow from the public.Real Seignorage Collection and Inflation

The amount of real revenue that the government collects from seignorage is closely related to the inflation rate. To examine this link let's consider an all-currency economy in which real output and the real interest rate are fixed and the rates of money growth and inflation are constant. In such an economy the real quantity of money demanded is constant[303] and hence, in equilibrium, the real money supply must also be constant. Because the real money supply M/P doesn't change, the growth rate of the nominal money supply must equal the growth rate of

must equal the growth rate of

the price level, or the rate of inflation π:

Equation (15.8) expresses the close link between an economy's inflation rate and money growth rate.

How much seignorage is the government collecting in this economy? The nominal value of seignorage in any period is the increase in the amount of money in circulation Multiplying both sides of Eq. (15.8) by M and rearranging gives an equation for the nominal value of seignorage:

Multiplying both sides of Eq. (15.8) by M and rearranging gives an equation for the nominal value of seignorage:

Real seignorage revenue, R, is the real value of the newly created money, which equals nominal seignorage revenue, ∆M, divided by the price level, P. Dividing both sides of Eq.

(15.9) by the price level P gives

Equation (15.10) states that the government's real seignorage revenue, R, equals the inflation rate, π, times the real money supply, M/P.

Equation (15.10) illustrates why economists sometimes call seignorage the inflation tax. In general, for any type of tax, tax revenue equals the tax rate multiplied by the tax base (whatever is being taxed). In the case of the inflation tax, the tax base is the real money supply and the tax rate is the rate of inflation. Multiplying the tax base (the real money supply) by the tax rate (the rate of inflation) gives the total inflation tax revenue.

How does the government collect the inflation tax and who pays this tax? The government collects the inflation tax by printing money (or by having the central bank issue new money) and using the newly created money to purchase goods and services. The inflation tax is paid by any member of the public who holds money because inflation erodes the purchasing power of money. For example, when the inflation rate is 10% per year, a person who holds currency for a year loses 10% of the purchasing power of that money and thus effectively pays a 10% tax on the real money holdings.

Suppose that a government finds that the seignorage being collected doesn't cover its spending and begins to increase the money supply faster. Will this increase in the money growth rate cause the real seignorage collected by the government to rise? Somewhat surprisingly, it may not. As Eq. (15.10) shows, the real seignorage collected by the government is the product of two terms—the rate of inflation (the tax rate) and the real money supply (the tax base). By raising the money growth rate, the government can increase the inflation rate. However, at a constant real interest rate, a higher rate of inflation will raise the nominal interest rate, causing people to reduce the real quantity of money held.

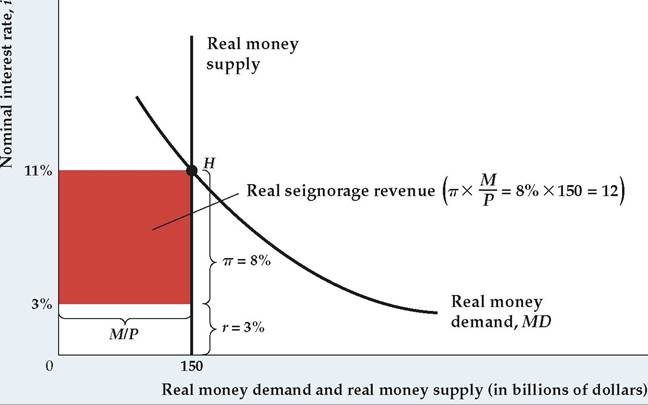

Thus whether real seignorage revenue increases when the money growth rate increases depends on whether the rise in inflation, π, outweighs the decline in real money holdings, M/P.[304]This point is illustrated by Figure 15.9, which shows the determination of real seignorage revenue at an assumed constant real interest rate of 3%. The real quantity of money is measured along the horizontal axes, and the nominal interest rate is measured along the vertical axes. The downward-sloping MD curves show the real demand for money; they slope downward because an increase in the nominal interest rate reduces the real quantity of money demanded.

In Fig. 15.9(a) the actual and expected rate of inflation is 8%, so that (for a real interest rate of 3%) the nominal interest rate is 11%. When the nominal interest rate is 11%, the real quantity of money that people are willing to hold is $150 billion (point H). Using Eq. (15.10), we find that the real value of seignorage revenue is 0.08 ? $150 billion, or $12 billion. Real seignorage revenue is represented graphically by the area of the shaded rectangle. The rectangle's height equals the inflation rate (8%) and the rectangle's width equals the real quantity of money held by the public ($150 billion).

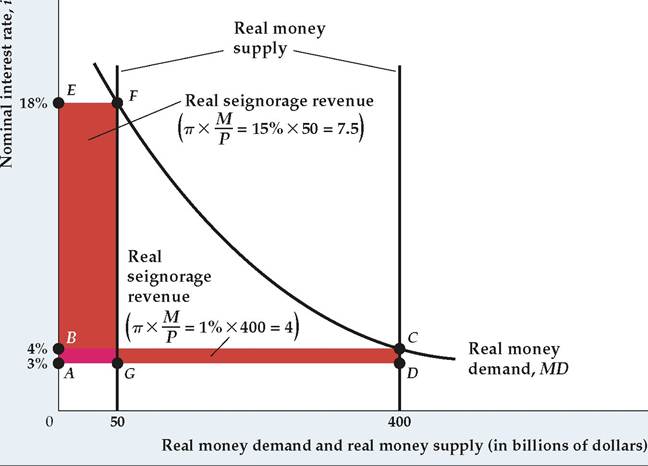

Figure 15.9(b) shows the real amount of seignorage revenue at two different inflation rates. The real interest rate (3%) and the money demand curve in Fig. 15.9(b) are identical to those in Fig. 15.9(a). When the rate of inflation is 1% per year, the nominal interest rate is 4%, and the real quantity of money that the public holds is $400 billion. Real seignorage revenue is 0.01 ? $400 billion = $4 billion, or the area of rectangle ABCD. Alternatively, when the rate of inflation is 15% per year, the nominal interest rate is 18% per year, and the real value of the public's money holdings is $50 billion. Real seignorage revenue in this case is $7.5 billion, or the area of rectangle AEFG.

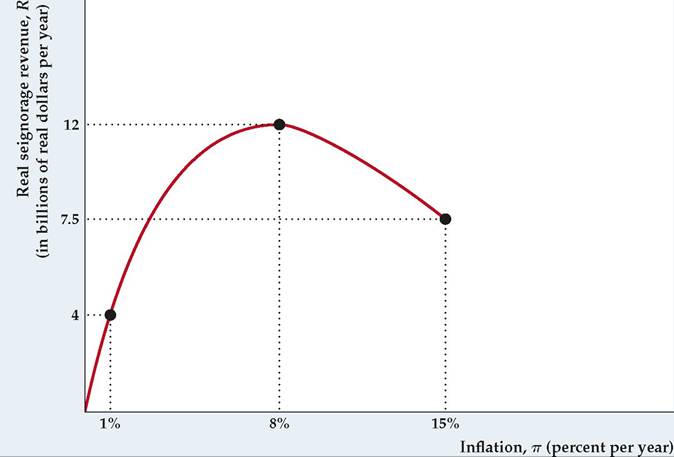

Comparing Fig. 15.9(a) and Fig. 15.9(b) reveals that real seignorage revenue is higher when inflation is 8% per year than when inflation is either 1% per year or 15% per year. Figure 15.10 shows the relationship between the inflation rate and seignorage revenue. At low inflation rates an increase in the inflation rate increases real seignorage revenue. However, at high inflation rates an increase in inflation reduces real seignorage revenue. In Fig. 15.10 the maximum possible real seignorage revenue is $12 billion, which is achieved at the intermediate level of inflation of 8% per year.

What happens if the government tries to raise more seignorage revenue than the maximum possible amount? If it does so, inflation will rise but the real value

FIGUREJ5.9

The determination of real seignorage revenue

(a) The downwardsloping curve, MD, is the money demand function for a given level of real income. The real interest rate is assumed to be 3%. When the rate of inflation is 8%, the nominal interest rate is 11%, and the real quantity of money held by the public is $150 billion (point H). Real seignorage revenue collected by the government, represented by the area of the shaded rectangle, equals the rate

of inflation (8%) times the real money stock ($150 billion), or $12 billion.

(b) The money demand function, MD, is the same as in (a), and the real interest rate remains at 3%. When the inflation rate is 1%, the nominal interest rate is 4%, and the real quantity of money held by the public is $400 billion. In this case real seignorage revenue equals the area of the rectangle, ABCD, or

$4 billion. When the rate of inflation is 15%, the nominal interest rate is 18%, and the real money stock held by the public is $50 billion. Real seignorage revenue in this case equals the area of the rectangle AEFG, or $7.5 billion.

(a) Determination of real seignorage revenue for π = 8%

(b) Determination of real seignorage revenue for π = 1% and π = 15%

of the government's seignorage will fall as real money holdings fall. If the government continues to increase the rate of money creation, the economy will experience a high rate of inflation or even hyperinflation. Inflation will continue until the government reduces the rate of money creation either by balancing its budget or by finding some other way to finance its deficit.

FIGUREJ5.10

The relation of real seignorage revenue to the rate of inflation Continuing the example of Fig. 15.9, this figure shows the relation of real seignorage revenue, R, measured on the vertical axis, to the rate of inflation, π, measured on the horizontal axis. From Fig. 15.9(a), when inflation is 8% per year, real seignorage revenue is $12 billion. From Fig. 15.9(b), real seignorage is $4 billion when inflation is 1% and $7.5 billion when inflation is 15%. At low rates of inflation, an increase in inflation increases seignorage revenue.

At high rates of inflation, increased inflation can cause seignorage revenue to fall. In this example the maximum amount of seignorage revenue the government can obtain is $12 billion, which occurs when the inflation rate is 8%.

In some hyperinflations, governments desperate for revenue raise the rate of money creation well above the level that maximizes real seignorage. For example, in the extreme hyperinflation that hit Germany after World War I, rapid money creation drove the rate of inflation to 322% per month. In contrast, in his classic study of the German hyperinflation, Philip Cagan32 of Columbia University calculated that the constant rate of inflation that would have maximized the German government's real seignorage revenue was "only" 20% per month.

More on the topic Deficits and Inflation:

- Article 3.8 Markets: the road to redemption

- Portugal

- Malaysia

- Reserve Accumulation and the InternationalRole of the Dollar

- France

- Introduction

- Latvia

- India

- Belgium

- Argentina